In lieu of our traditional "That's Our Two Satoshis" format, this week we will be focusing on mid-year predictions.

At the midpoint of the year, we’re assessing how these predictions have fared thus far, what changes are expected to transpire going forward, and introduce a few new predictions for the rest of 2021 and beyond.

Post Mortem 2021 Predictions

“Thematic investing will once again be a major driver of 2021 investment gains.” Specifically:

- Digital Money (growth in stablecoins)

- NFTs / Gaming

- Digitization of the Fan Experience

- Web 3.0 / Lack of Middlemen

- Growth in India

At the midpoint of the year, thematic investing has clearly impacted returns, as year-to-date returns by sector show clear dispersion. In January, DeFi was the best performing sector. In February, CeFi outperformed. In March, “Fan Experience” or “Social tokens” outperformed heavily. And in April, “cryptocurrencies” rallied the most (though that was largely driven by DOGE, not BTC).

|

Sector

|

YTD returns

(through June 30, 2021)

|

|

Currencies (Digital Money)

|

+216%

|

|

Protocols / Platforms

|

+305%

|

|

Decentralized Finance (DeFi)

|

+409%

|

|

Centralized Finance (CeFi)

|

+637%

|

|

NFTs / Gaming

|

+580%

|

|

Web 3.0

|

+224%

|

Source: Messari

Four of our five identified themes have seen rapid growth, with our views on India being the most inaccurate:

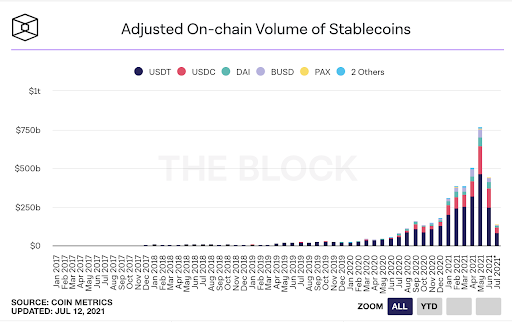

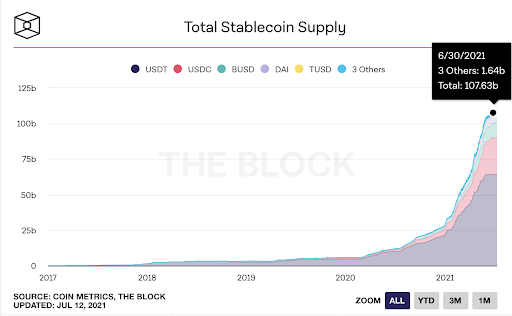

Stablecoin AUM grew from $28 billion at the end of 2020 to over $100 billion on June 30, 2021, and on-chain transactions grew 10x over 2020. We continue to believe stablecoin growth will accelerate in the second half of 2021. The recent Circle $4.5 billion SPAC confirms the interest in these assets.

Source: The Block

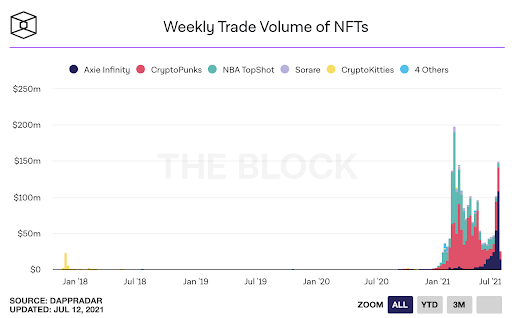

NFT / Gaming assets became household names, with NBA top shots starting the craze, and Axie Infinity and OpenSeas taking the torch. Some of the best performing tokens mid-way through the year came from this sector, including AXS (+857%), ENJ (+747%), and SAND (+553%).

Source: The Block

The digitization of the fan experience became more widely known as “social tokens,” and began to see strength as real world use cases unfolded. This sector penetrates sports, music, celebrities/influencers, and individual athletes. Some of the best performing tokens mid-way through the year came from this sector, including CHZ (+1121%), RLY (+313%), and AUDIO (+389%).

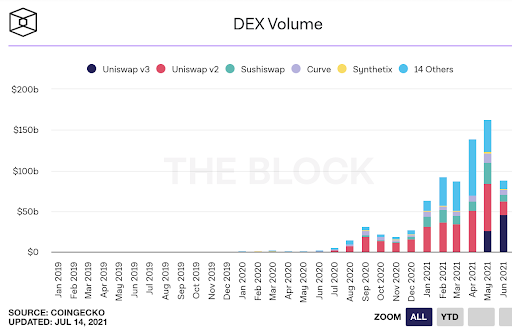

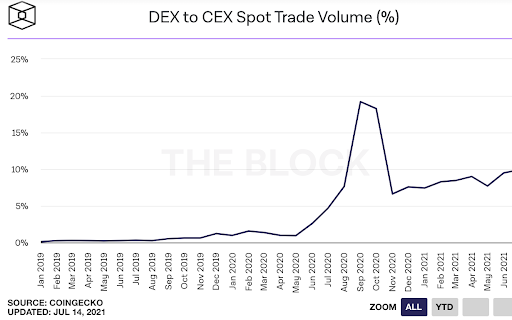

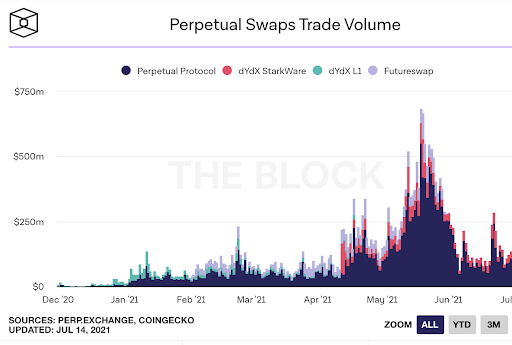

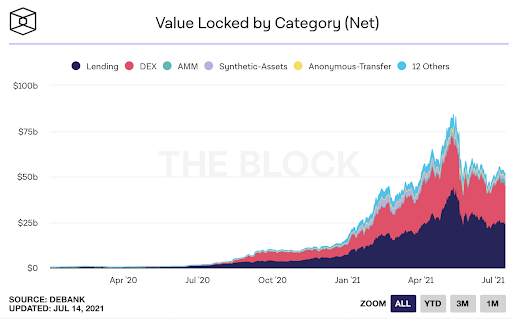

While Web 3.0 is the hardest to measure since it is so broad, we are clearly seeing a shift away from centralized intermediaries and towards decentralized entities. DeFi, which is a sub-sector of Web 3.0, has dominated, with Decentralized Exchanges (DEXs) gaining significant market share over Centralized Exchanges (CeFi) and their tokens following suit (UNI +302% / SUSHI +142%). We’ve also seen a rise in decentralized derivatives (PERP +599% / HXRO +238%). Similarly, we saw pockets of growth in telecom (Helium +830%), video (Livepeer +1258%), and file storage (Arweave +288%).

Source: The Block

- “Specific narratives will shape the investment landscape”:

- “Asset-backed” tokens will attract new investors

- “Community tokens” will outpace “VC tokens”

- Value tokens will outpace growth tokens

- A growing priority will be placed on transparency and governance

- Redistribution of Wealth

This is less quantifiable and therefore more difficult to measure, but we believe we have been right about value-investing and asset-backed tokens, and incorrect about Community tokens versus VC tokens and governance.

Bitcoin only experienced a +21% gain in the first half the year, making it one of the worst performing digital assets in the market, and the cryptocurrency sector itself was the worst performing sector. This is notable because currency is the only sector that has no cash flows or yields. Conversely, CeFi, DeFi, and NFT/Gaming were the best performing sectors, and they share a commonality - real revenues, real cash flows, and tokens that accrue economic value directly. While Arca has always maintained financial models for our investments, this same focus on financial modeling has only recently become mainstream, and we can thank firms like Token Terminal and Dune Analytics for helping push this initiative even further by introducing great dashboards with P/S, P/E, and other metrics. We believe this bifurcation will accelerate into the second half of 2021, as frankly, this industry can’t remain “dumb money” forever.

The high dividend yields and low multiples for growth assets are too significant for traditional investors to ignore. Why own Root or Lemonade when you can own Nexus Mutual at a fraction of the valuation? Why own Acorns when you can own Yearn Finance at the same valuation, but with a much faster growth trajectory? The only thing stopping investments into these growth / value assets is infrastructure, and that is quickly being solved with new entrants from Goldman Sachs, Morgan Stanley, BNY, State Street, and plenty of other incumbents. We believe value investing is a natural next step.

Conversely, we are still underwhelmed by transparency initiatives taken by issuing companies. Most companies / projects still don’t understand, or care, about transparency, which is perpetuated further by venture capital firms who use the lack of transparency to their advantage by quickly buying tokens at undisclosed discounts in order to dump them on unsuspecting retail investors who lack the same information. There have been a few positive steps towards transparency though - MakerDao (MKR), Yearn (YFI), Hegic (HEGIC), Aave (AAVE), Binance (BNB), Nexus Mutual (NXM) and a handful of others have begun to issue their own unaudited financials to their communities. This look behind the curtain makes it incredibly easy for token investors to track the progress of their favorite investments. For example, Axie Infinity, one of 2021’s biggest winners to date, began to outperform once they put their metrics on chain for everyone to see. Providing transparency allows investors to participate in this rerating, and token issuers are rewarded for it.

However, governance has largely been a failure to date, either because there isn’t anything worth voting on, or because truly democratic voting processes are blocked by highly concentrated ownership and voting powers. We also continue to see many companies intentionally hiding their financials, including privately held centralized companies like Celsius and BlockFi. Regardless, our research team believes transparency initiatives are necessary, but our prediction was certainly too early.

New Predictions for the Remainder of 2021 and Beyond

While our investment team still strongly believes in our original 2021 predictions, we’d be remiss to exclude our recent findings and updated outlook for the rest of this year.

#1: Rewards and Play-to-Earn will continue to encourage usage

When companies with a digital asset in their capital structure grow, they often grow at unprecedented rates. The BNB token is the main reason behind Binance becoming the fastest growing company in history (estimated value of $100 billion in under 4 years). Tokens provide a coordinated incentive mechanism via rewards for being an early adopter and a power user. Similarly, play-to-earn models turn sweat equity into actual equity, as it aligns players with games in a way that has never been done before (this model is behind Axie Infinity’s mind-blowing growth). We believe this model will continue to evolve, and be replicated, over the next six months as incentive based token structures will outperform those that have no utility. Ultimately, this model will likely pave the way for traditional non-blockchain based companies to begin issuing tokens as well, i.e., airlines, restaurant chains, barber shops, etc.

#2: The rise of "G" in ESG for digital assets

ESG is a growing investment theme throughout all industries. It speaks to investors’ universal interest and active promotion to build a more sustainable future. However, when the ESG investment conversation is directed at the digital asset ecosystem, the rhetoric is often misguided and arbitrary. We believe the discourse surrounding digital assets’ negative ESG impact, that is primarily focused on Bitcoin and the Environment, will turn its attention to digital assets / blockchain’s main purpose - Governance, and align digital assets with a positive ESG investment valuation. The birth of the digital asset ecosystem, with the Bitcoin whitepaper in 2008, was to solve problems derived from the abuse and ensuing mistrust of centralized authorities within the financial system - Environmental and Societal impacts are secondary bystanders. We foresee a rise in governance tokens, especially in DeFi.

As investors in digital assets, we feel an obligation to be stewards of responsibility and transparency, and to hold companies and project leaders accountable for their actions. When promises go unfulfilled, spending is irresponsible or misreported, or new endeavours are started and stopped without discipline or recourse, we as token holders can and should demand answers. We have constructively engaged with Gnosis, and most recently, Sushiswap, offering operational changes in an effort to help to deliver better results for token holders. Decentralized project models are still in their infancy, but we predict the token management and community will recognize the power of these governance structures and help administer effective products, incentives, and value.

#3: Passive income / yield — Staking-as-a-service

Historically, every new digital asset investor began their journey by touching BTC or ETH first. Anecdotally, we’re beginning to see a changing of the guard. From Wall Street write ups on Uniswap, Nexus Mutual, and Axie Infinity, to OTC desks onboarding new clients directly into DeFi assets, to our own hedge fund inflows from first time investors, it’s clear that value investing is starting to take precedent over “betting on a technology.”

With this in mind, and coupled with the fact that Treasury and corporate bonds are once again at all-time low yields / spreads, the search for yield will continue to find its way towards digital assets. Staking-as-a-service, along with certain DeFi farming opportunities, will likely begin to attract new money from investors who want to replace the safer, high single-digit yields that are no longer available in traditional finance.

This naturally leads to structured products, and there are a few digital asset companies / projects that are tackling this currently, however, we think it’s too early for structured products to take off. For starters, the risk tolerance is inverse to that of Wall Street packaged products. In traditional finance, no one wants the equity tranche (so the sponsors typically keep it), but there is high demand for the AAA and BBB tranches. In digital assets, most investors currently in this ecosystem want the high octane equity tranche, but there is no demand for the low yielding “safe tranche”. The biggest difference is that traditional finance has rating agencies, and decentralized digital asset projects do not. Until that is solved, yield opportunities will likely continue to be variable and require active management.

#4: The Rise of POAP

Proof of Attendance Protocol (POAP) provides event nomads with a way to verify their attendance through collecting digital badges, all of which live on chain. Each badge is unique, meaning that the only way to claim one is to physically, or digitally, receive it at the event. With the world opening up post-Covid, and millennials still valuing experiences over assets, we expect a return in force to live events. As such, POAP tokens may become much more heavily used in the second half of 2021 as bigger projects, artists, and influencers get into the NFT space. This will become proof of who was an "early adopter/believer", and these super fans can be granted access to certain exclusive goods, information, and experiences.

#5: Real world assets will continue to become collateral on blockchain

There are a few companies / projects tackling this enormous task, such as Centrifuge, Figure, Percent (formerly Cadence) and even MakerDao. This is the holy grail of decentralized finance, as it would allow more financing activity to take place on chain using traditionally owned assets as collateral instead of just today’s digital assets. For example, it makes no sense that Bitcoin can’t be used as an asset to get a home loan, but neither can your jewelry or your car. Similarly, it makes no sense that you can’t use your home equity to get a loan via DeFi. Bridging these two worlds is probably a few years away, but we expect to begin to see a few viable proof of concepts by the end of this year.

#6: DAOs = Idea Machines

Decentralized Autonomous Organizations (DAOs), are collections of individuals organized around a set of rules or beliefs. Built on a public blockchain, DAOs typically integrate around a token that provides the holder with governance rights over the entity. Think of a DAO like the government of a town, city, or country, with a constitution of rules determining the mission of the government and the rights of people residing within it. While we have only seen DAOs in their earliest iterations so far, we believe the current landscape represents a glimpse into a new form of human organization that will coordinate resources more efficiently and fairly than ever before.

Like governments and companies before them, DAOs can become self-sustaining organizations, but rather than providing rights or goods/services to society, they will spread and monetize ideas. For example, a DAO could organize around a political belief, such as environmental justice, with all members holding a native token. The inherent value of governance rights means the token can increase in value as the organization obtains more power and greater membership. A token creates a financial incentive for early members to grow the organization and to contribute by advancing causes that the membership believes in. Like the printing press or the Internet, DAOs have the potential to make ideas spread across the globe more quickly and pervasively than ever before. Whereas those innovations increased the ease of spreading information, DAOs incentivize the spreading of ideas.

#7: Ethereum is Evergreen, Competitors Fair Weather

In the first half of 2021, we saw the Ethereum Network at capacity - gas fees went from 40 GWEI to as high as 1400 GWEI (35x), congestion was at an all time high, and users were being priced out as the combination of yield farming, Priority Gas Auction (PGA) bot arbitrage, and the rise of NFTs led to a hypercompetitive positive feedback loop. This gave rise to a plethora of competitor chains (SOL +2928% YTD peak, BNB +1688% YTD peak, AVAX +1400% YTD peak, ETH +500% YTD peak) as well as the explosion of Layer 2 projects (Arbitrum, Optimism, Starkware, and Polygon) which looked to tap into the pain points experienced on Ethereum.

However, with the shift in the overall market structure - yield farming largely compressed, PGA bots taken offline, and price decrease - gas fees rest at 32 GWEI currently. The immediate demand for a competitive Layer 1 chain for cheaper fees, faster transaction times, better yields, or other reasons entirely has waned. With the increased development of Layer 2 technology, EIP-1559 looking to come online in August (cheaper fees for users), and the eventual shift to ETH 2.0, the value proposition for some of these niche alternatives begins to shrink.

We continue to believe that there is space for competitor chains that serve niche products to niche users for the specific desires mentioned above, and with any congestion issues on Ethereum they will once again catch the spotlight. In the same vein, we also believe that Ethereum has gained and earned the lion’s share of attention in this sector, and while other projects wax and wane, Ethereum remains evergreen.

The continued growth of the digital asset ecosystem provides an abundance of interesting projects and trends to investigate and evaluate. We, at Arca, eat, breath and live this world, and promise to keep our readers up to date with our newest insights. Check back in another 6 months for our market progress report and more future predictions.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

Andew Stein, VP of Research

To learn more or talk to us about investing in digital assets and cryptocurrency