Source: TradingView, CNBC, Bloomberg, Messari

The Thesis is the Easy Part – How You Express the Thesis is the Hardest Part

A select few are great traders. The rest of us have to stay long- biased in an industry or an asset class with asymmetric upside. Missing violent rallies by trying to time entry points is hard to recover from.

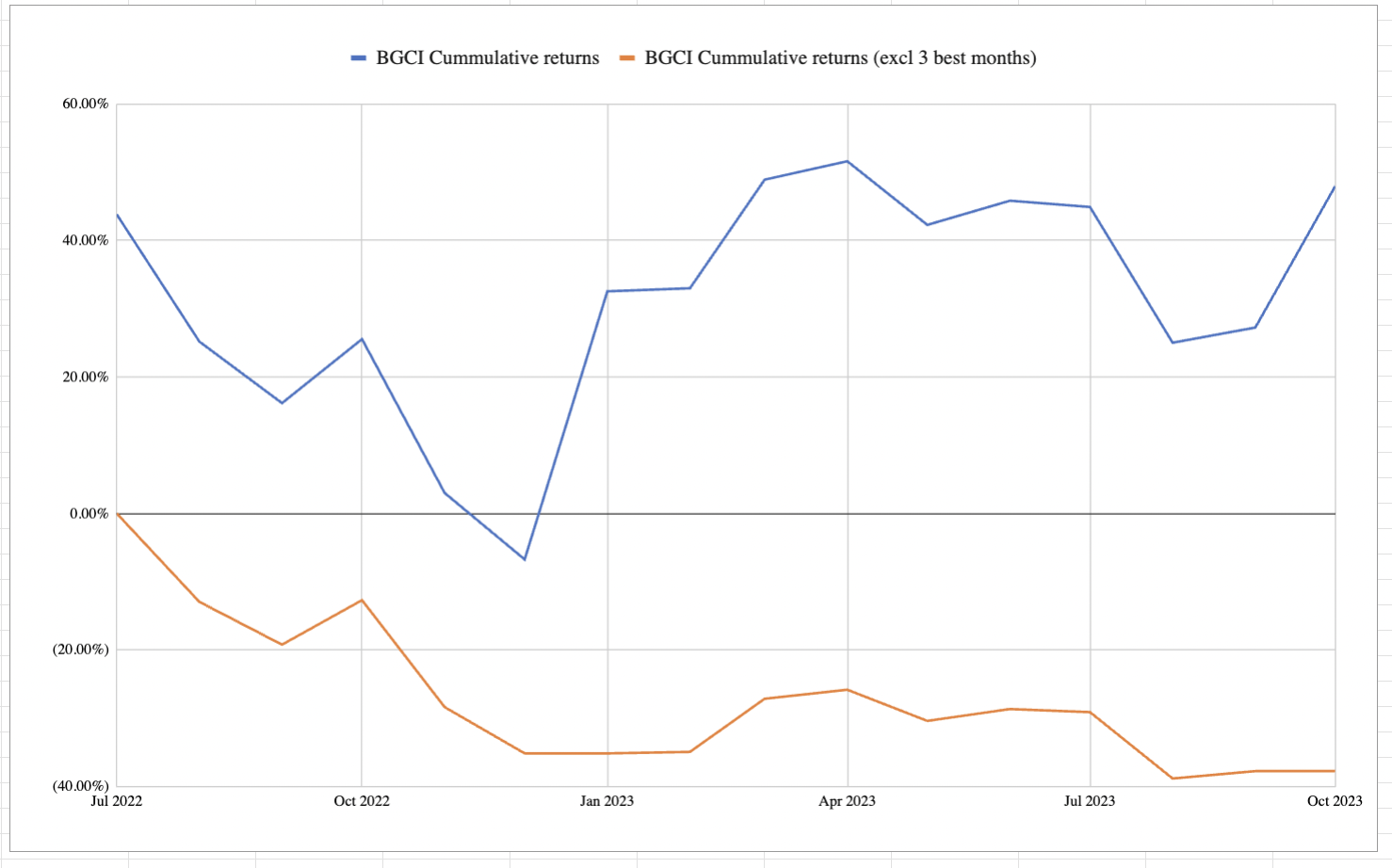

Case in point. It has felt pretty dismal in the digital assets investment arena since the 2nd quarter of 2022, when a cascade of liquidations and bankruptcies began. Over the past 5 quarters (plus October), there have been more down weeks and down months than there have been gains. It is understandable that many investors remain on the sidelines while others are trying to squeeze a few more drops from the lemon via shorting. Yet, amidst several long periods of accumulated losses, we have now seen three fast, sharp upticks (July 2022, January 2023, and now October 2023) that have erased all of the losses in a heartbeat. Using the Galaxy Bloomberg Crypto Index (BGCI) as an example, you can see how being long the market during these three months has been essential to offsetting an otherwise brutal investment period.

From July 1, 2022 through October 29, 2023, the cumulative gain for the BGCI is +47.95%. However, if you exclude these three months, the BGCI has registered a cumulative loss of -37.75%.

Source: Bloomberg / Arca estimates

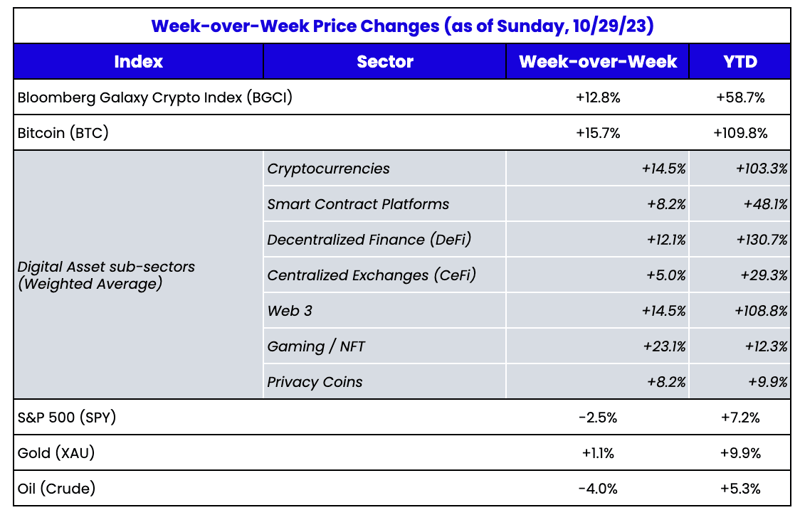

Most of these gains have gone unnoticed. In fact, the majority of non-crypto natives still think digital assets have been going lower despite Bitcoin being one of the best-performing assets year-to-date (+110% YTD) and digital assets collectively being the best-performing asset class. But anecdotally, over the past few weeks, this sentiment seems to have shifted. Not only are digital assets up double-digits for the second week in a row, but they are up dramatically when compared to declining commodities, equity and fixed-income markets.

It’s not how much digital assets are up, but rather, how this is happening when the rest of global markets seem to be in doom mode. The relative outperformance is raising eyebrows, TradFi is noticing, and phones are ringing again. Those who started investing in digital assets in mid-2021 may find it hard to comprehend that digital assets move differently than other risk assets. However those who were investing from 2016-2021 know that uncorrelated is actually the norm, and 2022's high correlation between digital assets and other asset classes was actually the anomaly.

And in some cases, it’s not just uncorrelated, but rather negatively correlated. We’ve been talking about

Bitcoin versus KRE (Regional banking ETF) since March 2023. The inverse correlation is back again this month. It’s not a coincidence that Bitcoin shows strength during perids of time when investors lose confidence in banks and local governments. As

Arthur Hayes points out, in times of strife, Bitcoin often wins.

- Since Russia / Ukraine war: TLT (US Treasury ETF) -16% versus BTC +50%

- Since Hamas / Israel war: TLT -3% vs. BTC +24%

Source: TradingView

Similarly, Ethereum (ETH) and Coinbase (COIN) may be the two most plain vanilla ways to express a “long blockchain” thesis. Coinbase derives revenues from trading, staking, stablecoins (USDC), and the growth of Layer-2 blockchains (via Base). Ethereum is the #1 smart contract protocol for DeFi, stablecoins and NFT activity, and you can even find almost $6 billion of “wrapped BTC” on Ethereum. Both ETH and COIN give you exposure to the broader growth and adoption of digital assets.

But all of the correlations in the world don't change the fact that COIN is a stock, while ETH is a token, and right now these investor bases are acting differently. These two assets have different investors, different indices, different asset class weightings, and different brokerages/exchanges where investors can access these different instruments. Stocks are getting pummeled and have fallen out of favor, while digital assets have caught a bid. As a result, if you tried to gain exposure to this month’s crypto rally via long COIN stock, you’d be severely disappointed, especially this past week.

Source: TradingView

The relative strength is being noticed. Bitcoin Open Interest on the CME hit all-time highs last week with

open interest of 100,000 BTC (~$3.4B USD). This trend may reflect growing interest in Bitcoin from institutional investors as the conversation around a coming spot bitcoin ETF continues to heat up. And Bitcoin’s strength has not been isolated this time- rest of the digital asset market is beginning to show life as well.

Views Around The Market

Strength in Bitcoin around increasing ETF expectations pulled up the whole market, with application platforms rising the most on the week. Solana (SOL) gained +19% and has become a market darling ahead of this week's Breakpoint conference while Aptos (APT) rose +28%. Binance Coin (BNB) and Cosmos (ATOM) lagged (up +5% and +10% respectively) as both continue to suffer from low sentiment, with Binance targeted this week by U.S. lawmakers who asked the DOJ to further investigate the exchange.

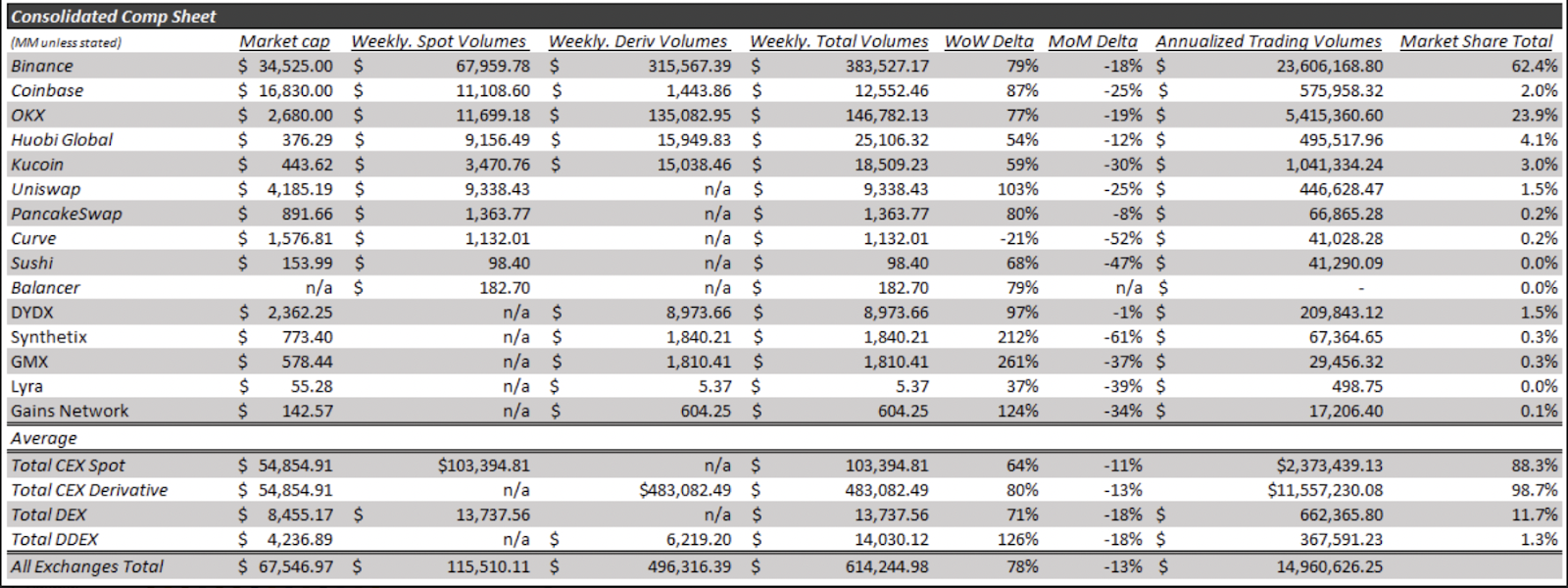

Because of increased volatility and outsized movements in BTC, exchange volumes across the board saw significant growth. Total volumes increased by 78% week-over-week to reach $614 billion. Derivatives volumes played a leading role in this surge, with CEX derivatives up by 80%, and DDEX derivatives volumes rising by 126% week-over-week.

Source: Token terminal and Arca Internal Calculations

With the market starting to slowly thaw, some projects and companies are beginning to take advantage of the improved sentiment by making much-needed updates and announcements, especially around tokenomics (a topic that we discussed

earlier this month). DYDX shipped

updated tokenomics last week as it migrated to its own chain on Cosmos, leading to a new +19% rally week-over-week. We’ve also seen tokenomics upgrades (or announcements) from OSMO, MATIC, IMX, AKT, BONE, and RLB in recent weeks.

It’s too early to tell if this shift is permanent, or just another strong month amidst a long drought. Our friends at Cumberland probably said it best in a weekly note to clients:

“With BTC up 30% in the past two weeks, it’s pretty fair to say that the market dynamic has changed significantly, so we wanted to take a big step back. “The Turn” is a term often thrown around on trading desks, signifying the moment when the dynamic fully flips. Unfortunately, it’s usually a term used in hindsight (and even more unfortunately, it’s usually a trader explaining to their boss that they missed the turn…); it’s difficult to tell if the market is turning in the moment, or if it’s just a headfake. It’s hard to tell if the move of the past two weeks is false optimism, or the beginning of a rally that will last the next eighteen months. However, it’s been a significant enough change that it merits stepping back and investigating priors. The story of 2022 was a crash driven by irresponsible optimism and unsavory practices in 2021. The story in the first ten months of 2023 was a slow recovery that nonetheless still felt like a bear market. No matter what happens next, that chapter seems to be closing now. One thing has definitely changed: for the past two years, the path of least resistance has been lower, but the path of least resistance seems to now be higher.”