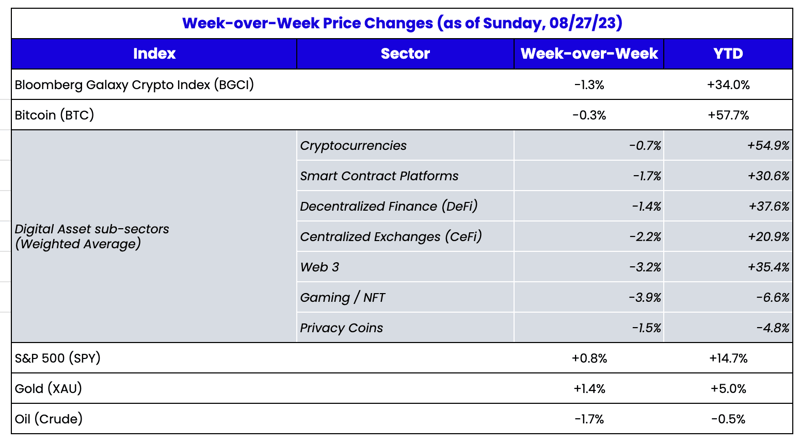

What happened this week in the Crypto markets?

Source: TradingView, CNBC, Bloomberg, Messari

How ETH Changed My Opinion in 2018

If you were expecting fireworks last week, you didn’t get them. Following the largest long liquidation of the year and subsequent price decline just one week ago, last week, most digital assets settled right back into a low volume, low volatility, range-bound trade. Total exchange volumes dropped by 20%, back in line with the average over the past two months, in contrast to the elevated trading volumes during the crash. The lackluster week-over-week price action is nothing new. We’ve now had a completely lackluster 12-month period. Take Ethereum (ETH) for example. As pointed about by

Messari and

Bitwise:

ETH Price Flat Year-Over-Year

August 22, 2022: $1640

August 22, 2023: $1640

Source: TradingView

Now, this by itself is not noteworthy. There are always ups and downs in crypto markets, and any arbitrary 1-year period can look like this. But, this is noteworthy because of how much Ethereum has changed over the last 12 months. This includes:

- A completed and “hiccup-free” ETH 2.0 merge

- A successful rollout of L2 SDKs (OPstack etc)

- Multiple zk-EVMs launched

- Hundreds of thousands of new contracts deployed on mainnet

- ETH staking rates rising from less than 10% to over 20% helping lock up significant supply

And last week marked the first deflationary year in ETH's history.

Total ETH outstanding supply:

August 23, 2022: 120,224,061

August 23, 2023: 120,213,931

Prior to the ETH 2.0 merge in September 2022, the amount of ETH in the world increased steadily at roughly +5% per year due to mining rewards. However the culmination of the entire ETH 2.0 roadmap changed this trajectory, allowing the fees paid to use the Ethereum network to be consumed by the blockchain itself. And these fees were

not insignificant.

ETH is now destroyed whenever Ethereum is utilized and can possibly be considered the most impactful tokenomics upgrade ever. Since these changes went into effect (the fees started to get burned in 2021, but the impact was not felt until the merge in 2022), the total amount of ETH in the world started declining, because (on average) more ETH is consumed in user fees each day than is produced by the blockchain. Again, as

Matt Hougan at Bitwise said,

“Think of ETH as a commodity. Like all commodities, its price is set by supply and demand. Supply is now falling because lots of people are using the new commodity. If demand to use Ethereum-based apps continues to grow, it could be interesting.”

In December 2018, towards the end of one of the longest bear markets on record, ETH was trading at $80. I remember saying at the time that ETH was not valuable. To clarify, I thought it was useful, but not valuable. If you believe ETH is a commodity, at that time, it was Aluminum – very useful, but not at all scarce or valuable. Basically, I thought ETH (as an investment) was dead, and it didn’t take long for me to realize how wrong I was. Of course, those closer to Ethereum who saw what was being built on it didn’t share my view. To them, ETH at $80 became a generational buying opportunity since the price was not correctly tracking the fundamental usage.

In just a few short months thereafter, ETH rose to $300. Fast forward to just 2 years later, and the price of ETH was over $1,000 at the end of 2020 and surpassed $4,000 in 2021. In just a few short years, everything I thought I knew about Ethereum’s native token was upended. Stablecoins, DeFi, and NFTs provided a massive boost to the blockchain’s usage, and the upgrade events in 2021 and 2022 (which had been planned and telegraphed for years), created real economic value tied to this increased usage.

Source: TradingView

The point is, following a long period of despair and downward/sideways price action, a technology asset that looked dead very quickly became the single most important asset in the entire asset class. A lot can change in a short period of time when dealing with new technologies.

With that in mind, ETH price now looks dead once again- even though nothing could be further from the truth in regards to its importance and economic trajectory. This begs the question: how many other blockchain protocols and applications look today how ETH looked 4 years ago? Most likely, there are many other tokens that are generational buying opportunities even if they look dead to the naked eye.

NFTs and Other Cool Use Cases For Blockchain Applications

If you’ve followed my musings for the past five years, you know that I believe every company, municipality, and university will issue a token one day. I believe that investment banks are asleep at the wheel for pitching debt and equity financings when, in many cases, the more obvious (and much cheaper cost of capital) solution is to launch a token.

Many companies are starting to get on the NFT bandwagon (Coca-Cola, Starbucks, Reddit, Nike, etc.) but have yet to issue a pass-thru token at the company level. Citibike in NY is the

latest to jump on board, and this is a pretty cool idea for New York City, and making me wonder what other ideas will be next.

I always thought someone should write a book with a huge cliffhanger, and if it's successful, charge for the ending and don't release it until you hit this threshold. Imagine if J.K. Rowling had given the first 5 books away for free, but charged for the final two books? Here’s an ex-Alameda Research employee who has

created a lot of interest in a future part 2 of his story working for Alameda. What if he created a token, and said that he will only write part 2 if he generates $50,000 in token sales, and set up a smart contract whereby the next iteration is released to token holders only upon hitting this $50,000 threshold? Tokenholders could also be privy to a portion of future proceeds should they try other ways of monetizing their story (i.e. writing a book, a Netflix special, etc).

We’ve barely scratched the surface of how companies, individuals, and entities can use tokens. To think this industry is dead simply because prices are stagnant is a huge misunderstanding of the potential usage.