Source: TradingView, CNBC, Bloomberg, Messari

Bitcoin pauses while other digital assets play catchup

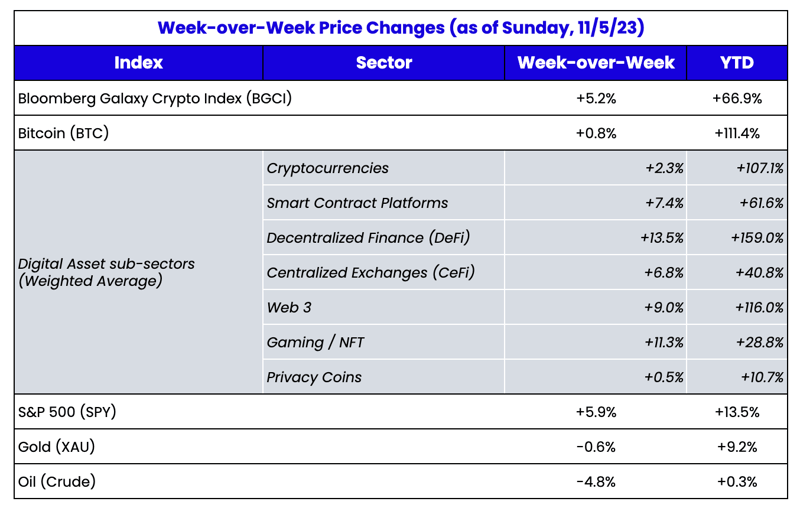

It was only a week ago when we highlighted the massive outperformance of digital assets compared to equities and fixed income:

“It’s not how much digital assets are up, but rather, how this is happening when the rest of global markets seem to be in doom mode. The relative outperformance is raising eyebrows, TradFi is noticing, and phones are ringing again.”

Immediately thereafter, the S&P 500 rallied +5.9% over the next five days, and 10-year U.S, Treasury yields fell 40 basis points. All it took was an

FOMC meeting, where the Fed essentially said it was done raising rates, followed by a somewhat weaker jobs report for all of the doom and gloom in TradFi markets was erased. Hedge funds

extended a record number of short positions on U.S. Treasuries at the worst moment last week — just before the rally. One might think that digital assets would sell off now that debt and equity markets have regained their footing, reversing some of the recent negative correlations, but instead, the crypto markets continued their ascent. But for the first time since January, Bitcoin had nothing to do with the rally, finishing the week basically unchanged. This makes sense, as BTC seems to do the best when regional banks (KRE) and U.S. government debt falter, and last week both bank stocks and government bonds showed strength. What was surprising was how fast tokens in other crypto sectors took off at the first sign of BTC stalling. As you can see in the table at the top, most digital asset sectors meaningfully outperformed Bitcoin and other cryptocurrencies. We saw particular strength in gaming (e.g. ILV and IMX both +29%), decentralized exchanges (e.g. CAKE +83%, SUSHI +53%), and even some Layer-1 protocols that had conferences and events (NEAR +20%, SOL +14%).

In past cycles, this behavior has been typical – Bitcoin rallies first, then a few select large caps, and then small caps. But that rotation typically happens slowly. The speed with which this is occurring indicates that investors are prepared for this behavior to repeat, and are therefore front-running it. Or perhaps some of the new money pouring into Bitcoin from traditional brokerage accounts in recent weeks has been met with crypto native investors selling BTC and using proceeds to roll further down the risk spectrum.

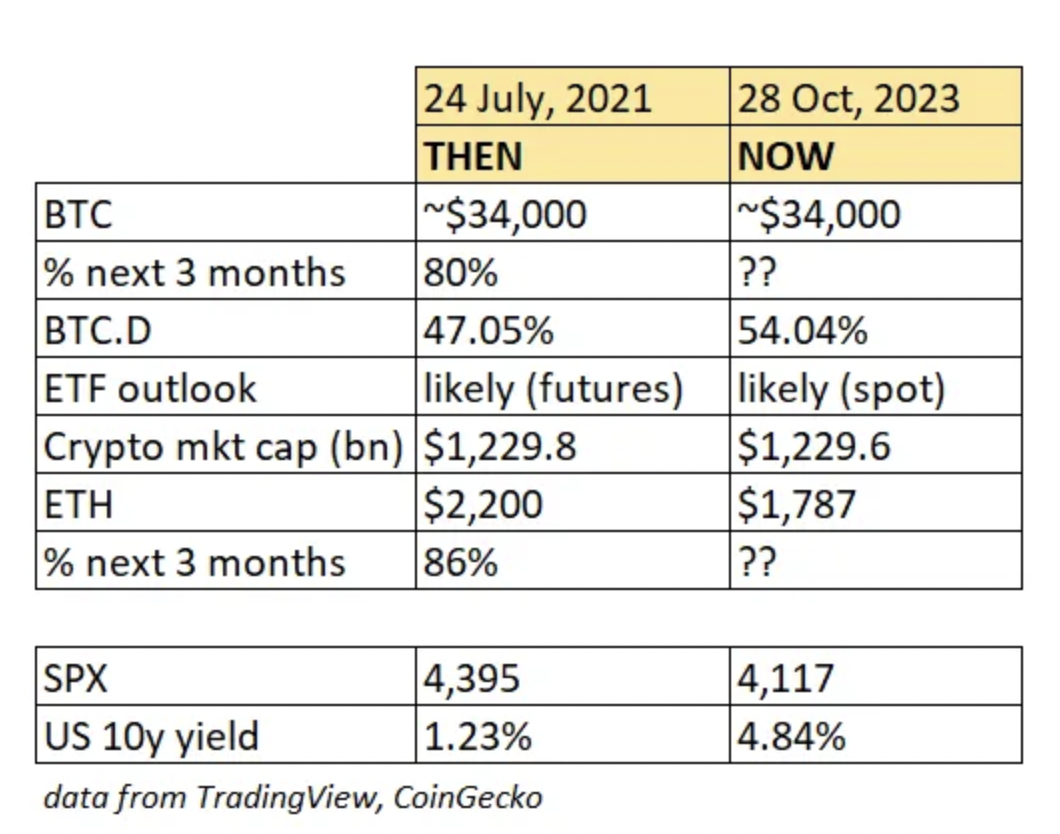

Crypto market research analyst, Noelle Acheson, made a wise observation last week. With BTC stalling between $34,000 and $35,000, it’s useful to look back a few years to the last time BTC traded around these levels. There are a lot of similarities to July 2021, as BTC, the S&P 500, and the total crypto market cap are basically unchanged over 2.25 years (her table is a week old, but the S&P has since rallied to 4,358 and ETH has rallied to $1,900). ETH has noticeably lagged over this time period, and interest rates are now over 300 basis points higher. As Acheson points out, it’s far more likely that rates go lower than higher from current levels, which in theory is much more accommodative for BTC. Back in mid-2021, BTC ultimately nearly doubled to a high of $69,000 over the next few months, and that was in the face of an eventual rate hiking cycle. If we do see another BTC breakout, will other areas of the crypto ecosystem lag or keep pace?

Taxonomies

I danced around the topic above, highlighting specific areas of the digital assets market that outperformed Bitcoin last week. Others will likely just call this an “altcoin rally” given the price gains excluding Bitcoin. Frequent readers know that I hate the term “altcoin”, as it suggests that there are two distinct areas of blockchain – Bitcoin and “other”. This is obviously not accurate, as many sectors have shown staying power (DeFi, Stablecoins, NFTs) while others are growing fast (AI, RWAs, Gaming, Social, etc). Altcoins is an outdated term that needs to be eradicated immediately.

Fortunately, we’re not the only ones trying to educate the masses on the different types of digital assets, and the different sectors. Grayscale, the asset management subsidiary of Digital Currency Group (DGC) recently

published a new Taxonomy for digital assets. I really liked how they laid this out.

The Grayscale Crypto Sectors can be categorized based on function, technical features, and investable exposure.

- Currencies: A medium of exchange and store of value

- Smart Contract Platforms: Infrastructure that enables autonomy and accessibility for developers to build applications

- Financial: Financial applications to lend, borrow, and trade assets directly with one another

- Consumer and Culture: Gaming, art, music, and media applications

- Utilities and Services: Tooling that augments the functionality of existing smart contract applications.

Recall, Arca was one of the first firms to

publish a taxonomy back in 2021. Grayscale’s taxonomy varies a bit from ours, as it focuses more on sectors whereas ours focuses more on token structures, but it’s a further step in the right direction. Despite many

legal and ethical problems currently swirling around Grayscale, Genesis, and their parent company, DCG, Grayscale is still the largest asset manager in the industry, and it’s good to finally see some educational materials published for their clients. For those who want a more independent segregation of digital assets, research firm Messari has been doing this for years with their

categories and tags.

This has been an encouraging rally for digital assets off of last year’s lows. It has now been exactly one year since FTX imploded and filed for bankruptcy. Over this time period, there has been great dispersion. Some tokens are now comfortably higher than pre-FTX default levels, including Bitcoin, Ethereum, and even Solana, which had cratered the most immediately following the FTX bankruptcy. The majority of other tokens remain significantly lower. In our coverage universe, roughly ⅓ of tokens are now flat to above their November 1, 2022 prices, while ⅔ are still below, the majority of which are down 30% or more. The past 12 months have truly been a “token pickers market”.

In order to pick tokens, you need a deeper understanding of what types of tokens exist, and what sectors they fall into, so we encourage everyone to explore these taxonomies.