Weekend Volatility Book-ended an Otherwise Quiet Week

If you only look at crypto prices once per week (which quite frankly is a good strategy), you’d notice a pattern emerging. We’ve now seen three straight weeks of positive returns, setting February up for what could be the first positive month for crypto markets since July 2018. Source: Returns are estimates fromBitwise

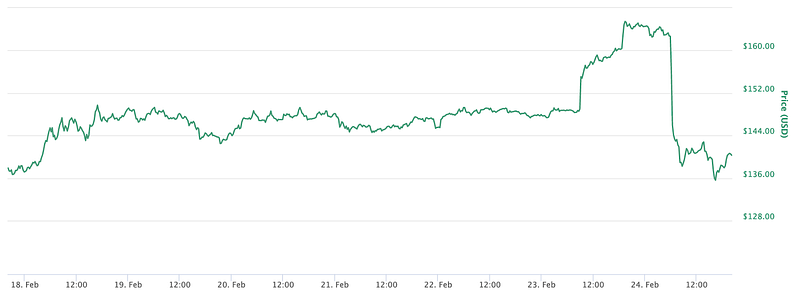

Yet it’s not out of the question that these gains fail to hold over the next 4 days, as this past week gave us another glimpse of just how volatile and violent crypto asset prices can be. In 3 out of the 7 trading days last week, the market gave us 3 separate daily moves of greater than 10%. And while most of the price action was positive (including two rip-a-thons Monday and Saturday), the week still culminated with a quick selloff on Sunday that left many digital assets 15–20% below Saturday’s highs.

Graph of Ethereum (ETH) over the past 7 trading days, with 2 large spikes and 1 massive dropSource:Coinmarketcap

To reiterate, week-over-week and month-over-month the crypto market is still much higher than where it began the prior Sunday and the month, respectively. And it’s important not to lose sight of that. From a macro standpoint, crypto is getting better and stronger. Institutional financial firms like Fidelity and Nasdaq are ramping up, pension funds and endowments are making investments, and technology firms like Abra and Samsung are rolling out consumer facing apps. Perhaps more importantly, real use cases for these digital assets are finally emerging, from a truly exciting and innovative decentralized consumer lending and borrowing boom via Ethereum smart contracts, to instant micro-money transfers via the Lightning network on Bitcoin. There is real reason to be excited again about the long-term potential of crypto assets beyond just speculation and price.

But it’s also important to remember that crypto investing is largely a sentiment game, and the sentiment over the last 24 hours has turned decisively negative. While the gains in early February showed signs of a healthy market, where price appreciation was driven by the tokens of real companies and projects that had positive events and improving fundamentals, last week’s rally saw just about every token gain including those that are largely seen as having no long-term value. That’s the danger of crypto — separating the “haves” from the “have nots” works in the long-run, but in the short-run the whole market often gets way ahead of itself. This latest runup of the “have nots” may have ultimately invalidated the whole rally, leading to the sharp decline we saw on Sunday.

The battle in crypto is navigating the short-term volatility while keeping an eye on the larger macro headwinds, all of which are positive.

Equity & Fixed Income Markets Remind us How Early it Really is for Crypto

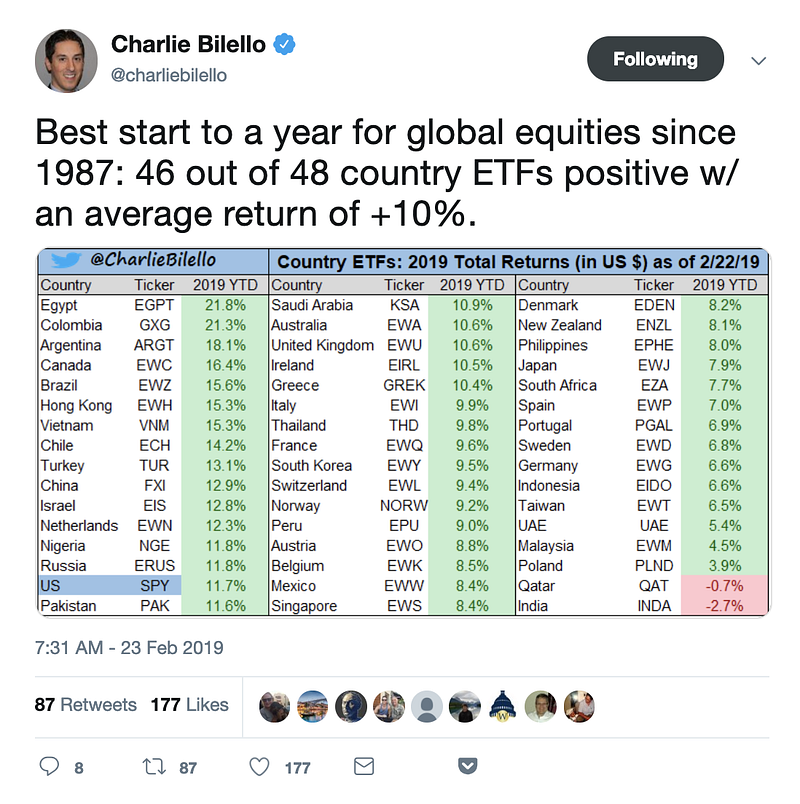

With the equity markets somehow posting their greatest start since 1987 (cough, Black Monday), and Fixed Income rallying across the board with strong High Yield corporate issuance and a Fed-induced Treasury rally, the volatility in crypto may seem like too much to stomach relative to alternative investment options. The minutes from last month’s Federal Reserve meeting showed near-unanimous support for halting the wind-down of its roughly $4.5 trillion balance sheet, which is creating another (potentially dangerous) risk-on environment.

Given this backdrop, crypto will remain in the shadows for a little while longer. But in these shadows the work is progressing… quickly. It is of course by no means certain that this giant crypto experiment will succeed. Most market participants really do understand that crypto is an experiment in monetary policy, governance, social psychology and technology — and those are difficult subjects for many to latch on to.

But each day that passes where digital assets still exist means it’s slightly more likely than the day before that this market will continue to grow and mature. And even if crypto only mildly succeeds, the upside will still be enormous. A quick look at total wealth relative to the size of the crypto market shows just how much room there is to grow with even modest adoption.

While traditional asset classes are providing comfort for investors today, and may offer most of what investors need today, it’s still worth appreciating just how early it really is for digital asset investments. It isn’t going to take much to move the needle.

Notable Movers and Shakers

Last week was not for the faint of heart. Amidst the volatility, a few noticeable winners and losers emerged.

Komodo (KMD) is up 6% last week afterreleasing a tool with the help of Amazon called Chainlizard. Chainlizard is designed to enable the creation of a blockchain in 60 seconds or less and will cost around $160 per month, much lower than other options currently available.

Binance Coin (BNB) swelled 8% last week with thelaunch of their Binance Chain Testnetand their second ICO sale, Fetch.AI, which launched today. Binance’s new chain will be used to host a decentralized exchange, many believing them to be the group to create a mainstream DEX.

Ontology (ONT) moved up 48% last weekafter releasing their development platform on Google Platform Marketplace, which is already available on Amazon AWS and Azure. Having ONT’s technology available on these cloud providers allows individuals to set up and code smart contracts without having to set up a local environment.

According to a piece published by MIT’s Technology Review, 2019 will be the year for blockchain to go mainstream, and even become “boring”. They explain that following 2017’s bull market and 2018’s crash, that real developments being made by corporations, startups and governments will normalize blockchain as a part of everyday life.

Cambridge Associatesreleased a report last weekthat advises pensions and endowments to consider an allocation to crypto. They recommend institutions take “a considerable amount of time learning about the space,” before getting involved. Cambridge advises that investors have a multitude of options from venture capital funds to buying cryptocurrency directly. It seems they havechanged their tune from 2017, when they recommended against purchasing tokens as “ much of the interest in cryptocurrencies is simply speculation”.

BitMex Research took a deep dive into what might be the cause of the next financial crisis. They posit that unlike the Great Recession, which was caused by banks, the rising rate of corporate debt and unconventional debt investment vehicles will be to blame this time.

The report covers the market landscape, different active strategies and the performance of hedge funds versus various benchmarks. We greatly appreciate their analysis on hedge fund returns and active management. Worth highlighting: “Active managers are outperforming passively holding bitcoin and large cap digital assets. We think this is a positive finding for all active managers in the industry and will help move the asset class forward for institutional investment as we develop better ways to benchmark performance by strategy.” We concur, and have stated before that active management and token selection matter in crypto.

For those who haven’t heard of Libra Tech, they are the back office engine that powers a majority of the fund administrators supporting crypto funds. Their white paper outlines the burgeoning crypto investing space and the challenges in properly accounting for crypto investments.

Last week, an Ethereum mining pool received a over 2,100 ETH as a mining reward for mining only one block (for reference the current reward is 3 ETH). Although, the source of the additional funds is unknown (current guesses include a buggy bot, accidental transaction fees or a malicious user attempting to “wash” ETH through the blockchain), the mining pool has decided tofreeze the additional ETH until the sender comes forward.

Samsung’s Newest Galaxy S10 launched last week with a special feature just for crypto enthusiasts: the phone can store the private keys of your cryptocurrency. Such a feature is exciting for the industry as current offline storage options are cumbersome to access, and the alternative of leaving private keys on centralized exchanges exposes users to hacks.

The real life use cases for blockchain continue to grow, with the LA Kings launching an augmented reality blockchain platform last week for authenticating merchandise for fans. Fans can download the app, register then snap a photo of the COA sticker on their merchandise to register it and ensure it is authentic.

Arca in the Press & on the Streets

Risk.net talked to the Arca Portfolio teamabout how they think about risk and fundamental valuation in crypto. The story is behind a payment wall but we think it’s worth paying for.

In last week’s “Reading the Merkle Leaves”, Arca’s CLO, Phil Liu, discusses the two catalysts necessary for mass crypto adoption: improved security and recoverability and a new blockchain securities settlement system.

Arca CEO Rayne Steinberg was at the Oppenheimer Blockchain Conference last week, speaking on the“Investing in Blockchain”panel about institutional focus in crypto, a panel that also featured Multicoin Capital, Delphi Digital, Sterling Global and Vision Hill Capital.

Reminder! Jeff Dorman, Arca’s Portfolio Manager, will be in San Francisco tomorrow (Tuesday, February 26). Reach out to us if you’d like to arrange a meeting.

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA — Portfolio Manager

Katie Talati — Director of Research

Hassan Bassiri , CFA — Junior PM / Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency

Subscribe For the Latest Blockchain News & Analysis

Disclaimer: This commentary is provided as general information only and is in no way intended as investment advice, investment research, legal advice, tax advice, a research report, or a recommendation. Any decision to invest or take any other action with respect to any investments discussed in this commentary may involve risks not discussed, and therefore, such decisions should not be based solely on the information contained in this document. Please consult your own financial/legal/tax professional.

Statements in this communication may include forward-looking information and/or may be based on various assumptions. The forward-looking statements and other views or opinions expressed are those of the author, and are made as of the date of this publication. Actual future results or occurrences may differ significantly from those anticipated and there is no guarantee that any particular outcome will come to pass. The statements made herein are subject to change at any time. Arca disclaims any obligation to update or revise any statements or views expressed herein. Past performance is not a guarantee of future results and there can be no assurance that any future results will be realized. Some or all of the information provided herein may be or be based on statements of opinion. In addition, certain information provided herein may be based on third-party sources, which is believed to be accurate, but has not been independently verified. Arca and/or certain of its affiliates and/or clients may now, or in the future, hold a financial interest in investments that are the same as or substantially similar to the investments discussed in this commentary. No claims are made as to the profitability of such financial interests, now, in the past or in the future and Arca and/or its clients may sell such financial interests at any time. The information provided herein is not intended to be, nor should it be construed as an offer to sell or a solicitation of any offer to buy any securities, or a solicitation to provide investment advisory services.

.jpg)

Source: Returns are estimates from Bitwise

Source: Returns are estimates from Bitwise