What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 10/25/20)

|

|

WoW

|

YTD

|

|

Bitcoin

|

+13.0%

|

+79.7%

|

|

Bloomberg Galaxy Crypto Index

|

+9.7%

|

+98.9%

|

|

S&P 500

|

-0.5%

|

+7.3%

|

|

Gold (XAU)

|

+1.2%

|

+26.7%

|

|

Oil (Brent)

|

-3.4%

|

-35.0%

|

Source: TradingView, CNBC, Bloomberg

Bitcoin Sucked the Life Out of the Digital Assets Market

Frequent readers of That’s Our Two Satoshis know that we love Bitcoin, but we also think Bitcoin is in a completely different category (cryptocurrency) than the majority of other digital assets (platforms, asset-backed tokens, and pass-thru tokens). There is of course a structural commonality between all blockchain-based digital assets, which is what makes this an asset class, but in every other way each asset is vastly different. Bitcoin is decentralized, has no leader, and competes as money on a global scale, while most other digital assets are closer to growth assets belonging to closed ecosystems of centralized companies or projects. As such, in a perfectly rational world, Bitcoin’s strong price action might not matter much to the rest of the digital assets ecosystem, as it is on an island unto itself. But there exists a rotation of capital in digital assets that is more powerful than anything seen in other asset classes.

In the traditional investing world, rotation of capital exists too, but it is quite different. If market conditions change in ways that make equities more attractive, you might see a natural rotation of capital out of fixed income and into equities, and you might also see cash being put to work, indicating new buying power. At the sector and individual asset level, you might also see rotations from growth stocks into value stocks, or from cyclicals into non-cyclicals. But it is rare that these moves suck the life out of other areas of the market.

The rotation of capital into Bitcoin these past weeks absolutely sucked the life out of the rest of the market.

To start with, there is a very odd and out-dated term in digital assets called “Bitcoin Dominance”, which measures the percentage of Bitcoin’s market cap relative to the overall size of publicly traded digital assets. This term perhaps made sense in the early days, when there were only a handful of digital assets, most of which were knockoff forms of money, but of course makes less and less sense as this asset class matures and evolves. It would be akin to measuring “Government Bond Dominance” as a way to indicate overall movements in the fixed income market, despite certain types of fixed income securities like converts and bank loans having nothing to do with govies.

There have been plenty of instances where Bitcoin has outperformed other digital assets. But as our friends at Cumberland pointed out, typically this happens when everything is rising and Bitcoin just rises more, or more often, when the entire market is falling and Bitcoin falls less as a flight to safety.

“This week, we’re seeing a much-discussed but seldom seen event in digital assets: a “BTC-up, everything else down” move. BTC dominance has rallied from 60% to open the week to about 61.7% right now. A move of that size is not unheard-of -- in fact, we see one that size every month or so. What is rare is that BTC is up while other digital assets are down. Normally a BTC.D move happens when there are large delta moves and one asset outpaces others. The move lower in BTC.D through this summer was largely a function of ETH and ERC20 tokens rallying, with BTC just rallying more slowly. The move higher in BTC.D last spring was while everything collapsed, as non-BTC tokens traded with much higher betas. We’d be counting on eagle-eyed readers to remind me of the last time we’ve seen BTC deltas separate from the pack in exactly this way.”

Bitcoin is seeing a lot of new inflows. From corporate Treasury departments, to family offices, to macro investors, this new influx of capital is, for the most part, only flowing into Bitcoin. And this makes sense given that Bitcoin is in a totally separate class of its own that attracts a wide array of different investor types. However, the decline in other digital assets suggests that native digital assets investors are also selling anything and everything they own for the opportunity to own more Bitcoin. Again using the Government bond example, this would make more sense if this was a flight to quality rally, but that would most likely occur during periods of market weakness, not periods of euphoria.

It’s highly unlikely that this dynamic will hold for longer periods of time. As institutional investors continue to invest in venture capital funds and fundamentally based research-driven hedge funds, the need to benchmark versus Bitcoin will subside, as will the ability for funds to sell everything into Bitcoin. Until then, retail and trade-oriented investors may continue to chase Bitcoin at the expense of other tokens.

How is Bitcoin Affecting Traditional Finance?

Away from digital assets, Bitcoin is affecting the rest of the financial world as well. To start with, there are a number of publicly traded companies that have, intentionally or unintentionally, marketed themselves as “Bitcoin companies”. Who needs a Bitcoin ETF when these existing stocks basically track the price of Bitcoin already? From Bitcoin mining companies like Hut 8 (HUT), to crypto merchant banks like Galaxy Digital (GLXY) and traditional banks like Silvergate (SI), to the recent corporate actions by Microstrategy (MSTR), most of these stocks have basically become BTC tracking stocks, whether that is their core business or not. As Square (SQ) and Paypal (PYPL) enter the market, it will be interesting to see if Bitcoin’s price action begins to dominate these companies’ narratives as well. Further, the upcoming Coinbase IPO should be interesting, as Coinbase has a very diversified business line, but the market may completely ignore that in favor of simply watching Bitcoin’s price.

Stocks of companies with exposure to Bitcoin have become Bitcoin tracking stocks

Source: Bloomberg, TradingView

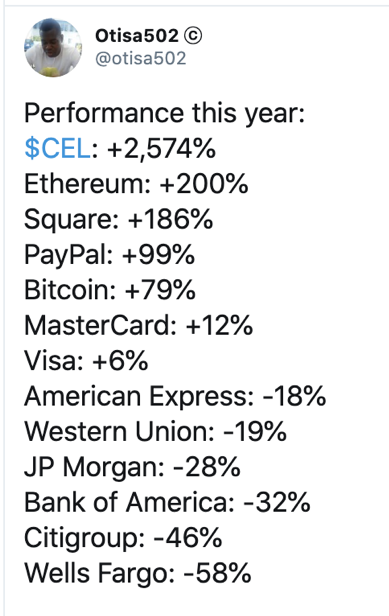

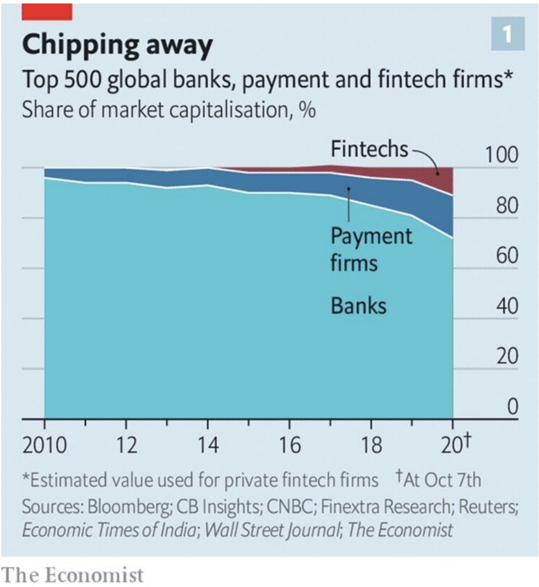

While it remains to be seen whether or not it is a good thing for companies to be associated with Bitcoin, we know definitively that traditional finance companies that have not evolved are being punished. Perhaps we need a “Traditional Bank Dominance Index” to help visualize the massive decline of traditional banks at the expense of FinTech and digital assets.

Source: Twitter / @otisa502 and The Economist

Will Bitcoin’s rise and the subsequent growth of FinTech companies like Square and PayPal be enough to move digital assets into the mainstream? We’ve long argued that investment bankers are missing one of the biggest opportunities in history by not introducing digital assets to their clients. While investment banks can’t profit on Bitcoin itself since they lack the infrastructure to trade it, they do care about missing out on lost fees. When direct listings threatened their IPO businesses, they responded by starting consulting arms to help companies with direct listing processes. Similarly, these new corporate treasury Bitcoin purchases will threaten their stock buyback fees and their M&A fees (as cash is being used to buy Bitcoin instead of making acquisitions). When companies like Square ($80 bn market cap) and PayPal ($230 bn market cap) become unbankable, it’s inevitable that investment banks will find a way to insert themselves into this growing revenue stream.

What’s Driving Token Prices?

Off the heels of the PayPal announcement and overall continued strength of Bitcoin, Bitcoin Dominance rose 3% (the largest such increase since the last week of April 2020). While the rest of the Digital Assets market suffered as a result of this capital rotation, there were two notable standouts this week:

- Reserve Rights (RSR) was the beneficiary of seemingly unrelated news when PayPal announced their new service for digital assets, as their investor list contains three associates of Paypal: Peter Thiel (co-founder), Jack Selby (founding member), and Eric Jackson (former VP of marketing). To add to the speculative whirlwind, Coinbase Ventures is also on the investor list, and in their blog post two weeks ago RSR was on the list of potential candidates for Coinbase Custody. Rumors spread fast in this space, and the token benefitted: RSR finished the week up 40%.

- Filecoin (FIL) experienced a hiccup shortly after having their main net go live as Filecoin miners went on strike due to their disapproval with the economic model’s impact on their operations. Filecoin requires miners to stake a significant amount of FIL to ramp up capacity and utilize mining equipment, which led to many large miners keeping a significant portion of their machinery offline. The Filecoin team quickly met the demands of the disgruntled miners, announcing that they have revised the model to release 25% of the token rewards in advance as soon as a machine comes online to help bootstrap operations as they ramp up to full capacity. The market reacted favorably to this revision, as the token finished the week up 19%.

What We’re Reading this Week

PayPal to open up network to cryptocurrenciesChina digital currency: Shenzhen consumers spend 8.8 million yuan in largest trial of digital yuan

The First Nationwide Central Bank Digital Currency In The World Has Been Launched By The Bahamas

IMF Says CBDCs Have Potential, but Don’t Solve Every Issue

Paul Tudor Jones says he likes bitcoin even more now, rally still in the ‘first inning’

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodward- Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency