What happened this week in the Crypto markets?

Double-edged Sword

The crypto markets were once again fairly quiet last week. Generically, prices drifted lower on low volume following a bit of month-end window dressing the week before. And of course, most of the attention was focused on Bitcoin (BTC), which fell just 0.29% week-over-week. So for the second straight week, the narrative around “lack of volatility” in crypto continues to make its way through the ranks of market participants. It is true that Bitcoin has traded in a very narrow range for the past 2 weeks, and as a result, many alt-coins have also seen a reduction in volume and volatility. But as we highlighted last week, volatility is most certainly not gone. In fact, this past week alone, the Bloomberg Galaxy Crypto Index fell over 6%. While that may be a pedestrian move for crypto traders, losing 6% in a week in any other asset class would undoubtedly set off a near-panic.

Bitcoin (BTC) trading in a narrow range the past 2 weeks

And therein lies the problem.

On the one hand, these retail-dominated traders and speculators are constantly irritated by a lack of volatility because it reduces their ability to gamble trade. Yet, on the other hand, these same crypto participants are begging for a Bitcoin ETF and further institutional investor adoption ( we see you Yale ). Amongst other factors, institutional investors care about Sharpe Ratio — the ratio of returns to volatility. For those that want volatility to stay high, that would imply that they are banking on astronomical returns in order to keep up with the heightened volatility and keep their Sharpe Ratio above 1.0.

When we talk to CIOs and analysts at endowments, pension funds, and even fund of funds and family offices, they consistently tell us that they don’t care about 2017’s 1,000+ percent returns. They simply want an uncorrelated asset class that offers high returns per unit of risk (i.e. high Sharpe Ratios) — something that crypto can definitely achieve for them within the constructs of an otherwise balanced portfolio. For example, Thursday and Friday saw big equity declines across most global markets, and yet the crypto markets were largely unchanged, seemingly immune to the carnage abroad. So if you want volatility, you’re either aiming for returns that aren’t within reasonable expectations, or you don’t really care about institutional adoption.

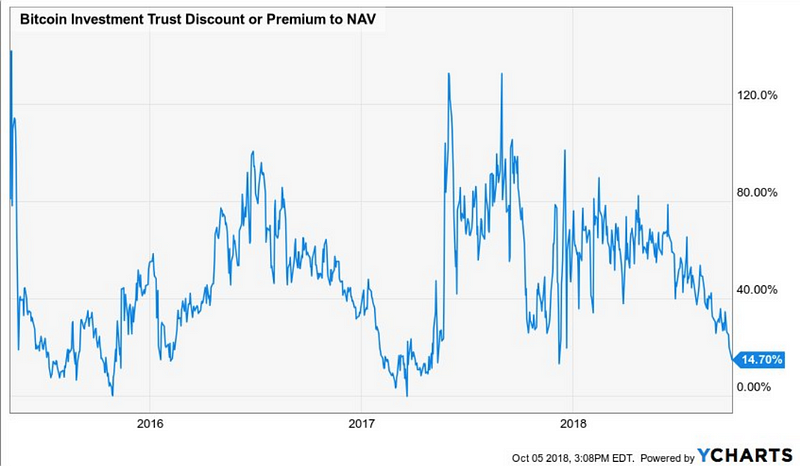

What are lower GBTC premiums telling us?

Let’s face it — thus far, most passive crypto investment products are expensive and solve for problems that don’t exist. Set aside alternative / hedge fund products for a moment, which, whether you believe in them or not, are at least designed to create alpha for Qualified Buyers and Accredited Investors through some form of actively managed strategy. What you have left is a variety of passive products that typically offer exposure to no more than 5–10 of the largest digital assets available in today’s market.

And there has been a lot of news around Crypto Index Funds lately:

- On Wednesday, Abra revealed the Bit10 token — a token tracking a Bitwise index fund.

- On Thursday, Coinable announced “Coinable Bundle” — a market-weighted selection of their five digital asset offerings.

- On Friday, Circle announced three additional “Collections” — digital asset packages that are weighted by market cap and grouped by sector: Privacy, Payments, and Platforms

Unfortunately for investors looking at these products, until digital assets become less correlated with each other, all of these companies are selling a story rather than a viable product. The majority of tokens still track Bitcoin pretty closely over a longer time horizon (rolling 90-day correlations above 0.9). So if you eliminate active management, no matter which “basket” you purchase, you are basically just buying Bitcoin.

So let’s look just at the leader in Bitcoin-specific products. The Grayscale Investment Trust (GBTC) has over $1.5bn under management, all for a product that mirrors a direct purchase in BTC. There are some legitimate reasons why an investor might prefer to own this security versus owning Bitcoin directly:

- GBTC (as a publicly listed security) is an approved vehicle for FAs and funds to buy for their clients

- Until the UI/UX improves across all “Onramp” sites/exchanges in the crypto space, many investors are just afraid to embark in Crypto purchases directly (by onboard, I mean physically transferring Fiat to a place where they can buy crypto).

- A slight premium in GBTC may actually be warranted given GBTC avoids significant risks caused by transacting directly in Bitcoin (exchange hacks, insurance, loss of private keys, etc). GBTC solves the problem of security without sacrificing the liquidity, creating value that is potentially worth more than the liquidation price of its assets.

- Many exchanges where you can buy Bitcoin impose limits on the amount of Bitcoin that can be bought at one time, and have 3–5 day bank transfer limitations. GBTC allows investors to buy and sell freely. With the volatility we see in BTC, the timing element can make a big difference.

That said, just about everyone agreed that massive premiums were not sustainable and is expecting this premium to go away at some point. The question is, now that it has, what is the reason?

Is this an indication that retail has given up on crypto? Or does this mean investors are getting more comfortable with crypto and no longer need an expensive proxy? We think the latter, which is positive for the overall industry (albeit bad for grayscale and other expensive products). While the 67% decline of GBTC this year compared to a 51% decline in BTC clearly stings GBTC investors, we’d argue that this is actually a BULLISH signal for the overall market.

Bitcoin Investment Trust (GBTC) — discounts or premium vs Net-Asset-Value

Source: Ycharts

Notable Movers and Shakers

For the 2nd straight week, the crypto market saw a mixed bag of winners and losers, with roughly half of the Top 100 higher and the other half lower. This lack of correlation is also extending beyond crypto, as global equity weakness towards the end of last week had very little effect on crypto prices.

- Ripple’s XRP token came back down to earth last week, falling 18% after climbing 70% the week before. A combination of profit taking, and some new shorts being set pushed XRP back down, but the token still remains up over 100% from its 2018 lows.

- Maker (MKR) continued its ascent, rising another 27% week-over-week (its 3rd straight week of large gains). The market is still reacting favorably to Andreessen Horowitz’s investment, which showed support for MakerDAO’s Dai stablecoin. This has ramifications for the Index world, as MKR is only included in certain indices.

- 0x Protocol (ZRX) jumped 12% week-over-week, almost all of it coming on Sunday following a widespread belief that Coinbase will be listing the token. Similarly, Tron (TRX) gained 12% on Sunday leading to a 20% week-over-week gain, after Tron CEO, Justin Sun, announced the launch of the Tron Virtual Machine (TVM), part of Tron’s latest software update, released earlier today.

What We’re Reading this Week

Old news by now, but certainly no less important. Yale’s CIO is a pioneer and a trendsetter in alternative investing amongst endowments, and this is another great data point for the institutional investing world as they continue to move into crypto.

This has nothing to do with cryptocurrency, and yet it remains a must read for all crypto investors. Marks once again takes aim at excess lending and high debt levels, which may cause the next financial crisis. How crypto will respond remains to be seen, but you certainly cannot ignore the geopolitical risks.

That sound you hear is more adoption. Retail brokerage firm TD Ameritrade has announced that it is backing new crypto exchange ErisX. How will this affect its 11mm users?

Stellar launched its completely free, transparent decentralized exchange and trading platform, StellarX, which theoretically allows for the trading of any asset. Surprisingly, the XLM token did not budge on this news.

It would appear that Puerto Rico’s Noble Bank, reportedly one of the major repositories of Tether, is having serious financial issues.

With proper discipline and respect, the future looks bright for tokenized securities.

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA — Portfolio Manager

Katie Talati — Director of Research

Hassan Bassiri , CFA — Junior PM / Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)