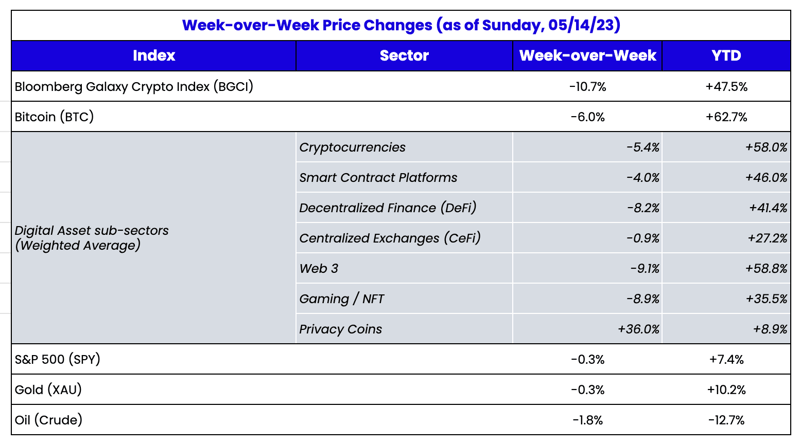

Source: TradingView, CNBC, Bloomberg, Messari

May's Market Mystery: Buy, Sell or Hold?

It’s getting pretty quiet out here. So sell in May and go away. Or maybe buy in May and go away. I don’t know—just go away, I guess, because the bid/ask is wide, market makers are leaving, and the prices of most digital assets are stuck in a wind tunnel.

In equities, it’s expensive to be short. If you don’t think an asset is going to zero, or there is no defined short-term catalyst, it’s hard to stay short when it is slow. The same goes for fixed income, which comes with an even higher cost of carry to keep shorts on when markets are quiet. But digital asset participants have historically equated “slow” with “we must be going lower” for reasons that make little sense other than the fact that slow times mean less frenzied impulse buying. And shorting is pretty cheap, given perpetual futures contracts that often move faster (right or wrong) than any negative funding rates.

Last week, it was slow again. And prices did drift lower on low volatility. But interestingly, trading activity was actually higher. Total exchange volumes were up 15% week-over-week to $525 billion, led by spot DEXs and derivatives DEXs with volumes up 26% and 28% WoW respectively.

Source: Arca Internal Estimates

The DEX to CEX spot ratio hit an all-time high, which makes sense, considering market makers on centralized exchanges are leaving in droves. In contrast, Automated Market Makers (AMMs) on DeFi exchanges are largely unaffected, as market makers aren’t forced to leave via regulation. We expect DEXs to continue outperforming CEXs due to market makers like Jane Street and Jump exiting market-making services.

In a somewhat ironic twist, 3 of the 4 important blockchain themes are on fire right now, even as interest wanes.

- Bitcoin has never been more important due to the ongoing regional banking crisis and the debt ceiling debates pushing U.S. 5-year CDS to new wides.

- DeFi has never been more relevant, as centralized market makers and exchanges die at the hands of regulation.

- Stablecoins that are not U.S.-based (Tether continues to take market share from USDC) are thriving worldwide amidst inflationary pressures and lack of government trust.

Aragon and More Problems with DAOs

I feel like I’m in a Saturday Night Live “Coffee Talk” skit with Mike Myers—“Decentralized autonomous organizations are neither decentralized nor autonomous… talk amongst yourselves.”

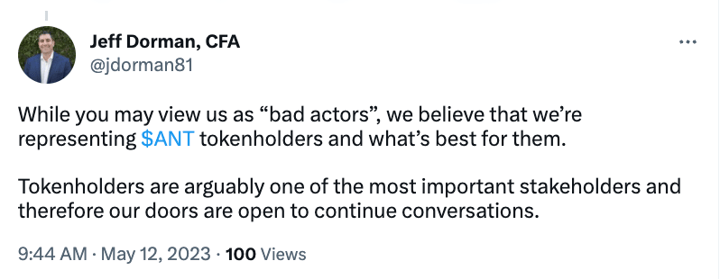

Arca has been at the forefront of DAO discussions since our inception. On the one hand, we support them; democratic decision-making on-chain is one of the main reasons we have dedicated our lives to this industry. On the other hand, they cause more frustration than any other aspect of the digital asset revolution due to seemingly endless voting mishaps and decentralized theater. This past week, another DAO, Aragon (ANT), raised more questions about the sanctity of governance.

For those not familiar with the situation, here are some highlights from Aragon’s governance debacle:

- April 2022: An initial proposal was submitted to allow token holders to oversee Aragon’s treasury directly.

- June 17, 2022: The proposal passed via a governance vote.

- November 2022: The agreed-upon timeline for the treasury to transition approached.

- February 2023: The Aragon team pushed the transition date back by 3 months.

- May 2, 2023: The first transaction of the treasury fund’s transition occurred Aragon started to ban members on their Discord channel the same day,.

On May 2nd, Arca analyst Alex Woodard was banned from the Aragon Discord channel, prompting Arca to write an

open letter that was published on Twitter. Aragon responded with a

startling blog post and

tweet thread. Some highlights below:

- Aragon accused Arca and other activist investors of staging a 51% attack. The "51%" attack narrative is factually incorrect—we are token holders (of tokens we bought off the open market), and we want to use our tokens to participate in governance. Before we staked our tokens, wANT consisted of 95% of team members who either was a founder of Aragon or had a connection to the Aragon sablier wallet. Arca staking our tokens introduced some of the first active participation by token holders. Additionally, on numerous occasions in the Discord, the team asked token holders to stake their tokens to oversee the treasury and participate in DAO governance. The Aragon team sugge a 51% attack is outright false.

- The Aragon Association 'exercised their Fiduciary Responsibility.' This is an incorrect use of the word fiduciary. Calling themselves a DAO while unilaterally going against token holders’ votes to move the treasury to a new DAO and repurpose the DAO without a governance vote is antithetical to Aragon’s fiduciary responsibility to its token holders.

- Aragon repeatedly stated that Arca was attempting to dissolve Aragon. Arca was not trying to do this. In fact, the open letter specifically states that Arca would like them to continue the buybacks that they have done in the past.

- Aragon stated that Arca was responsible for the dissolutions of Rook DAO, Invictus DAO, Fei Protocol, Rome DAO, and Temple DAO. Arca has had no investments in Invictus, Rook, Rome, or Temple. Additionally, the Fei Labs team proposed the dissolution themselves, and the Rook team initially proposed the spin-off "Incubator DAO" themselves. These "RFV raiders" pushed for the best outcome for token holders in both situations.

- Direct quote: "The letter was signed by Arca research analyst Alex Woodard, and came after a period of tension between Aragon and a group of activist investors who demanded changes to Aragon’s leadership." There were no requests for changes to Aragon's leadership—just to continue their buybacks and be open to discussing solutions with token holders.

- Direct quote: "After a recent cyber attack, the Aragon Association has decided to cancel its plans to grant voting rights to Aragon (ANT) token holders." There was no cyber attack and there has been no proposal outside of those already passed to move the treasury to the DAO, which Aragon has ignored. Staking tokens to actively participate in the protocol and governance is not considered an attack.

Aragon’s reaction was received very poorly by the digital assets community. If you read the comments and quote tweets to Aragon’s tweet, the response was largely against their unilateral decision-making. And for good reason. Essentially, Arca and a few other ANT token holders walked into Aragon with a note that said, “We’re thinking about withdrawing $80,” and the Aragon bank teller responded by calling the police, stealing the money from the vault, lighting the bank on fire, and threatening to open a new bank in a new country that no original customers could access. Yes, that analogy makes sense because it was that ridiculous. The Aragon team felt the heat, as they should have, and began to walk back their overreaction.

We’ve got a long way to go before DAOs get this right. In the meantime, I’m proud to be on team Arca fighting on the side of token holders.

Source: Twitter