What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

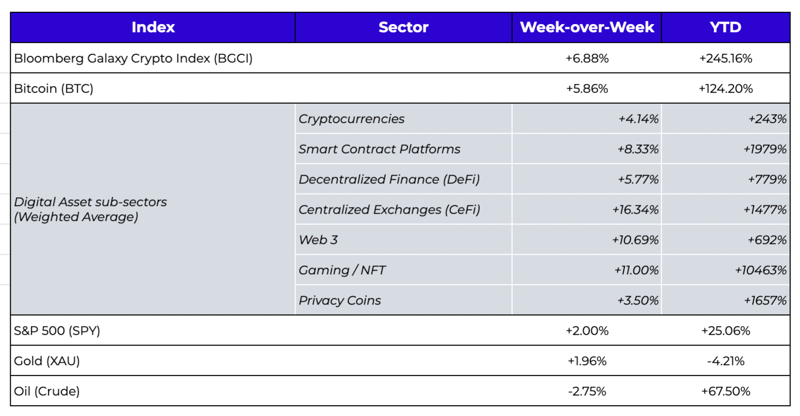

Week-over-Week Price Changes (as of Sunday, 11/07/21)

Source: TradingView, CNBC, Bloomberg, Messari

Has the Fat Protocol Thesis Been Proven?

The Fed finally capitulated and began the tapering process, agreeing to stem the purchases of Treasuries and mortgage-backed bonds. The last time we had a tapering announcement was in May 2013, and at that time, Fed Chairman Ben Bernanke surprised the market which led to a 6% decline in equities before ultimately rallying 17% from the lows to close out the year. But the Jerome Powell-led Federal Reserve does not surprise markets… at all. They are overly transparent and consistent to a fault, and it's quite-likely that the Fed-induced selloff already happened in September, when equities fell 5% amidst explicit signs that the tapering was likely.

With no surprises from the Fed, US equities once again hit all-time highs, and the VIX touched a new YTD low. Perhaps counter-intuitively, bond yields also fell across the curve, completely retracing the bond selloff that also happened a few months ago. Amidst this backdrop, it’s not surprising that many digital assets also hit new all-time highs last week. As has been the case most of the year, many different parts of the ecosystem participated.

- Gaming and metaverse tokens continued their rapid ascent, with Sandbox (SAND) rallying over 50% to new ATHs on the heels of an investment from Softbank.

- Web 3 got a jolt from Arweave (AR), which gained over 50% to ATHs as transaction usage soared, and Helium (HNT) jumped 56% to ATHs on a partnership with DISH network.

- DeFi was led by Nexus Mutual (WNXM), which gained +44% on a new governance proposal designed to put the capital pool to work.

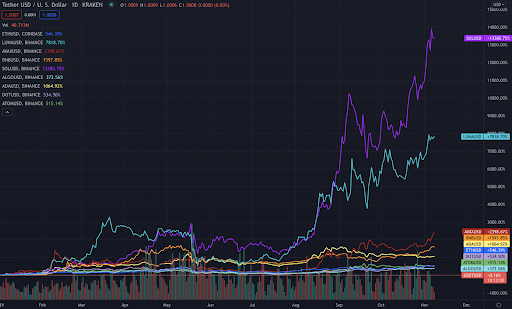

But these gains pale in compression to layer 1 smart contract platforms, which saw SOL, AVAX, LUNA, BNB and ETH (among others) march to new all-time highs last week.

YTD Price Performance of Select Layer 1 Smart Contract Platforms

Source: TradingView

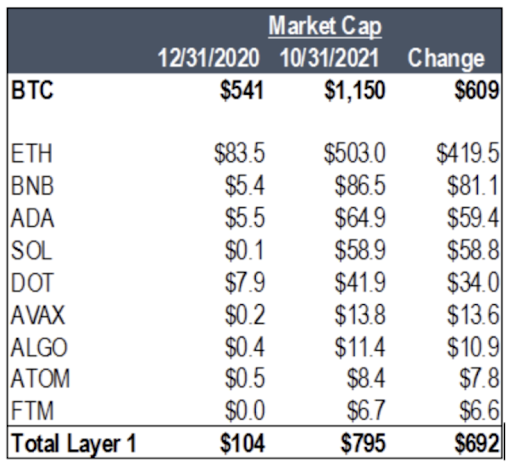

Layer 1 smart contract protocols are like the app store to DeFi/gaming/NFT apps. They are the rails on which smart contracts are built and projects can harness for their specific designs. In 2016, years before most blockchain-based apps were even created and certainly before any achieved success, Joel Monegro and others at Union Square Ventures penned the “Fat Protocol Thesis”, which essentially predicted that the protocol layer would create and capture more value than those applications built upon them. Five years later, it’s possible that this thesis has been proven. Not only has the price performance of layer 1 Protocol tokens significantly outpaced that of any other sector (other than select NFT and Gaming assets), but the total market cap increases YTD have now surpassed that of Bitcoin despite starting the year collectively making up less than 20% of Bitcoin’s value.

Source: CoinMarketCap

The data is compelling. But I’d still argue that the fat protocol thesis hasn’t been proven yet. The crazy rise in layer 1 valuations could be due to four other reasons that have nothing to do with value being captured:

- Retail and traditional investors lack the resources and skills necessary to analyze the wide variety of complex individual application tokens, so the tokens of layer 1 blockchains have essentially become the “lazy man’s index” - a catch all solution for betting on the overall growth of digital assets.

- Digital asset investing is still dominated by early stage venture capital funds, who focus on total addressable market (TAM) over financial valuation, and tend to seek out what “could be” over “what currently is”. Few technologies have higher potential upsides, so layer 1 tokens fit their strategy better. And with inflows into venture capital funds at all-time highs, the money continues to pour into their favorite investments.

- Per #2 above, layer 1 blockchain projects have raised the largest amount of money from investors, and therefore have the most money to spend on marketing - and these marketing efforts bring in investors that know little about the space. It’s not uncommon for new investors to ask about AVAX or ADA because they saw an ice cream truck advertisement in Times Square versus having actually utilized an application on Avalanche.

- In addition to marketing spend, the layer 1 blockchains are using their large cash Treasuries to create ecosystem development funds and incentive programs. This concept once again caters to the “what could be” crowd, as expectations are high that these funds will be utilized to bootstrap growth on these protocols. As our friends at FalconX pointed out, in the last two months alone, we’ve seen funds announced from FTM ($314mm), AVAX ($180mm), CELO ($100mm), ONE ($300mm), ALGO ($330mm) and NEAR ($800mm). These incentive/development programs have been a precursor to sizable runs, even though the funds themselves have yet to be deployed in a meaningful way. The average 1-day return post-program announcement for FTM, AVAX, CELO, ONE and ALGO is +38.8%, while the average return to date is +168%.

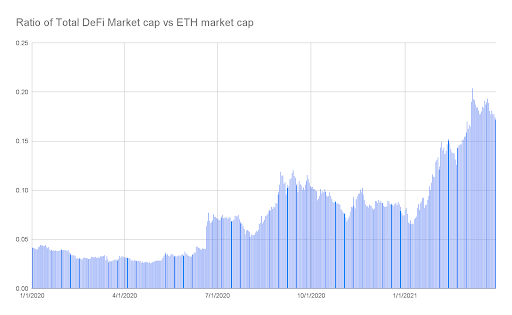

While layer 1 blockchains clearly have value, most of the value to date (outside of ETH and LUNA which have deflationary forces) comes from the fact that they cannot be valued, and thus have no ceiling. That’s attractive for long shot investing (low probability with massive upside). But eventually, the totality of applications built on blockchains has to be larger than the platforms themselves. As we continue to see more successful applications (like what we’ve seen from ETH-based DeFi, Gaming and NFTs thus far), traditional investors will flock more to these investments since they can more easily be valued using traditional cash flow analysis.

In fact, right around the time when ETH hit $25 bn market cap and $10 bn TVL (summer 2020), the first successful consumer-facing apps (DeFi) began to flourish. DeFi tokens boomed and outperformed ETH by ~7x over the next 9 months. After that, gaming and NFT apps (and tokens) built on Ethereum were the next to flourish relatively, with large outperformance versus ETH itself. Today, with so many Ethereum competitors now reaching similar market caps and TVLs, from here, these layer 1s will need a few killer apps to succeed in order to sustain their rising market caps. If these success stories happen, the apps themselves will likely outperform the layer 1s as we’ve seen historically with Ethereum-based apps. If, however, the apps don’t come to fruition, the layer 1s will likely suffer like we’ve seen with disappointing layer 1 projects like ICP, EOS, ZIL and XTZ. Either way, the risk / reward is now shifting towards the applications.

Source: CoinMarketCap & Arca Estimates

It’s worth noting that even within the virtual walls of Arca, not everyone agrees. It was pointed out recently by Connor King that layer 1 blockchain dominance in digital assets mirrors that of equities, where the largest stocks are networks and ecosystems (FB, AMZN, AAPL, GOOGL) rather than applications. While true, the counterargument is that the collective size of ALL applications exceeds that of the networks themselves. Of course the Apple app store is bigger than the biggest app, and Amazon is bigger than the biggest store, but collectively...

- The market cap of all of the stores on Amazon > AMZN

- The market cap of all of the apps on IOS > AAPL

- Thus, it stands to reason that the collective size of all of the apps on blockchains will be > layer 1s.

Similarly, Arca Senior Research Analyst, Nick Hotz, believes that the closer proxy for layer 1 value versus application value is thinking about currency value versus equity market capitalization of a country. Like equities, digital asset applications rely on the government (layer 1) to provide a medium of exchange, rules of the road and security. Essentially, this means that layer 1 blockchain tokens represent the country, but unless there are thousands of stores, restaurants, schools and housing in the country, the country itself becomes worthless. This makes sense. In the US for example, broad money supply is worth about $20T while equity capitalization is $50T. And that ratio should vary based on how much value that government (layer 1) is providing to its native apps.

While the fat protocol thesis has been a very profitable and ahead of its time idea, the reason these investments have worked so well for investors to date is largely due to a lack of alternative places to invest, and a lack of traction from the applications themselves, not necessarily value capture.

Stablecoin Regulation

On Monday, the Presidential working group on financial markets (PWG) released a long-awaited report on stablecoins. The 22-page report from the PWG included thoughts from members of the Fed, SEC, CFTC, FDIC and OCC. In essence, the report attempted to set forth the risks associated with stablecoins, and set the table for an inevitable showdown. Each of these protection groups seeks more authority from Congress to regulate, and requests that Congress pass clarifying legislation to establish a cohesive regulatory framework.

The digital assets community had mixed feelings with regard to the report. In our opinion, the report was fairly balanced, and did not introduce much in the way of new information. The digital assets market reacted with a sigh of relief, ultimately trading higher simply due to the lack of landmines.

We believe there were four main takeaways:

- While the report centered around the risks that stablecoins pose to the traditional financial system, the opposite is more likely true. The financial system poses more of a risk to stablecoins than stablecoins pose to the traditional financial system since a shock to the traditional system would result in lower underlying collateral (i.e. if commercial paper prices fell or certain high-quality issuers of CP defaulted). Ironically, a run on the bank in stablecoins that regulators are so fearful of would likely only be triggered by the regulatory pressure itself.

- That said, regulating stablecoins does make sense, more so than almost every other form of regulation currently being debated. Regulation is not a bad word -- if regulators can clearly articulate what it is they want stablecoin issuers to do in terms of FDIC protection, underlying asset mix, and standardized disclosures…. most stablecoin issuers would happily follow the rules. The market welcomes a clearly articulated roadmap.

- Stablecoins have perfect substitutes. There are no differences between them, so if one fails to comply while another does comply, there will be no overall market disruption as investors and customers will move seamlessly from one to another (no different than how derivatives investors left Bitmex to go to Binance/FTX).

- Tether is no more or less risky than USDC and every other decentralized stablecoin. This is not, and should not be, a witch hunt. Any frameworks that result will apply equally to all stablecoin issuers.

It will take years for these new laws and regulations to take shape. But in the meantime, it’s encouraging to at least see the efforts of regulators focused in the right place.

What’s Driving Token Prices?

- SLP (+19): Katana, the Ronin decentralized exchange went live this week. Katana allows anyone to easily swap between the various assets within the Axie Infinity ecosystem which are AXS, SLP, USDC and WETH. Currently total value locked on Katana has exceeded $1B, including $546M for WETH, $325M for AXS, $216M for SLP and $4.65M for USDC. More importantly, SLP is amongst a handful of assets that can be used to farm RON.

- AURY (+62%): Aurory team successfully raised over $113M through its seed round, NFT sales, and IDO. One of the major Play to Earn games on Solana, AURY is about to release its game in Q1 2022. Aurory is one of the most hyped role-playing games (RPG), with backers such as Alemeda Research and CMS Holdings.

- SAND (+67%): After announcing a $93M Series B round led by Softbank, Sandbox continued to benefit from the momentum around the Metaverse space with Microsoft, Nike and other brands announcing their intention to get into the space, taking the lead from Facebook/Meta.

- AR (+52%): Arweave has seen a huge increase in transactions as more projects on Solana use the platform to permanently store NFTs. In addition, an investor released a valuation on Arweave pricing it at $150B, (currently $3.8B), comparing it to AWS.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - PM

Alex Woodard - Research Analyst

Andrew Stein - Research Analyst

Nick Hotz, CFA - Research Analyst

Wes Hansen - Director of Trading & Operations

Mike Geraci - Trader

Kyle Doane - Trading Operations

David Nage - Principal, Venture investing

Michael Dershewitz - COO of Arca Funds

To learn more or talk to us about investing in digital assets and cryptocurrency