Source: TradingView, CNBC, Bloomberg, Messari

A Little Bit of Buy Interest

These days, the digital assets market will take what it can get. Last week’s modest rally was a much-needed break from the constant selling pressure we’ve seen over the past few months. More importantly, it was led by assets other than Bitcoin. Bitcoin rose +8% week-over-week, outperforming ETH and SOL (+2% each), but lagged many other tokens in sectors like DeFi, AI, and Gaming. Now, this wasn’t an all-out “

alt rally” by any means, but for what feels like the first time since March, a few tokens that would be considered “higher quality” tended to outperform. However, as is the new recent norm, this had very little to do with crypto itself, and more to do with macro.

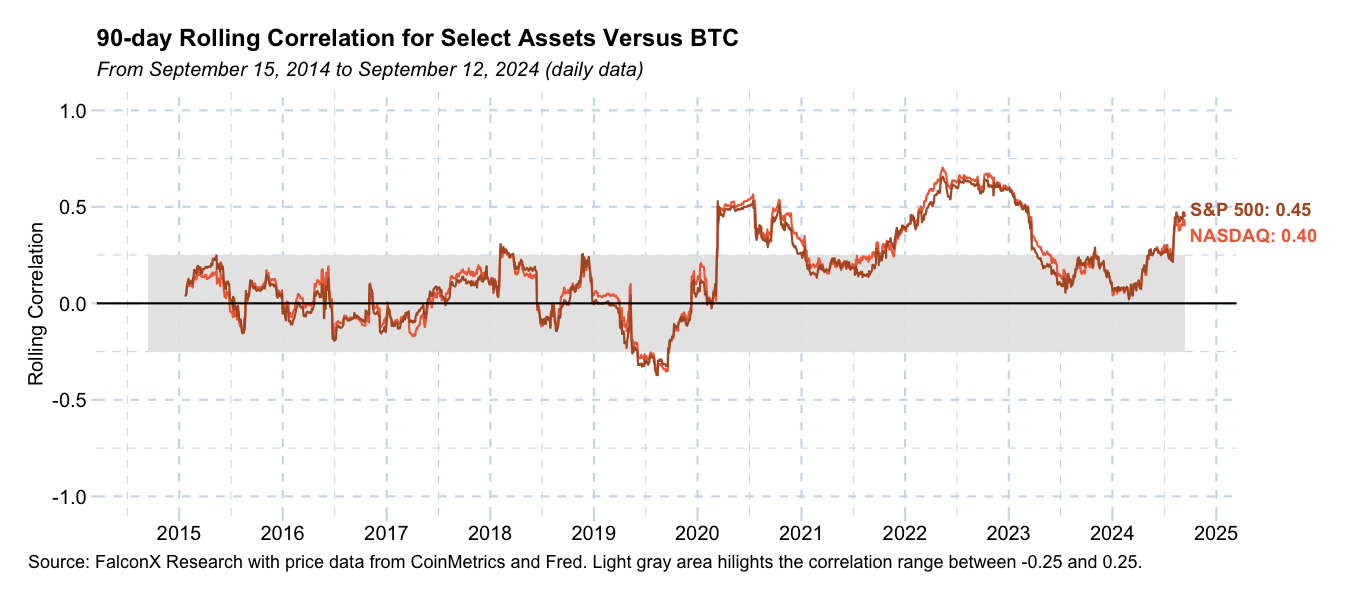

As FalconX pointed out over the weekend, correlations between Bitcoin and the leading broad equity indices (S&P 500 and the Nasdaq) are approaching levels not seen since the mid-sized banking crisis in 2023. While correlations had been near-zero for most of the past 18 months, the upcoming election combined with the FOMC’s imminent rate cutting regime are driving price action. And since the rest of the digital assets market is currently just following Bitcoin rather than its own achievements, this graph looks similar to just about any crypto asset.

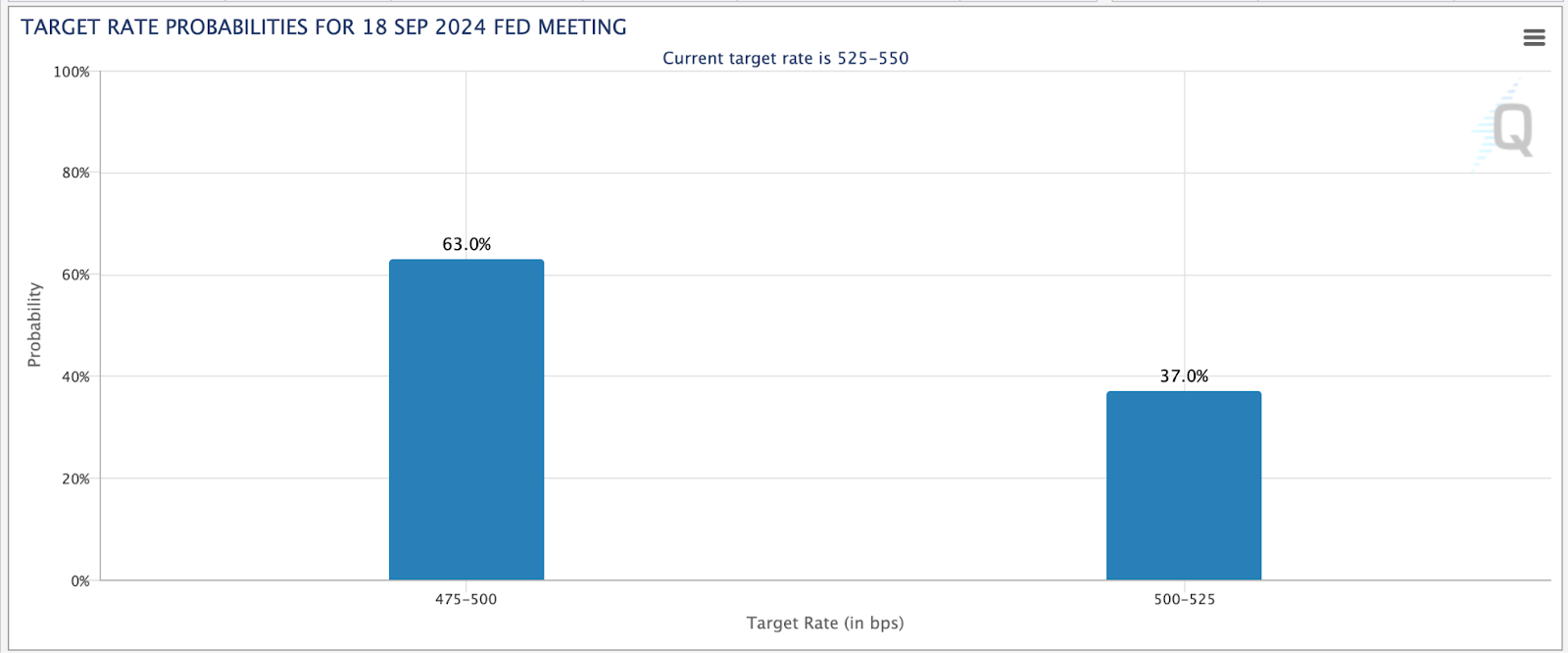

It is likely that the Fed will cut rates by 25 basis points this week at the September FOMC meeting. As of last week, the market was only pricing in a 20% chance of a 50 bps cut, then Friday this jumped to 43%, and as of Monday morning, this has jumped to 63%. Those in the 50 bps camp are REALLY stretching in my opinion.

While some parts of the government are inconsistent, like the SEC, which continues to get called out for blatant

double-speak, the Fed is an entirely different animal. The Jerome Powell-led Federal Reserve is the most transparent Fed in my three-decade investing history. They do not throw curveballs. They often get projections wrong (like the expected 75 basis points of hikes in 2022), but they don’t intentionally mislead. There were days back in the early 2000s when you would have no idea what to expect from a Bernanke or Greenspan-led Fed. The FOMC meetings were actually quite riveting because you simply had no idea what to expect. But not the Powell-led Fed. They often explicitly tell you what they will do, but in rare cases when they don’t, they leak it to their favorite Wall Street Journal puppet,

Nick Timiraos, who spells it out for you. And there have been no indications that the Fed is going fast and furious. Feel free to tell me I’m wrong if we get a 50bps cut this week. I’d be shocked if it happens. Either way, it’s the first FOMC meeting in a decade that is going to leave some people surprised.

How to Describe Digital Assets to Our Friends

Despite calls for a “bull cycle”, it’s been pretty clear for months that digital assets are not serving as great investments so far this year. Often, price leads the narrative rather than the other way around, and the price has been nothing but down recently. When that happens,

sentiment sours fast, participants in this industry tend to get REALLY negative, infighting between communities becomes prevalent, and many start to lose hope. It’s not uncommon for people to forget how far digital assets have come in just a short 5-10 year span, focusing instead on how little has been accomplished in recent weeks/months. As Bill Gates once said (paraphrasing), “people tend to overestimate what can be achieved in a year and underestimate what can be achieved in 10 years.”

As Chief Investment Officer for a crypto-native fund for the past seven years, I’ve had thousands of meetings with investors, trying many different analogies and descriptions to best educate newbies and help them understand this new technology. Below are some of the explanations I’ve used that have resonated the most with new investors and helped me see the forest through the trees.

Valuing Bitcoin:

Bitcoin is hard, if not impossible, to value. It most certainly has value, but quantifying that value is difficult. However, businesses that derive value from Bitcoin, like Bitcoin miners and exchanges, can be easily valued as long as you operate under the assumption that Bitcoin does indeed exist (which it does). Bitcoin itself has always been a call option on anarchy if citizens begin to lose faith in their banks and local governments. It is either worth $0 if Bitcoin ultimately fails, or it is worth tens if not hundreds of trillions of dollars, and any price in between simply reflects a probability-weighted outcome of achieving one of these two extremes. At a current market cap of just over $1 trillion, the market is pricing in a roughly 5-10% chance of achieving success in the future.

Perhaps the best way to value Bitcoin under this model is by treating it like a

credit-default swap (CDS) contract on global government debt. If you just look at the U.S. by itself, by buying Bitcoin, you are buying default insurance on the USA for a significant discount to fair value as indicated by the cost of Bitcoin compared to the cost to insure against all U.S. liabilities. But equally important, buying Bitcoin as insurance also covers you against defaults on ALL other government obligations.

There is roughly

$100 trillion of combined global government debt, plus trillions more if you include off-balance sheet and unfunded long-term liabilities. Add in global bank debt, which is essentially backed by governments anyway, and the numbers become staggering. Suddenly, paying a 1-time fee of just under $60,000 for Bitcoin doesn’t seem that expensive. Perhaps we should stop looking at Bitcoin as an inflation hedge or store of value and start valuing it as wealth and livelihood protection.

Layer-1 Smart Contract Platforms Are Just App Stores

Both iOS and Ethereum started as blank canvases reliant on the creativity of outside developers to find success. At the same time, both Apple stock and the ETH token had speculative value in anticipation of future success. Today, both are thriving ecosystems where the growth of apps, users, downloads, and transactions create revenue (Apple) and fees (Ethereum) that accrue to AAPL shareholders and ETH token holders, respectively.

Newer Layer-1 apps (like Solana and TON Network) are like the Apple iOS competitors, such as Android. Don’t get too caught up in which is which (I know Android is bigger than iOS, and maybe Solana is iOS and Ethereum is Android…whatever). The point is there are multiple “app stores” via the iOS and Android ecosystems, much like multiple blockchain app stores across different blockchain platforms.

Layer 2 Side-Chains Are To Ethereum as Automobiles Are To Oil

This one was

not my own, but I have found it useful to explain to new investors. The most recent hatred for Ethereum stems from the growth of Layer 2 side-chains, like Base and Arbitrum. When analyzing ETH as an investor, the most important thing to pay attention to is the network effect of ETH, the asset.

Layer-2 side chains drive demand for ETH, the asset, because you need ETH to transact on them. The growth of L2s simply adds to Ethereum’s usage, similar to how the growth in automobiles leads to increased oil/gas usage.

Now, if one were to analyze an oil producer as an investor, the rising demand for electric cars would negatively affect oil usage. Similarly, if L2s start to use their own native tokens for gas, then ETH becomes less useful as the oil.

Ultimately, Choosing a Layer-1 Blockchain Is Like Choosing Gmail vs Yahoo – It Doesn’t Matter

Because digital assets are still relatively young and because you can make (or lose money) by betting on the right blockchains, there is a lot of tribalism in the crypto markets: ETH vs. SOL, AVAX vs. TON, BNB vs. TRX, etc.

But ultimately, none of this matters. By the time non-crypto consumers start using blockchain regularly, no one will even know what chain they are using. Interoperability standards will make moving between blockchains seamless. Consider how we use email today. One standard protocol (SMTP) exists, but consumers can use different interfaces (Gmail, Yahoo, Hotmail, Protonmail, etc). The same applies to internet protocols (http) and the various browsers you use to access this protocol (Safari, Chrome, etc). Imagine a world where a Gmail user couldn’t interact with a Yahoo mail user or where picking one email provider actually dictated what you could do online. It would be ridiculous. But that’s where the blockchain world is today – where a Solana user can’t easily interact with an Ethereum user. This will soon change through operability, and most know this, yet they still think the chain itself matters.

Moreover, much of the debate over which blockchain to use stems from the fact that the apps themselves aren't that popular yet. Could you imagine if your Citi, Paypal, or Venmo app was only built on iOS or Android, but not both? These are popular banking apps, so of course, there are different versions for different operating systems so that these companies can access as many consumers as possible. Maybe a company chose to build on iOS first or on Android first. Still, ultimately, if it is a successful business, it will build multiple versions rather than risk alienating and ignoring a huge consumer base on another OS. Similarly, once a crypto app becomes popular, it will move on to other chains, regardless of how it started.

- Uniswap is the most popular decentralized trading platform. While it was originally built on Ethereum, it is now accessible on multiple chains.

- Tether (USDT) is the most popular stablecoin, now with a $118 billion market cap. Of course, Tether is now multi-chain as well, with Tron and the TON network challenging Ethereum usage.

So, let’s not get too caught up in which chain will win. Ultimately, apps need to win, and once they do, they will use every chain that has customers.

Crypto is the Greatest Capital Formation and Customer Bootstrapping Mechanism Ever

Digital assets are the greatest capital formation and customer bootstrapping mechanism we’ve ever seen, fully aligning all stakeholders, from customers to founders to passive token holders, and turning customers into power users and evangelists.

Customers and shareholders are often mutually exclusive in the traditional debt and equity world. For example, McDonald’s (MCD) customers are rarely MCD shareholders, and MCD shareholders are not McDonald’s target demographic. However, in the digital assets world, this gap is bridged. All customers are encouraged and incentivized to be token holders, thereby sparking motivation to help the company grow because they are being paid (via quasi-equity – the token) for their efforts. This creates full stakeholder alignment, sticky customers, and evangelists.

DoorDash, Uber and Airbnb are examples of places where this is NOT the case. DoorDash only exists because people cook, eat, and deliver food every day, but only a handful of venture capital investors share in DoorDash’s financial success. Similarly, Uber only exists because people drive cars and ride in cars, but none of these participants made money on the Uber IPO. Airbnb only exists because people own houses and like to vacation. Yet, none of the people who have made Airbnb, Uber, and DoorDash successful have any economic incentive to see these companies succeed. Had these companies been recapitalized with tokens sold or given away to early customers, their success may have been even faster and more remarkable; it certainly would have resulted in more wealth equality.

When you get past all of the misconceptions about “cryptocurrency,” “store of value,” and “internet money,” tokens really are a new form of equity transfer, where those building and growing a valuable company share in its financial success.