Source: TradingView, CNBC, Bloomberg, Messari

Theories On The Next Move Higher

I spend a lot of time trying to distinguish signals from noise. This year, most newsworthy events have been noise. The few exceptions:

- The March regional banking crisis in the U.S. was an undeniable boost for Bitcoin, as it reminded small business owners, high net worth individuals, and regular depositors why a bearer asset is important, and once again weakened the perception of banks and governments.

- Blackrock’s announcement in June that they had applied for a Bitcoin ETF was an undeniable sentiment shift, as it gave digital assets investors hope that TradFi institutions were still very interested in digital assets.

- The SEC’s back-to-back losses in court versus Ripple and Grayscale undeniably gave the industry some hope that this industry could continue to grow even in the face of a hostile regulatory environment.

By my count, that’s about it in terms of meaningful events this year that have driven markets. There have been a few other interesting topics (i.e. the rise in liquid staking derivatives, the ability to invest high cash balances into treasuries on-chain, and the growth of Base and other Layer 2s), and a few other announcements that may matter in the future (i.e. Paypal and J.P. Morgan using crypto for settlement, continued investment in web3 gaming, potential ETF inflows once a spot ETF is actually approved), but these have not been market moving events.

But it is possible that we are now embarking on the 4th significant event for the digital assets market. While recession fears have been pushed out from 2023 to 2024 at the earliest (and possibly not until 2025), and corporate balance sheets remain healthy, government balance sheets are definitely not.

Per the IMF, total global debt stood at 238% of global GDP, 9% higher than in 2019. In U.S. dollar terms, debt amounted to $235 trillion, or $200 billion above its level in 2021. Most of the growth in debt is coming from the public sector, as the events of 2008 and 2020 (pandemic) did not erase corporate and household debt, but instead replaced it with more government debt.

In the U.S. alone, Federal debt is $33.5 trillion, and is jumping by $40 billion per day. At the current pace, the U.S. would add $1 trillion in Federal debt every 45 days. Since 2008, the U.S. has added $24 trillion in Federal debt, rising to 3.8x what it was in January 2008. Total U.S. debt is now officially up more than $2 trillion since the debt ceiling crisis "ended." As spending is going up, U.S. tax receipts are down 8% over the last 12 months. This is an unsustainable path.

Worse, interest expense is skyrocketing, which only adds further fuel to the rising debt balance. The Interest Expense on U.S. Public Debt rose to $883 billion over the past year, another record high. If it continues to increase at the current pace it will soon be the largest line item in the Federal budget, surpassing Social Security.

As a result of both the rising debt, and rising rates (which will presumably slow growth), some prominent investors have been calling both the stock market and bond market basically uninvestable. Bill Gross is

shunning bonds and stocks. Paul Tudor Jones is back

pitching Bitcoin and gold. For those keeping score at home, that doesn’t leave a whole lot of other options for liquid investments. This is not to say that money will begin flooding into digital assets, but the stars are aligning for the first time in 18 months. A Bitcoin and Ethereum ETF are likely getting approved by year-end, while at the same time investors

continue to take a beating in the 60/40 portfolio.

Admittedly, most of the excitement is around potential inflows, not higher usage. But they are related. Inflows lead to higher prices, which often reflexively leads to more activity and higher usage. And while the rest of the industry is cooling, it’s far from dead. Stablecoins still account for the majority of wallet activity in crypto at over 40% of overall active address activity. And DeFi ranks next on that list with about half as much activity, but certainly high enough to disprove the theory that "DeFi is dead" and no one uses it.

Growing, unsustainable debt balances are nothing new. But digital assets tend to get a bid every time the market loses faith in banks and governments. And that is happening again right now.

Binance Is Still A Sensitive Topic

Going back to the “noise” category, just about everything surrounding Binance post the FTX collapse has been just that. A plethora of influencers have been spreading "imminent Binance takedown" concerns for most of the year. They may need to wait even longer.

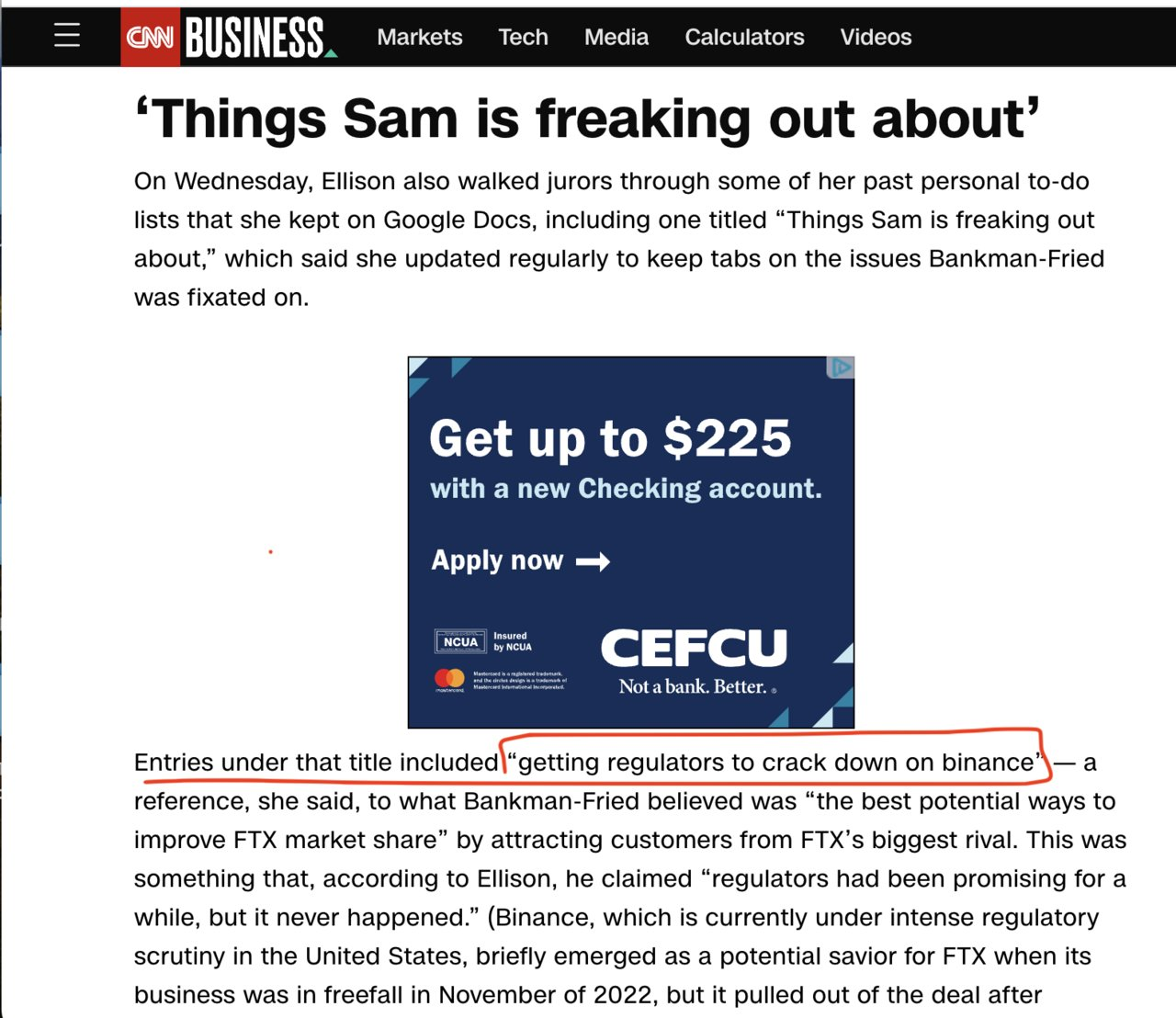

It’s been widely expected that the DOJ will eventually

bring charges against Binance. But Arca’s legal team has been surprised at how long this has been taking and how little movement there has been in this case. We may now know why there's been no recent movement in the DOJ case against Binance - prosecution evidence was likely provided by SBF and is now tainted (and unusable). Per the Sam Bankman-Fried trial:

Source: CNN

With the recent revelation from the Sam Bankman-Fried trial, we now believe that a big part of the DOJ’s case against Binance came from SBF (or other FTX) evidence. Any evidence (like trade ops info, not testimonial) that SBF/FTX might have provided to the DOJ will be discredited. The standard of proof in a criminal trial is "beyond a reasonable doubt". Given the amount of fraud coming out in this trial, nothing that SBF may have fed to the DOJ will be able to meet that standard. So the evidence will be unusable at trial (even if he gets acquitted, there will still be "reasonable doubt" about anything provided by SBF/FTX). There is also the hearsay rule that could limit the use of a defendant's testimony in another case.

It’s highly probable that SBF had been secretly feeding DOJ "evidence" for a criminal prosecution against Binance. Now his motives for doing that will create "reasonable doubt" as to the truthfulness of the "evidence" he was providing.

Those shouting from the rooftops about Binance’s demise may get hoarse.