Source: TradingView, CNBC, Bloomberg, Messari

PLEASE Stop With The “Bitcoin Isn’t A Safe Haven” Narrative

Here we go again—another geopolitical crisis and another foolish narrative that Bitcoin didn’t protect your portfolio during it.

Earlier this week, Iran launched at least 180 ballistic missiles toward Israel, marking the largest missile strike against Israel in history. As is always the case when you have any sort of war or war-like action, risk assets are immediately taken lower, and volatility spikes. Even though wars are generally good for markets in the long run due to increased government spending and stimulus, and investors have largely become numb specifically to Middle East turmoil– the algo-driven markets always respond negatively to a shock headline for a day or two before retracing.

And right on cue, here come the idiotic takes about Bitcoin.

First, yes, it’s true. Bitcoin does not protect your portfolio from geopolitical-driven macro shocks. It never has.

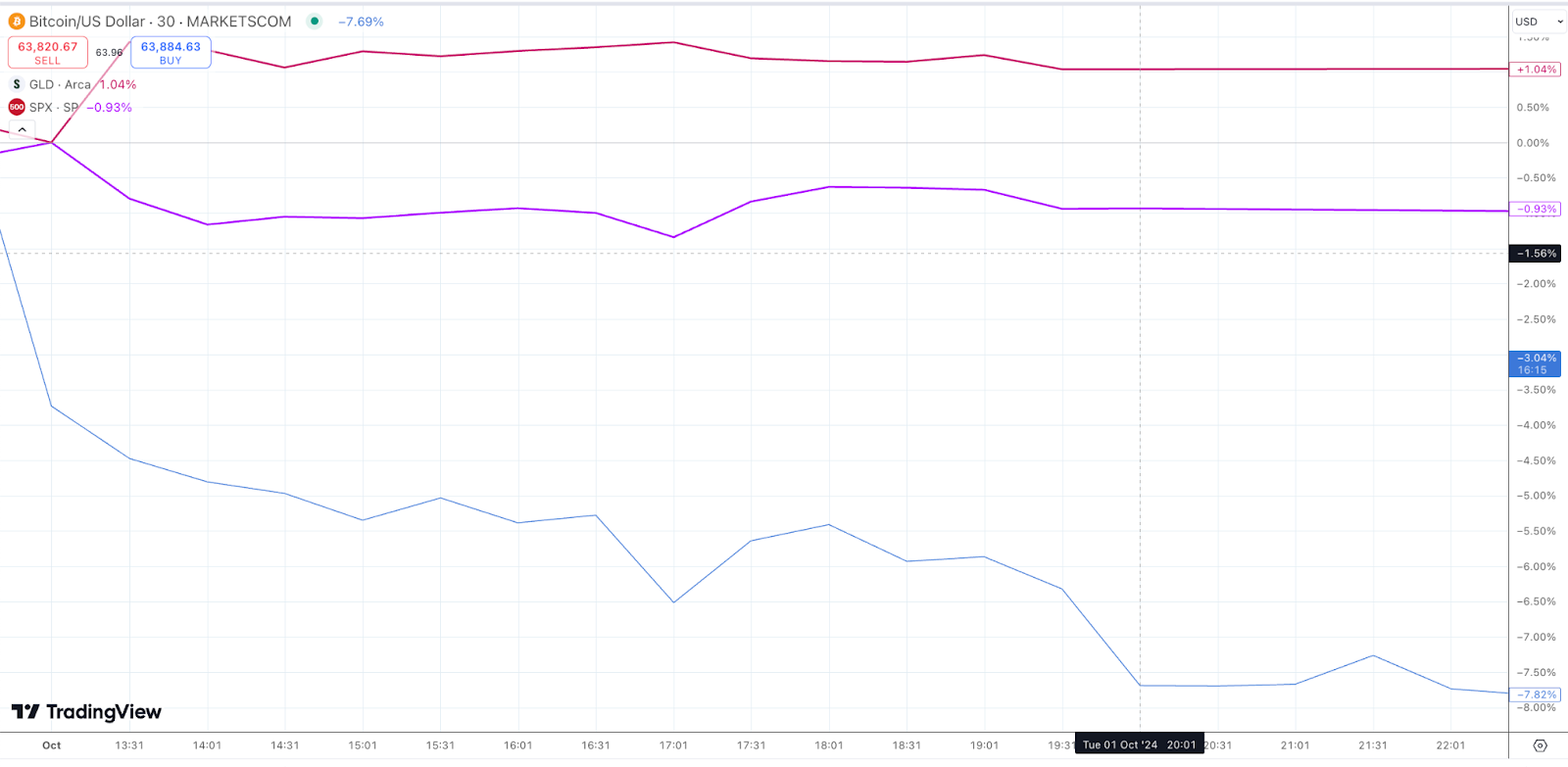

Here is a chart from October 2nd showing how gold and Bitcoin responded in opposite ways following the attack. Gold surged while Bitcoin plummeted, and stocks sold off.

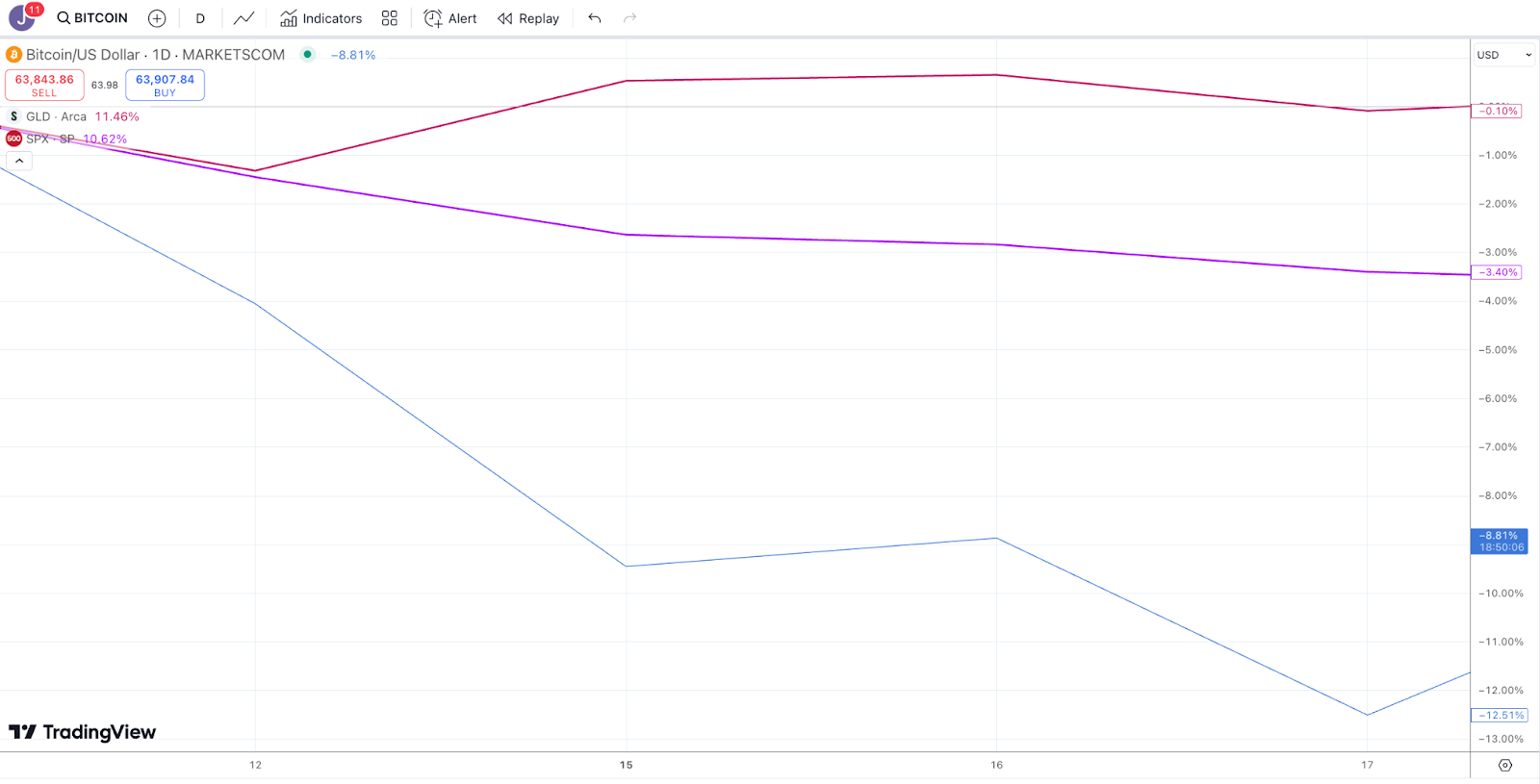

The same thing has happened throughout history. Here is a chart from mid-April 2024, when

Iran struck Israel. Stocks down, Bitcoin down, gold flat.

Source: TradingView

Source: TradingView

I know I’ve written

this same thing for five years, but I guess I must write it again. Bitcoin goes up when people lose trust in their local governments or banks, not when markets tank on other risk factors. Bitcoin rose during the March 2023 regional banking crisis, the Canadian trucking standoff, the Cypress banking crisis, the 2019 Chinese tariffs, and every time Argentina or Turkey currencies debase. There is a common theme here – Bitcoin rises like a credit default swap when the risk of governments or banks increases.

But Bitcoin never goes up when there is a market dislocation or geopolitical risk. Bitcoin will not protect your portfolio in a good old-fashioned fear trade.

And I would argue that being a hedge to local banks and governments stealing or harming your assets is a much better story than trying to pretend Bitcoin will protect your portfolio during a market crash.

Many are confused about what a “safe-haven” really is. A safe-haven investment is not an asset that never goes down; a safe-haven is an investment that is expected to retain or increase in value during times of market turbulence. More literally, “safe haven” is defined as “a place of refuge or security”. U.S. Treasuries lose substantial value when rates rise, but few argue that U.S. Treasuries aren’t a safe haven. Similarly, protecting your assets against macro factors and corrupt, overleveraged governments is a form of safe haven as well.

If you define what we're fleeing, Bitcoin is a flight to quality assets. But as a market hedge, it will not protect your portfolio from market dislocations.

Explain Bittensor (TAO) like I’m 5 years Old

Bittensor (TAO) is one of the best-performing crypto assets YTD (+128%) and has been quite the talk of the town this past week as it showed considerable strength relative to other assets.

We’ve written extensively about Bittensor over the past 18 months, showcasing its potential as early as

November 2023 and

defending criticism in April of this year. But I had no idea how polarizing this AI-themed protocol was until I

tweeted this past week that TAO is the most obvious long since Binance Coin (BNB) in 2019. There were many passionate responses, both positive and negative.

Some crypto and blockchain projects are confusing. So I always try to dumb down complex crypto topics into more digestible analogies. Here’s a simplistic way to think about the value of Bittensor:

BTC vs TAO:

BTC has one problem. Miners solve a complex math problem. It's obvious who the winner is, and the winner gets the prize (emissions). It's the most powerful supercomputer but doesn’t do anything.

Conversely, TAO does not have a single fixed problem; instead, there are lots of problems to solve. Essentially, if you can create another useful supercomputer, why not task it to do useful things? For example:

- Querying an AI model

- File storage

- Compute services

- Price predictions

Imagine the major players in Bittensor’s ecosystem similar to a science fair. Teachers (subnet owners) create the problems and try to attract the most talented students (miners) to solve and compete. Judges (validators) decide which teachers and subjects are worthwhile. They reward the teachers (subnet owners) and the students (miners) if they agree.

A popular criticism is that this dynamic is arbitrary since the validators (judges) may not be the most knowledgeable or appropriate judges. Soon to be implemented,

Dynamic TAO solves this by introducing a token for each subnet, and the market price of each subnet token will determine how much reward you get. You must buy TAO and stake it to get subnet tokens.

The best subnets will ultimately create resources that other apps can be built upon (these apps can be profitable). Said another way, the subnets themselves are not valuable but can lead to valuable products. For example, wheat and oil (mined on a subnet) aren’t useful on their own, but people (validators) can refine them to make them useful (Make flour out of wheat, make bread out of flour). Looking at some of the

most popular subnets to date gives you an idea of what resources are available for others to profit from.

Value of TAO:

To be a validator and use these resources, you must own TAO. Thus, the demand function for TAO is real. For example, if miners produce trade recommendations based on price predictions from a subnet, then validators can build an app to sell these trade recommendations. Essentially, the validators are the business development team. The number of apps you can build is seemingly endless – you can sell a language translator app, or video rendering services, etc.

As long as the value you receive from the outputs of these subnets (profitable apps) is (or will be) greater than the cost of TAO, then TAO will be bought. We currently think these resources are collectively worth hundreds of billions of dollars to current and future companies.

As a result, TAO hits all three value drivers:

- Financial value - future revenue from selling apps/services

- Utility value - must own / stake TAO to do this

- Social value - AI Theme

And that is why TAO is outperforming.