What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 9/27/20)

|

|

WoW

|

YTD

|

|

Bitcoin

|

-0.7%

|

+50%

|

|

Bloomberg Galaxy Crypto Index

|

-0.6%

|

+73%

|

|

S&P 500

|

-0.7%

|

+2%

|

|

Gold (XAU)

|

-3.9%

|

+25%

|

|

Oil (Brent)

|

-2.4%

|

-34%

|

Source: TradingView, CNBC, Bloomberg

The Ongoing Debt Spiral

The ongoing debt spiral at both the government and corporate level has been top of mind for investors in all asset classes. Both central bank and corporate balance sheets are on a seemingly endless march upwards, and Covid-19 has simply accelerated a trend that was already in place.

While none of this is new news, let’s contextualize the rise in global debt for a minute before getting to our broader point (and I promise the end point is NOT going to be another argument for “Bitcoin protects against inflation”).

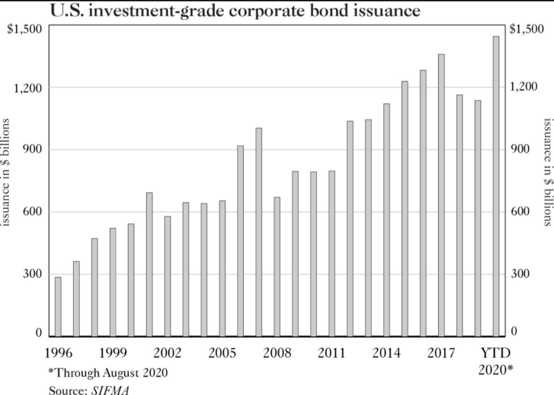

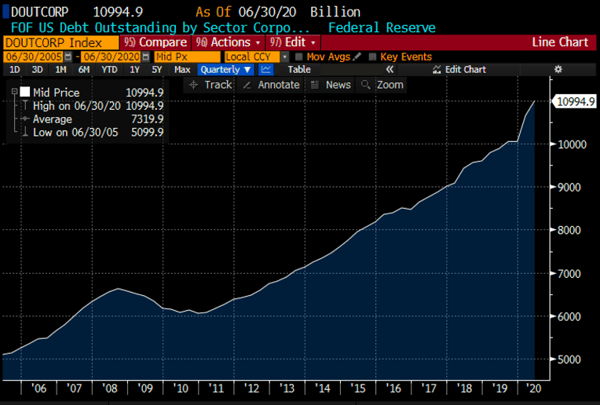

- Record corporate bond issuance in the U.S., with over $1.6 trillion investment grade debt and over $300 billion in high yield debt issued already this year.

Source: Bloomberg

Source: Bloomberg Source: Bloomberg

Source: Bloomberg

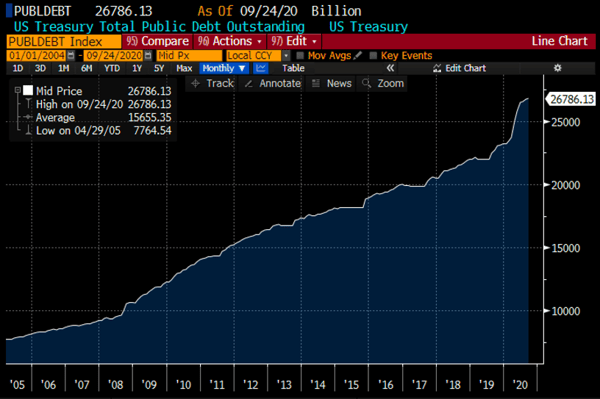

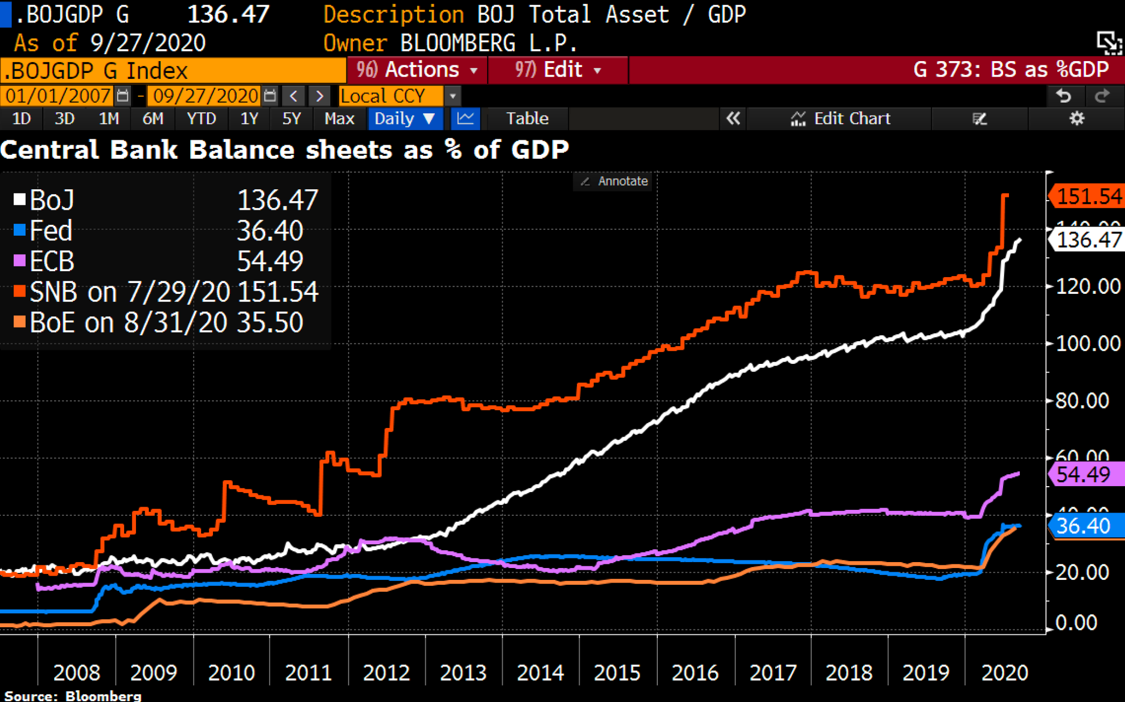

- Global Debt to GDP is now at record highs, with possibly unsustainable debt levels held at each major Central Bank as money printing continues unabated.

Source: Twitter @Schuldensuehner / Bloomberg

Source: Twitter @Schuldensuehner / Bloomberg

At record low interest rates, debt issuance makes sense, in theory. But with declining corporate profits and shrinking global GDP, the ability to service this debt is obviously being called into question. Corporate leverage is rising, and interest coverage is falling, with estimates that 18% of companies cannot cover interest expense. This doesn’t even include mortgage-backed securities, for which a wave of delinquencies and defaults are likely coming. Warren Buffett once said, "Only when the tide goes out do you discover who has been swimming naked".

One of the arguments for owning Bitcoin has always been that unsustainable government debt levels will inevitably lead to either inflating our way out of debt, or default… both of which lead to loss of purchasing power for those stuck holding fiat currencies. This chorus is getting louder, and louder, and louder, and louder. When companies and governments simply issue more and more debt to paper over a debt problem, there is no end game.

But let’s not forget that much of the government’s increased debt load over the past 10+ years is simply a transfer of debt from private to public. The 2008 financial crisis started this bailout culture, and recent handouts to both corporations and private citizens to combat Covid-19 have worsened the trend.

What if the solution isn’t Bitcoin, but rather, less debt?

Where do Tokens Fit into the Corporate Capital Structure?

- Debt = Claim on assets

- Equity = Assets minus liabilities or a claim on excess profits/cash flows

- Digital Assets = Claim on future services or customer growth (i.e. “network equity”)

Non “crypto-native” companies have yet to embrace tokens as a financing solution, for a variety of reasons including regulatory uncertainty, a lack of education, and no creative investment bankers. Worse, companies for which this is the most obvious solution, like airlines, are simply dipping further into the debt spiral playbook instead of using this more creative and customer-friendly solution. Numerous airlines, who have already received huge government loans and bailouts, recently made headlines for issuing debt backed by their loyalty rewards programs. The airline industry is already plagued with high rates of Chapter 11 bankruptcies due to unsustainable cost structures and low recoveries on unsecured debt and equities due to a lack of unencumbered assets (airlines already issue a lot of secured debt in the form of EETCs - debt backed by planes and equipment). Meanwhile, revenues and profits are plummeting as planes remain grounded.

In the case of the airlines, their equity value is declining due to lower profits, and their debt coverage is falling as they continue to layer on secured debt. But for the most part, airline customers are still around and are willing to fly as soon as it is safe and affordable. Thus, the airlines’ “network equity” and customer loyalty hasn’t decreased. Instead of searching the coffers for unencumbered assets and issuing debt against this loyalty program, they should be raising new, non-dilutive capital in the form of more loyalty programs. This is exactly how token issuance is being used in the small but evolving digital assets industry.

Unfortunately, this is complex. There are a rising number of companies and projects in the “crypto-native” world that are raising capital and bootstrapping growth by issuing “Pass-thru tokens” in an unregulated fashion, but only a handful of companies who have issued “network equity” in a fully regulated manner, which of course public companies would have to do. Both INX Global and Blockstack have issued registered securities in the form of tokens, but both of these companies are brand new startups with no existing customers or business lines. These are more like venture capital token offerings, giving investors a lottery ticket if the projects succeed. It would be much different for a mature public company or large private company to issue pass-thru or hybrid tokens, like one of the major airlines or any other business with a large customer focus (like small gym membership chains, coffee shops or local restaurants). There is something very bizarre about the S-1 filings that may influence the ability for existing companies to follow suit. Even though both INX and Blockstack filed S-1s, performed lengthy roadshows, and raised investor capital, from an accounting standpoint, these token sales are treated as revenue, not capital raises.

In the case of INX:

“The INX Token is a hybrid financial instrument. The host instrument is a financial liability due to the right of the INX Token holder to effectively redeem the INX Token in consideration as payment for services. The INX Token is considered a puttable instrument which is a financial liability in accordance with IAS 32, Financial Instruments. When the INX Token is used to pay for services provided by the Company, the respective portion of the INX Token liability is derecognized and revenue is recognized. The fair value of INX Tokens issued in consideration for services to be provided to the Company is recognized as compensation expense as the services are provided.”

And Blockstack:

“Blockstack characterizes portions of the proceeds of the private placements of Stacks Tokens as revenue. Specifically, Blockstack recognizes revenue from previous sales of Stacks Tokens over the estimated period in which Blockstack is performing development services under the contracts. Blockstack uses a cost to cost method of measuring progress toward complete satisfaction of these obligations, and based on this methodology, these sales yielded a total of $0.4 million of recognized revenue and $7.4 million of deferred revenue in 2017, and $34.5 million of recognized revenue and $2.5 million of deferred revenue in 2018. As a result, substantially all of the revenue Blockstack recognizes comes from our sales of Stacks Tokens. The remainder of the proceeds of Stacks Tokens sales is not recognized as revenue because these proceeds remain subject to the achievement of a future milestone. Proceeds from Stacks Tokens sales subject to milestones are recognized as restricted assets on the balance sheets included in Blockstack’s consolidated financial statements.”

As is always the case with new technologies, the waters are murky. We are arguing that tokens are part of the capital structure, but in order to fit a round peg through a square accounting hole, companies to date are issuing tokens as deferred revenue. We need more companies to act as pioneers, especially those with large enough legal and accounting teams to get greater clarity. While this is slowly happening completely under the radar with firms like INX and Blockstack, the market is now awaiting a more mature company to push the envelope further and establish repeatable legal and accounting frameworks that make more intuitive sense. As my friend Maartje Bus opined, recent market dynamics are begging for solutions like this to level the playing field and help companies grow again.

Unless of course you think more debt is the best solution to unsustainable bad debt.

What’s Driving Token Prices?

For those that don’t take it upon themselves to watch each tick, this week may have seemed like a bit of a snooze fest - Bitcoin barely budged week over week (-70bps), the rest of the market seemingly kept pace (BTC.D -25bps), and there was even some strength shown by alternative assets (34 out of the Top 100 finished 10%+). For the rest of us, this week had more twists than an M. Night Shyamalan thriller. A rocky start to the week drove the Digital Assets market down 9% (-$30 billion), and then midway through, the market took a metaphorical pirouette, rallying 8% into the weekly close. Beyond all that noise there was quite a sneak peek into what the future of this market may entail:

- Synthetix (SNX) was notably active this week, starting with a cryptic tweet from the founder himself regarding a potential fix to the high gas prices encountered while using DeFi. On Thursday, they released a blog post announcing an incentivized test net trial of the Optimistic Ethereum Layer 2 solution. This has been a long time coming, as ETH gas fees have become cumbersome to smaller users (flat fee costs hurt the little guy) with the rapid rise of decentralized finance. The market reacted favorably to SNX being the potential pioneer of the L2 scaling solution the space has been waiting for, with SNX finishing the week up 23%.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodward- Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency