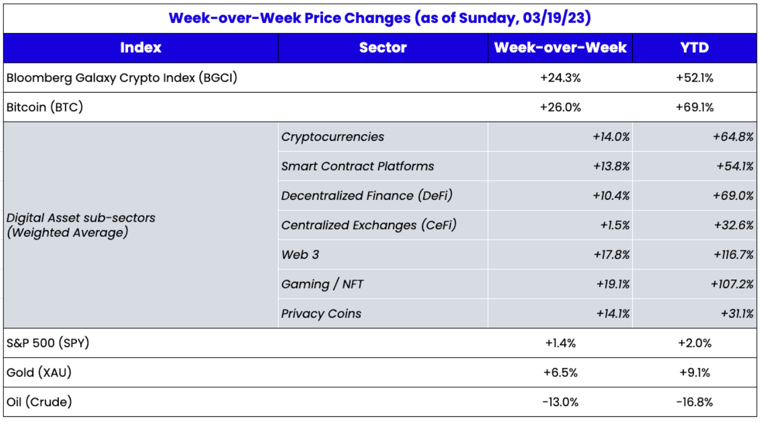

Time For More Cowbell

Source: Interest Rate Trading Desks Worldwide

Source: Interest Rate Trading Desks Worldwide

Central banks and regulators stepped in internationally to allay concerns of a burgeoning bank run this week. The moves came rapidly in response to last week’s collapse of Silicon Valley Bank, the following failure (*) of Signature Bank, and UBS’s buyout of Credit Suisse, which have shaken the nerves of investors and policymakers.

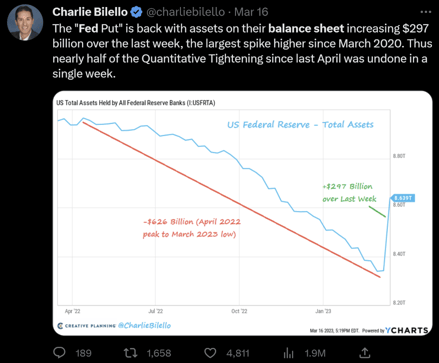

Late in the week, the Federal Reserve announced its Bank Term Funding Program (which provides undercollateralized loans to those banks able to front AAA collateral) had already seen $165B of withdrawals from the facility. While the terms of the loans were incredibly attractive, a draw from the facility was well known to come with a knock on the door from bank regulators, and withdrawals were relatively limited, given the circumstances. Still, the program helped contribute to a massive, nearly overnight, expansion of the Fed’s balance sheet, which has been in decline for almost a year with its quantitative tightening program in place.

Source: Twitter

On Sunday, UBS rescued Credit Suisse in an emergency buyout for $3.25 billion, forced through by the Swiss National Bank (SNB) without facing a shareholder vote. Concerns about the bank had escalated throughout the week, even as the SNB devoted an increasingly large proportion of its annual GDP to try to quell the fears. The takeover came only after the SNB’s offer of a $54B credit line to the troubled bank wasn’t enough to calm spooked investors and customers.

In a coordinated response effort later that day, the Federal Reserve, European Central Bank, Bank of England, Bank of Japan, and SNB introduced enhanced swap lines to ensure greater U.S. Dollar liquidity to the banking system. This tactic was also used to bolster the financial system’s resilience after the fall of Lehman Brothers in 2008 and during the early stages of the COVID-19 pandemic.

Finally, Sunday evening, the Federal Deposit Insurance Corporation (FDIC) announced that New York Community Bank would buy a large portion of the now defunct Signature Bank’s deposits for $2.7B. However, none of the deposits related to digital asset customers were part of the purchase.

After nearly two years of an uninterrupted march higher, global interest rates collapsed during the week. The MOVE index, which measures interest rate volatility, exploded to levels unseen since the Lehman Brothers fell in 2008.

Source: TradingView

Source: TradingView

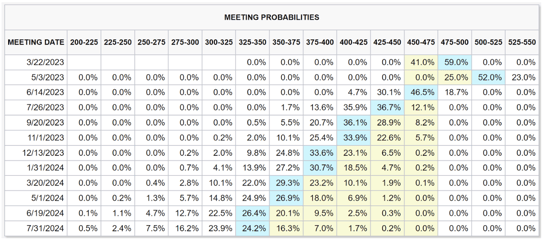

The dramatic moves on the front end of the curve resulted from traders rapidly pricing in future cuts in the Fed funds rate, with the market now pricing in a net 100bps of cuts within the year. For context, the market was priced for 50bps of hikes eight days ago. This starkly contrasts what we have recently heard from the Fed, which has vowed to hold interest rates steadily high for the foreseeable future to shake out inflation.

Source: CME FedWatch Tool

As measured by the spread between the 2-year Treasury yield (which the Fed doesn’t control) and the 3-month yield (which it basically does), at one point this week, the market was making the largest-ever call that the Fed would be unable to keep its “higher for longer” promise.

Source: TradingView

A big question for investors to keep in mind now is the Fed’s view on all this. Clearly, they have had a sense of urgency in deploying their liquidity tools over the past week. But it's still uncertain if they view these issues as overwhelming the importance of lowering inflation. The Fed has been steadfast in its desire to hold interest rates high for as long as it takes to lower inflation. If this is a true pivot, we should see some capitulation from Chair Powell at the FOMC meeting on Wednesday. But if they believe the issues have been contained and inflation remains the number one priority, we could instead see Powell sticking to his guns, which would likely put last week’s interest rate (and digital asset) moves offside instead.

Bitcoin on Display

After years of languishing without a strong narrative to propel it, Bitcoin recently caught some attention over the adoption of Ordinals, which allow things like NFTs and Layer-2 rollups to be built on Bitcoin. This news, of course, took a backseat last week.

Bitcoin was created following the fallout from the 2008 Global Financial Crisis in protest of the existing financial system and the perceived largesse of policymakers in response. Famously, Bitcoin’s Genesis Block is etched with the London Times headline “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks.” After this week, Satoshi must be feeling some serious deja vu.

With the emergency buyout of a globally systemic bank (Credit Suisse), rippling failures of regional banks, and central banks working together to establish swap lines, the parallels are striking between the periods.

Bitcoin certainly took notice.

The top cryptocurrency by market cap saw a 26.4% rise on the weekly candle—its largest move since April 2019. The rip higher comes after BTC fell below $20K just ten days ago.

You could say that Bitcoiners are feeling *ahem* bullish…

Source: Twitter

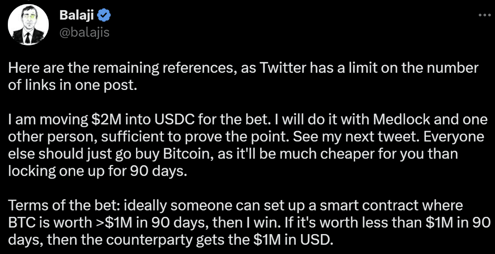

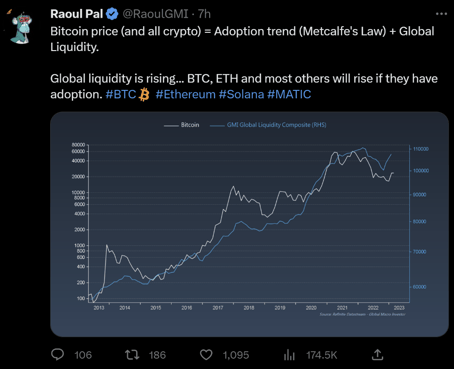

While many agree with Satoshi’s vision of Bitcoin as a hedge to systemic risk and inflation, I see Bitcoin much more as a proxy for monetary debasement and financial liquidity. Indeed, some of the strongest long-term correlations to Bitcoin’s price come from measures of monetary liquidity. After a year of tightening conditions, the trend seems to have reversed in a rather dramatic fashion. Regardless of whether banks continue to fail or the system shakes, if the Fed is giving markets more cowbell, Bitcoin will continue to work.

Source: Twitter

A Different Type of Stimulus

The second form of money from thin air came not from the government but from a crypto project, Arbitrum. Laser week, the Ethereum Layer 2 rollup announced the airdrop of its eagerly awaited token, ARB, to early users and DAOs. The airdrop of 13% of the ARB token supply will go to over 600K individual addresses beginning Thursday.

Part of the reason ARB has been so highly anticipated for nearly a year now is its likely huge size. Comparable Layer 2s like Optimism (OP) and Polygon (MATIC) are valued at over $10B. Based on Arbitrum’s relative fundamentals, we could see ARB pricing at a decent premium to its competitors, meaning that, all told, the 13% airdrop could very well exceed $1.5B of tokens.

Source: Arca Internal Research, Artemis

Source: Arca Internal Research, Artemis

Going forward, ARB holders will control a new DAO, which will decide the fate of the remaining 43% of yet unallocated tokens. If the governance decides on a similar deployment to Optimism’s, the remaining tokens may be granted to promising projects over time; the tokens can then be distributed to users. The result could be a sort of continuous airdrop, potentially worth billions of dollars over time to a community widely seen as one of the most organic in crypto.

While it's obviously an apples-to-oranges comparison, at a 10,000-foot view, it's striking to observe the week’s events together. In one world, we had a bank failure requiring emergency action from the government without shareholders’ approval. In another, a project distributed governance rights to hundreds of thousands, where all token holder decisions will immediately and automatically be executed by smart contract after a vote, and where users could gain access to the distribution for fees numbering in the cents. In one world, we watched in amazement as the central bank offered larger and larger credit lines to an ailing bank, wondering what could have created such a big hole. In the other, every single transaction that led to the governance distribution was posted to a globally accessible public ledger and able to be checked for people trying to cheat the system. The differences in transparency and fairness between these two worlds should be readily apparent.