Please note, "The Four Buckets of the Digital Assets Market" will be the last "That's Our Two Satoshis" published in 2019. The next edition will be published January 6, 2019.

What happened this week in the Crypto markets?

The digital assets market broadly fell 3-6% last week, with only a few out-performers (largely related to the staking theme we pointed out last week). As we near the end of the month/year/decade, crypto markets are noticeably slowing down. Price action in digital assets has oscillated with less amplitude, volumes are stagnating, and news cycles are slowing. This feels similar to December 2018, where nothing of significance happened until March 2019. Notably, during that next 3-month stretch in early 2019, a few select non-Bitcoin digital assets broke out with large gains, setting the stage for a broad-based market rally over the next 6 months.

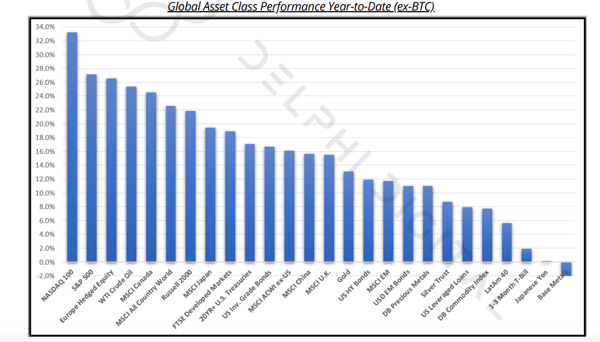

Crypto Returns Have Been Mixed in 2019

Unless you are long volatility, it has been pretty difficult to lose money in 2019.

As regular readers know, there is a lot more to the digital assets space than just Bitcoin, and the crypto returns have been very mixed depending on where you focus. There are clear themes within digital assets that are emerging, and investors in this space need to differentiate between the “Haves” and “Have Nots” -- sometimes these “Haves” are specific to individual investable assets, but more often they are tied to themes and categories.

We believe the digital assets space can now be split into 4 buckets. It’s worth looking back at the return spectrums from 2019 in each bucket as a guide to what will likely work in 2020 and beyond.

- Money

- Protocols/platforms/decentralized projects

- Real cash-flow producing companies that utilize tokens

- Existing asset classes that can be digitized

1) Money

Bitcoin is the only proven winner thus far, and it is outperforming the field by a wide margin, though the majority are still positive YTD.

2) Decentralized Protocols/Platforms

Decentralized Protocols and Platforms are the backbone of the “Decentralized Web 3.0” narrative. But these tokens are really more suitable for venture capital portfolios, as they are 5-10 years away from creating any real economic value, and most will fail while only a few will be home runs. They are often half-built, largely untested, and have a lot of slack between usage and token value. As such, the majority of these tokens are down YTD as the market has adopted a "prove it" mentality. Even Ethereum, the undisputed leader in terms of usage and activity, has yet to prove any economic value, but it is a live working product and thus has outperformed handsomely.

3) Real Cash Flow Producing Companies

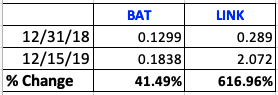

With regard to real cash flow producing companies, this is where it gets more interesting. There are many real companies that have found product-market fit and have figured out a real use case for tokens. The gaming industry is a good example, with HXRO being one of the best games and best token use cases we’ve come across (gamification of trading). There has also been progress from middleware companies (like Chainlink - LINK) and internet companies (like Brave Browser - BAT). In addition to crypto-native companies like the ones mentioned above, there are many existing companies that have nothing to do with crypto or decentralization that could very easily introduce a token into their cap structure -- companies that come to mind are Twitter, Wikipedia and Starbucks, all of whom could issue a token that has immediate utility for its customers.

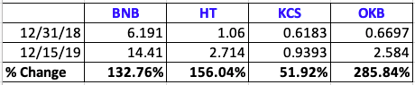

But the problem with real cash flow producing companies is there is often a disconnect between their customers and their knowledge of digital assets. That's why the tokens of Binance and other Centralized Exchanges have been so successful -- there is 100% overlap between Exchange customers AND their knowledge of tokens. Even with lower volumes, centralized exchanges generate strong revenues, have a real use case for their tokens (reduced trading fees and access to special offers) and quasi-equity like features (distributions to token holders via token burns from revenue/profit). As a result, they have outperformed the market YTD. As expected though, success has brought competition -- and this sub-sector of real cash-flow producing companies is fairly saturated now with the addition of several new tokens.

4) Existing Asset Classes That Can Be Digitized

This doesn’t really exist yet, but it’s coming. Soon. Tokens backed by hard assets, or by the equity and debt of real companies, will be immediately investable by traditional investors as well as crypto investors. We’d expect these tokens to trade similarly to traditional asset classes, but will likely come at significant discounts in the early days as the market develops.

A Note on Repo, Risk & Moral Hazard

While every asset class has produced outsized returns in 2019, it’s worth pausing from the euphoria to look at the risks that are brewing. You can’t focus on digital assets without paying attention to stresses in traditional markets, as digital assets wouldn’t even exist if it wasn’t for the issues that were surfaced from 2008-2012, which was the impetus for Satoshi releasing the Bitcoin whitepaper.

While central banks have papered over the problems for years, unfortunately, the issues are back. And this time, digital assets won’t be an unknown solution born from the ashes, it may be the saving grace.

The repo markets are currently sending a giant red flag. And most people are completely ignoring it. For a primer, start here. Why is this being ignored? Two reasons:

- People generally IGNORE what they don't understand. It's far easier to assume a problem will go away than to ask the right questions and learn.

- There is very little INCENTIVE to take the other side.

Ignorance

Take a conversation I had with 2 friends of mine -- one works on the repo desk at a very large broker/dealer, the other works at a very large commercial/investment bank that is at the heart of the repo issues (but he himself does not work in that area of the firm).

The person who understands repo and lives it every day said this: "It's a mess. If you can picture the money markets on drugs, then that's my take. It's a big debacle that gets swept under the rug. Nobody pays attention to the MM space until they have to. A decade ago, nobody understood that the issues stemmed from the Commercial Paper market. Same thing today. But I find it hard to believe it has taken this long to figure out what happened 3 months ago. I don't have a lot of faith in our financial system right now."

Contrast that to my incredibly smart friend who works within the large bank and has made 5x return on his company stock the last 10 years, who said this: “08 repo issues were about lack of confidence / c'party risk. That’s not happening now. It's just a mismatch in supply / demand."

He may be completely right, but he's also incentivized to not care that much and to turn a blind eye. He can't do anything about it anyway. When Bear Stearns and Lehman employees tried to sell their stock, they were berated and shamed and often were convinced not to sell.

Incentives

When I was a trader at Merrill Lynch in 2007, I was very short the credit markets. An older, very smart trader told me "Don't bother - if you're wrong, you won't get a good bonus. If you're right, Merrill will be out of business and you won't get paid."

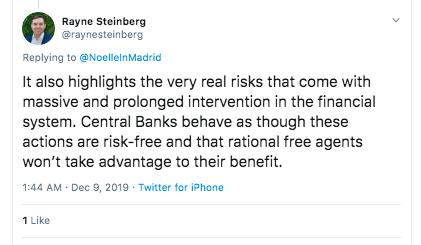

This is the entire market right now. There is no incentive to do anything other than just stay long. If you're long and wrong, so is everyone else. If you're short/cautious and are too early, you will get slammed (see Ray Dalio). As Arca CEO, Rayne Steinberg, pointed out, not only does this create moral hazard, but it creates excessive risk taking.

What does this have to do with digital assets? Potentially nothing. Bitcoin is unlikely to trade up in a real financial crisis similar to 2008. However, the reason Bitcoin and decentralized finance exists today is to eventually eliminate future episodes of what is about to come. So while it may not preserve wealth during the next crisis, it will likely prevent wealth destruction for future generations. More importantly, the repo markets should make everyone curious enough to challenge the status quo. With today’s information ubiquity, it is time to challenge and ask questions, and ultimately learn. We wrote about this in August before the repo mess even started. It still applies.

Notable Movers and Shakers

With the decade drawing to a close, Bitcoin has chosen to go quietly into the night (thus far!). Muted price action and volumes give way to a bored market as many are spending time with family and friends, and paying less attention to our favorite 24/7 asset class. Nonetheless, the beat goes on, with a few projects moving and shaking:

- VeChain (VET) was the unfortunate recipient of a hack on Friday, as 1% (1.1B VET, $6.52M) of the outstanding supply was taken out of the Foundation’s wallet. The VeChain Foundation has attributed this loss to “human error within the foundation”, which was “most likely due to misconduct of one of the team members within our finance team”. The market didn’t respond well to the news, losing 21% by week end.

- Matic Network (MATIC) inexplicably fell like a stone last week, losing 65% (with a 60% loss in a 2 hour span). The Binance and Matic Network team both released statements attributing this drop to a “coordinated attack”, without specifying the details of said attack. Another likely scenario is that MATIC was propped up for weeks by a combination of one-sided margin trading and the FLINT airdrop, which had their snapshot at the exact same time as the token’s sharp price decline. These sharp moves are seen as black swan events in any other market - in this market, however, they are a painful reminder of the lack of real liquidity (see CLAMS, ZCL).

What We’re Reading this Week

Last week, Twitter CEO Jack Dorsey, made waves announcing a new team within Twitter that would actively work to decentralize the social media platform. The team, bluesky, will be tasked with creating an open-source protocol, similar to internet protocols that run internet applications (such as HTTP for webpages or SMTP for email). Dorsey explained in his Tweet Thread how a decentralized version of Twitter made far more sense, especially as the platform seeks further expansion. This latest move by Twitter may be the catalyst to move digital assets and tokenization to the mainstream.

Grayscale released a study last week that inspected female investors and their attitudes towards digital assets as investments, in particular Bitcoin. The study found that women are interested in Bitcoin as an investment and appreciate its features such as the ability to buy fractional amounts (63% female versus 56% male) and trade it easily (60% female versus 56% male). What is most surprising is that the education opportunities for women is massive: 93% of women indicated they’d be more open to investing in digital assets if they had more education on the subject.

According to reports, JPMorgan is eyeing a January launch for Interbank Information Network (IIN), its blockchain payments network. The system allows banks that join the ability to verify payment information with each other instantly. Japan has been under pressure recently to increase its AML procedures and therefore 80 Japanese banks have expressed interested in joining IIN. Aside from speeding up the settlement of payments, IIN also offers the ability for banks to collaborate with law enforcement on potential money laundering activity.

Last week Nike received a patent to create Ethereum-based tokens that represent a pair of their sneakers. Specifically, Nike plans to generate a unique ID and a ERC-721 (one of the Ethereum token standards) token. The token will link ownership for sneakers and also give the owner control over their shoes and shoe design. The move is not surprising given the increased interest in trading and reselling collectible shoes.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)