What happened this week in the Crypto markets?

A Sea of Red

Last month’s gains are starting to look like a mirage — as the crypto market continues to hemorrhage following a second straight week of double digit losses. Bitcoin fell 10% to $6300 last week, while the overall Crypto market cap declined by another $40B (not an insignificant number considering the entire asset class now represents just $213 bn in value).

The carnage started on Tuesday when the SEC extended the deadline of the VanEck ETF proposal to September 30th, causing Bitcoin to drop $500 intraday, and the rest of the market reacted in kind. We did not expect the SEC to approve the Van Eck filing in August nor do we expect an approval in 2018. The downward price action continued throughout the week, accelerating into Thursday and Friday. We believe we have entered a “Capitulation phase”, where many retail investors have given up on trying to recoup gains and have sold off their portfolios at a loss, unable to cope with the daily stressors of the market. This is historically the tail end of a bear market.

It is perhaps curious that Bitcoin has such a perceived dependence on the SEC’s looming decision. Cryptocurrency was the brainchild of a group of people disheartened by how ‘money’ was controlled by banks and regulatory agencies — yet here we are in 2018, nearly 10 years after the Bitcoin Whitepaper was written, watching as a regulatory agency’s decision (or lack thereof) dominates the price action of the whole market.

Elsewhere, other large cap tokens such as Ethereum (ETH), Litecoin (LTC) and Eos (EOS) were hit much harder than Bitcoin, falling between 20–40% on extremely thin volumes (more on volumes below). Ethereum is particularly interesting to watch. The majority of ICO projects raised funds in Ethereum, but these project owners have no need to hold ETH, especially in a declining market. As a result, there is a consistent overhang from these project owners looking to offload ETH in order to secure enough funds to keep operations afloat. An example of this was seen in EOS, which sold their remaining ETH in June and July of this year — a position that had initially been as high as 3 million ETH. From what we can tell, almost all of the selling pressure at these depressed prices is coming from short-sellers looking to push prices lower until they find resistance, and ICO project owners.

Low volume / wide markets — perspective on illiquid securities

At this point in time, we want to remind our readers that the Arca Funds team has decades of experience trading illiquid assets, like high yield bonds, distressed bonds, emerging markets debt, and reorg equities. It is not uncommon to buy a distressed bond on the way down at 80 cents on the dollar, 60 cents on the dollar and 40 cents on the dollar… in the same day. News comes out, prices adjust, and market participants must react to new prices that may or may not be transactable (i.e. it takes time to get to a market equilibrium where there are equal buyers/sellers on both sides).

Bringing this back to crypto, just because crypto exchanges allow anyone to see real-time prices does NOT mean that any trading is actually happening at these levels. This is an extremely immature market that is lulling people into a false sense of liquidity by showing constantly available prices that appear to be transactable, but really aren’t. Crypto is largely an OTC driven market — and that can mean very wide Bid/Ask spreads as buyers and sellers are miles apart. As a result, liquidity is thin in crypto right now. Prices of many crypto assets are falling dramatically and swiftly on little to no volume. Most of these tokens, including some of the ones that are perceived to be liquid, are moving lower without sellers. Market makers are like casino bookies — they don’t care which side wins, they just want to find a level where there is even action on both sides (so they can make their money on higher volumes). We believe illiquidity was a primary contributor to last week’s price action. The selling largely stopped two weeks ago, but there just were not enough buyers to bring the market to equilibrium — so market makers continue to test the market lower to see where the buyers will step in. When they finally step in and we touch a “floor”, there will be very little volume traded down at the bottom either as we quickly bounce back up to see if any sellers are still there at these lower levels. It takes a different approach and discipline to invest in volatile, illiquid markets — one in which we’re very comfortable.

Macro Concerns

We have been tracking several macro trends that we believe have an impact on crypto, and markets in general. The first trend is inflation and how higher commodity prices will impact digital assets (See our thoughts on commodities and oil here). Inflation is of high concern and the primary mandate for central banks who are preparing for battle by raising rates, first in the US by the Fed, and now by the ECB, as described here. Higher rates have an effect on Emerging Market economies, as their borrowing costs are more reliant on the Fed Funds rate and LIBOR than their own local rates. Hawkish policies by the Fed, ECB, and BoE have hurt Emerging Markets, as demonstrated by the recent depreciation of the Turkish Lira (-20% last week) and the South African Rand (-10% yesterday). Onerous tariffs have also been a catalyst for this move. We have been tracking correlations between crypto and other risk assets, such as EM equities, but we believe that hyper-inflation and currency volatility will drive more adoption into cryptocurrency.

Notable Movers and Shakers

The overall market fell an astonishing 21% last week, on the heels of a 15% loss the week before. Very few assets were safe in crypto, with a few exceptions and notable movers.

-

- Chainlink (LINK) was up 10.5% last week, and +20% versus BTC. The Chainlink development team has been extremely active — it’s the 18th most active project out of thousands in the last 9 months. A storm seems to be brewing in the background with this project as they gear up for mainnet release.

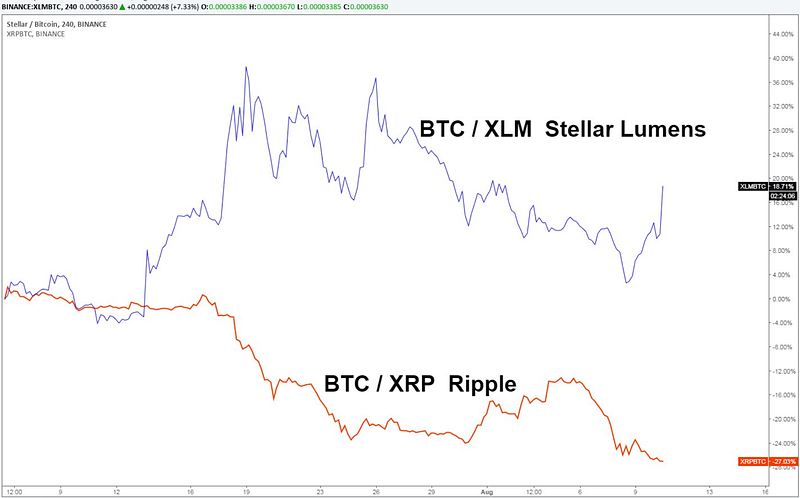

- The XRP/XLM battle rages on, with XRP falling 30% and XLM falling 9.5%. Ripple and Stellar have been classified as competitors ever since Jed McCaleb left Ripple to found Stellar in 2013/2014. While they tackle different sectors of banking (transaction fees vs. remittance network), they are always brought up in tandem for comparison. While XRP has been the dominant project thus far, it seems to be losing significant steam to XLM, as depicted in the chart below made by a prominent cryptocurrency analyst on Twitter.

- Bitcoin (BTC) dominance has now reached 50.8%, and shows no signs of slowing down. In an extended bear market such as this, Bitcoin continues to be the safe haven in the store of value debate. With markets, traditional and otherwise, suffering (see Turkish Lira and South African Rand), Bitcoin offers stability.

What We’re Reading This Week

Blockchain fatigue has begun to hit firms, as evidenced by a decline in the number of times ‘blockchain’ was mentioned on earnings calls. In 2018 companies seem to be more cautious on name dropping crypto related terms.

We’ve argued that the best is yet to come for crypto assets, particularly security tokens. Soon, the fact that you are buying assets on the blockchain won’t even be a topic of conversation, it will be assumed (much like ETFs are assumed to be the vehicle that you buy baskets of stocks now). In this case, the equity of The St. Regis Aspen Resort is being sold to investors via a new “Aspen token”.

Brave will add Twitter and Reddit support by the end of the year, allowing for users to cash in on tweets and posts. This will be done voluntarily by user donations to authors of content they find worthwhile, using the cryptocurrency BAT as payment.

According to the U.S. DEA, the use of Bitcoin is no longer primarily as a means for illegal activity. One member of the DEA even admitted they’d prefer criminals use Crypto, because of how easy it is to track via the Blockchain’s flawless record-keeping (dispelling a popular myth of crypto as a criminal safe haven).

A survey done by analytics firm Harris Insights shows the age gap of investors in both Bitcoin and cryptocurrency in general. With the extreme volatility in the new asset class, youth investors are more prone to taking a chance whereas older investors are more hesitant to take the risk. With the youth being more connected to the digital age, Bitcoin seems to resonate more so with them than other adults.

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA — Portfolio Manager

Katie Talati — Director of Research

Hassan Bassiri , CFA — Junior PM / Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)