Last week we wrote about how eerily quiet the digital assets market is. Unfortunately, not much has changed a week later. The macro picture has been relatively unchanged, and the debt ceiling saga has had little to no effect on most equities, bonds, or digital assets (USA CDS hitting new wides seems to be the most affected). Meanwhile, digital asset-specific news and events have been few and far between.

This isn’t necessarily good or bad for most higher quality “benchmark” digital assets. These projects and companies have stickier investors and often real revenue streams to buoy prices via buybacks and burns while it’s slow. The next move higher or lower for this group will likely be driven by specific news or flows. But the lack of market excitement could be very bad for many smaller capitalization tokens and those that have yet to find any product-market fit.

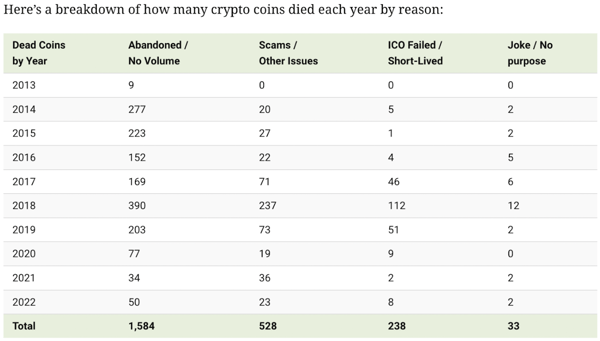

Visual Capitalist recently released an interesting study discussing dead digital assets that have faded away. As we’ve discussed in the past, tokens are really perpetual call options, with few (if any) triggers for dissolution. Token issuers rarely file for bankruptcy, and even if they do, the tokens often keep trading as some sort of future call option on a resurrection (e.g., FTT, VGX) because there is no court-approved re-organization. But while there is no court process to officially value a token at zero in a restructuring, many tokens still do fail, typically due to the following:

Reasons 3-4 should scare many token issuers and investors right now. There are plenty of projects that are in year 3+ that still have not really produced anything of value other than a publicly traded token. Further, with market makers and exchanges pulling back for regulatory reasons, many non-core assets will likely be left for dead.

Right after the boom year of 2017, 2018 was a particularly bad year for defunct tokens. The hype and subsequent fade didn’t kill major digital assets of successful projects in sectors and themes that are relevant, but it did kill many other off-the-run projects. We’re now 18 months past the last hype cycle, and the lack of liquidity and usage of many smaller projects is a cause for real concern.

Source: Visual Capitalist

Again, this is affecting a very small percentage of the overall crypto market cap. Those tokens that are not bleeding out are still seeing interest. A large digital asset service provider revealed to Arca (by phone) that interest in BTC and ETH remains robust. Additionally, we learned that traditional hedge funds continue to be quiet and are sitting on cash, but miners, high net worth individuals, RIAs, and family offices are continuing to onboard, looking for ways to invest in this industry.

Thus, the overall market cap may rise even as the total number of tradable assets shrinks.

Tether Is the Best

Imagine having most of the world gunning for your head while large hedge funds constantly short your token and the DOJ and SEC harass you. How would you respond? How about by printing $1.48 billion in profits in one quarter?

Tether announced its first quarter results last week, which included a $2.4 billion surplus above the value of its USDT stablecoin (this is what’s leftover, presumably, after paying themselves handsome bonuses). They also announced yesterday that the company would begin investing 15% of its operating profits into bitcoin.

Paolo Ardoino, the CTO of Tether, stated, "Our investment in bitcoin is not only a way to enhance the performance of our portfolio, but it is also a method of aligning ourselves with a transformative technology that has the potential to reshape the way we conduct business and live our lives.”

We’ve talked a lot about why shorting USDT always makes sense from a risk/reward perspective but also will likely never really pay out. And this was before Tether became one of the most profitable companies on earth. Now that the company’s net interest margin is soaring due to higher rates and a still low (basically free) cost of capital, it will be even harder for this short to work as any wrongdoings or under collateralization in the past have easily been papered over by record and ongoing high profits. This company flat-out mints cash when short-term rates are high, which does not appear to be changing anytime soon.

But the Bitcoin component is interesting. They certainly don’t need to do this. Tether could invest 100% of their cash holdings in short-duration U.S. Treasuries, and they would still print roughly $4 billion in profit per year with arguably the simplest business model on the planet. “Just don’t mess it up” should be their corporate tagline. I don’t believe owning BTC necessarily improves their operating model at all. But it does improve their clients’ business models. Most USDT users care about and rely on bitcoin’s success. You’d be unlikely to start using USDT because you own bitcoin, but you might be around a lot longer to use USDT if bitcoin goes higher. It’s a savvy use of capital to enrich and excite your user base.

Using similar logic, Coinbase should never buy back its stock or its distressed bonds (50-60 cents on the dollar), even though Coinbase has plenty of idle cash, and both actions would be accretive. Instead, if Coinbase felt the need to generate higher revenues and a higher stock price, it could use its capital to buy smaller tokens that trade frequently on the Coinbase site, as helping to raise these prices increases their client’s net worth and personal equity, which in turn leads to higher trading volumes and revenues for Coinbase. Once again, Tether is showing the rest of the global corporate world how it’s done.

Bitcoin and Tether will forever be linked, but this explicit backing makes that bond even stronger. Granted, when they inevitably have to sell the BTC they buy, it will be just as bad for Bitcoin and its narrative as when Terra Luna, BlockFi, Elon Musk, and every other Bitcoin brand ambassador became sellers. But for now, kudos to them on recognizing their audience and what drives flows to Tether.