Source: TradingView, CNBC, Bloomberg, Messari

A Strange and Uneven Selloff

Most of the week was uneventful, if not positively biased, until Friday when a strong selloff quickly and swiftly pushed the market lower. But you wouldn’t know it even happened if you only looked at week-over-week prices.

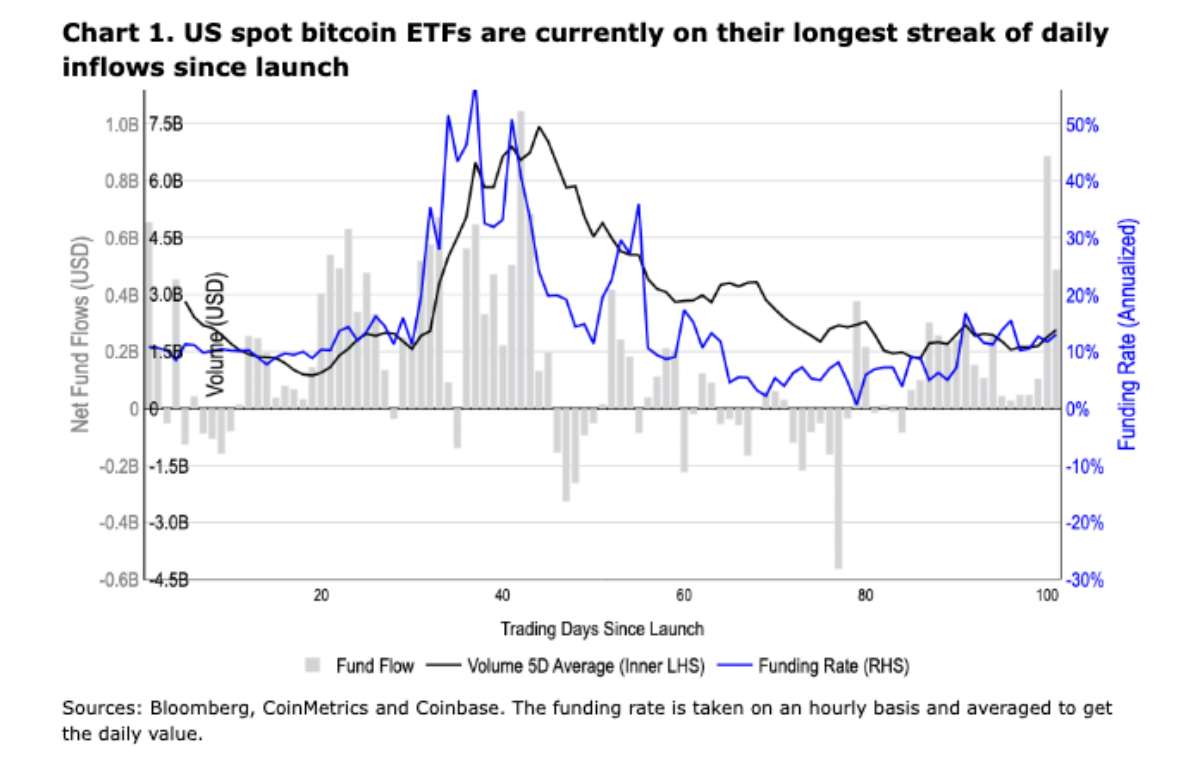

Bitcoin ETF flows continued throughout the week after a huge day on Tuesday, which gave participants incremental confidence to buy upside. In fact, according to Coinbase, the BTC ETFs now have 16 consecutive days of inflows, equivalent to the previous longest inflow streak between January 26 and February 20, shortly after the initial ETF launches. The total magnitude of inflows in the present streak has been comparable to the previous streak at $3.6 billion versus $4.4 billion, with meaningful price appreciation occurring over both periods. BTC appreciated from $40K to $52K BTC (+30%) during the Jan/Feb streak and from $61K to $71K (+16%) in the current May/June streak.

The problem, as has been the case for most of the year, is that inflows are almost entirely coming into BTC, and BTC only. While this has a trickle-down effect, it’s a completely different dynamic than we saw in 2020 and 2021, where the capital came directly to other parts of the market and into more broad-focused crypto funds. Market advances have been shallow without direct inflows into other market areas, and liquidity has worsened.

Liquidity and volume remained low last week outside of BTC and, to some extent ETH. This is exacerbated further by the attention on the macro calendar, as most macro traders focus only on BTC and ETH. While the macro backdrop appears encouraging, Friday's mixed NFP report offered no confirmation to the market that the Fed will cut rates, even as both the Bank of Canada and the ECB began their easing cycles last week. All eyes will be on the Federal Reserve meeting on June 11-12, and once again, all market participants are focusing on the same data. The upward trend exhausted pretty quickly by the end of the week, leading to sizable sell orders coming through, which muscled the market lower, triggering algos and forced liquidations. But again, the BTC ETF inflows muted any pain in BTC, so most of the pain was felt in altcoin land with some nasty wicks lower. Many tokens were down as much as 20-25% in the brief period following the Friday selloff.

The typical large open interest flush pattern played out for most coins - initial large wick lower, relatively strong initial rebound, sellers on the rebound, which pushes price lower again, and then bleed on low volume. Total open interest is down over 10%, so the market structure is set up nicely for an upward trend to resume this week. The last time open interest fell this much was at the end of May when prices rebounded strongly over the course of the next three days but then revisited the lows and traded sideways over the following week.

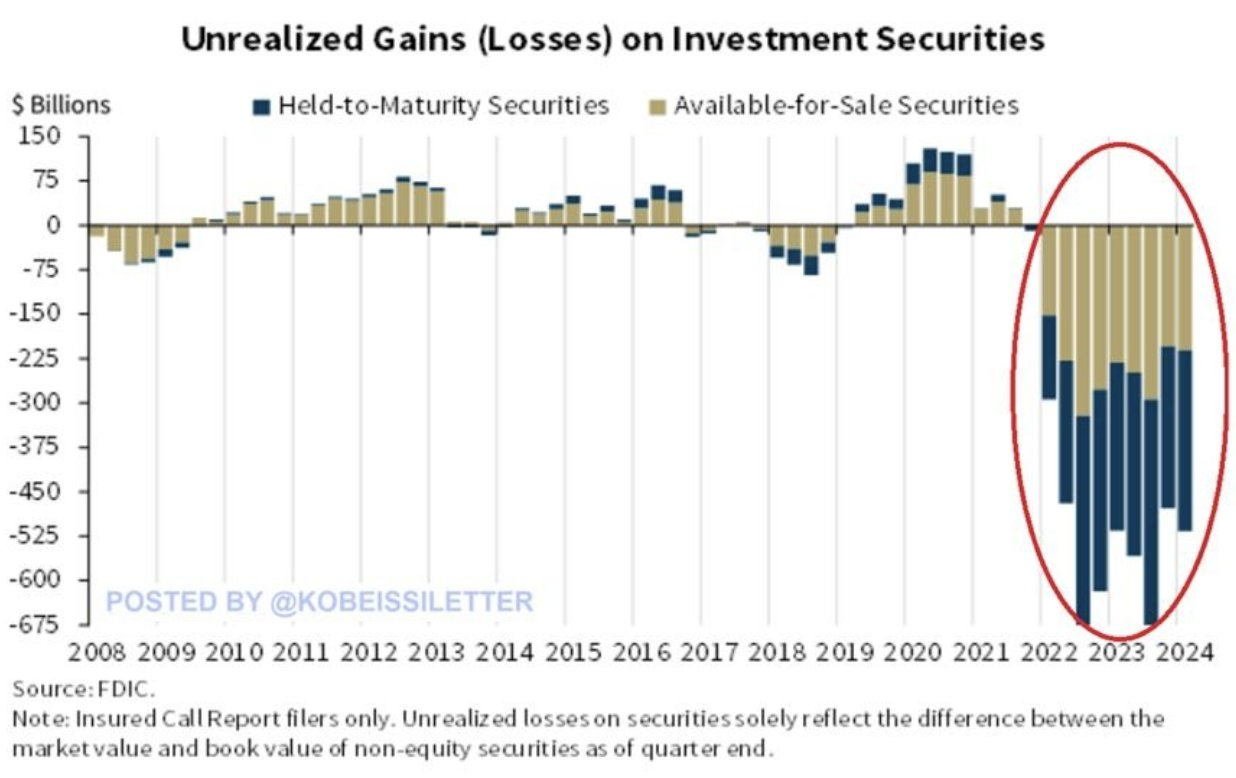

More Regional Bank Issues?

In its

Quarterly Banking Profile report, the FDIC says banks are now saddled with more than half a trillion dollars in paper losses on their balance sheets, with 63 lenders on the brink of insolvency, due largely to exposure to the residential real estate market.

Source: FDIC

It wasn't that long ago (March 2023) when 3 regional banks failed. While customers of these banks did not suffer losses because the government stepped in and backstopped deposits, there was a 3-day period over the weekend when customers of these banks faced real, unknown fears. Many bank customers feared they would be unable to get their money out of the bank, and small business customers feared they could not meet payroll and vendor obligations. I received calls from 4 small business owners that weekend, asking what they should do, specifically inquiring about Bitcoin and other bearer assets.

March 2023 was a reminder that your assets in a bank or brokerage account are not actually your assets but rather a liability of your bank, brokerage, or the government, and

it's up to them to decide if you will get your money back. While those of us in the U.S. feel safe due to our government's size and historical leniency, others worldwide don't feel the same way. They know that their money is not always their money.

The recent FDIC report does not mean we are about to have another regional bank crisis. Banks can handle unrealized losses for a long time as long as:

- a) customers don't flee

- b) equity holders don't dump their shares.

However, both (a) and (b) are real risks that could happen without a moment's notice due to the speed of online banking and equity trading. This is a non-zero risk. It's a good reminder why hundreds of millions of people worldwide and a few companies are beginning to put some of their assets into crypto, where they can safeguard and custody the assets themselves.

Owning your assets feels a lot different than hoping your bank, brokerage, or custodian will return them.

Source: Coinbase

Source: Coinbase