What happened this week in the Crypto markets?

Moral Hazard… here we come!

Fresh off the heels of one of the best months ever for crypto, and one of the worst months for stocks, the first week of June saw a stark reversal. So the question is, “Are crypto investment opportunities expanding”? After declining for four straight weeks in May, stocks rebounded with 4-5% gains last week as monetary policy re-entered the spotlight, pushing aside the more recent trade policy narrative. Market participants are now anticipating at least one rate cut in 2019, and Fed Chair Powell stated publicly that policymakers “will act as appropriate to sustain the expansion” in light of recent trade developments. Similarly, ECB President Draghi reiterated that the central bank stands ready to implement any necessary policy tools, including rate cuts or the extension of quantitative easing to bolster growth in the region. Moral hazard -- thy name is Central Banks.

Meanwhile, crypto markets gave back some of May’s startling gains, as volatility increased and volumes decreased. The week began with Monday’s sharp 11% peak-to-trough drop in Bitcoin, and for the remainder of the week we bounced in a wide range, ultimately ending the week near the lows. We still believe the market is in “buy the dip” mode, as we once again saw strong support at lower levels. That said, this can change quickly, and the market has an “uneasiness” to it right now that didn’t exist a few months ago. Stay tuned.

It’s Time to Think Rationally and Not Emotionally

Growing up, there were 3 topics that your parents told you not to discuss publicly: Politics, Religion and Money. With apologies to whoever we stole this from (can’t recall the source), one of the reasons crypto is such a divisive topic is that it touches on all 3 simultaneously. Emotions run very high in the crypto world.

“No coiners” hate Bitcoin

Bitcoin supporters hate Ethereum

Ethereum supporters hate EOS

EOS supporters hate Tron

Believers in dececentralization hate Facebook Coin (now called “Globalcoin”)

Everyone hates JP Morgan Coin

The list goes on and on. But as investors, we’re taught to be objective. The best companies may be terrible investments, and the worst companies may be great investments. Emotions can prevent rational interpretation of facts, and may cloud better judgement. These biases are difficult to overcome. For example, if you own Apple stock, you’re far more likely to believe Apple is going to perform well than if you don’t own it; the fact that you already own it can influence your expectations (otherwise known as “confirmation bias”).

To many, “crypto” simply means “decentralized money”. No matter how this space evolves, doubters will think this is a ponzi-like fraud, while believers think Bitcoin (or a competitor) will be the only token that ever accrues value. This ideology is buoyed by the fact that Bitcoin still represents over 50% of all digital asset wealth.

To others, “crypto” is a catch-all that implies placing any assets on a blockchain. The phrase “tokenize the world” has developed as a rallying cry to support the notion of creating digital representations of assets that would trade like securities, and would replace existing, outdated infrastructure. This Security Token argument is meant to distermediate the countless middlemen in finance, and is fueled further by the large number of financial incumbents entering the crypto arena.

The problem with the former argument is that by focusing only on crypto as money, and Bitcoin specifically, those who are already in the digital asset ecosystem have missed out on some truly great and innovative investment opportunities. The problem with the latter is that there are very few successful Security Token Offerings (STOs) to date, and certainly nothing sexy enough to make traditional investors feel like they are missing out by not investing.

Let’s Call a Spade a Spade

A recent Forbes article highlighted how little progress the Security Token movement has made. While there are over 150 tokens that are meant to be digital representations of an asset and are clearly securities (unlike Bitcoin and other decentralized “money” tokens), liquidity is so poor in these STOs that it is difficult if not impossible to invest in them. To be blunt, this effort is not happening as fast as supporters had hoped. But the problem is not that these tokenized security offerings are bad ideas, the problem is lack of product/market fit. These STOs are run-the-mill securities issued in a digital format. So who is the natural buyer? Your typical crypto investor doesn’t care about 10-20% annual returns, as they are trying to make 10-20% per day trading unregistered tokens on unregulated exchanges, and likely wouldn’t put in the work required to analyze a real security. So that leaves traditional investors, but these investors aren’t going to jump through hoops to buy tokenized versions of assets they can already buy via the stock and bond markets.

In order to change this product/market fit problem, 1 of 2 events has to happen:

- We have to wait until more traditional investors become comfortable with owning digitized securities. This may happen as a result of JPM Coin, or Facebook’s GlobalCoin, or Fidelity Digital’s Bitcoin trading and custody platform, as these financial giants are going to introduce digital wallets and peer-to-peer electronic asset transfer to billions of people. Once onboarded and comfortable, traditional investors will be more likely to look within this new ecosystem for other investable offerings - like tokenized real estate, equity and debt.

- Some beloved company or asset will become a pioneer, offering a tokenized asset that will blow people’s minds, and leave investors no choice but to enter the digital assets world to buy it. Similar to 2004 when Google decided to forego the typical underwritten IPO to instead pursue a Dutch Auction because, well, they’re Google and they assumed investors would buy anyway… we now need the same type of renegade to issue a digital stock or bond that they know investors will buy. Maybe Amazon (AMZN) or Domino’s Pizza (DPZ) tokenizes its equity, or ownership of the Mona Lisa is auctioned off as a digital security (thanks to Tim Enneking at Digital Capital Management for this idea). Whoever does it, it has to be such an impressive investment opportunity with such high demand that investors will be forced to figure out how to invest in it.

In the meantime, there is something interesting happening. While STO proponents are waiting around for their market to blossom, and Bitcoin maximalists are arguing against all other non-Bitcoin tokens, there is a grassroots STO market taking off right under their noses.

Legally call it whatever you want, but Binance (BNB) and Bitfinex (LEO) have tokens that, for all intents and purposes, are securities. Without getting into a religious, political or money debate here, it doesn’t matter whether or not these tokens would pass the “Howey test”. And it doesn’t matter if these tokens are decentralized utilities or financial securities. What matters is, from an investor’s standpoint, these are absolutely fantastic digital representations of cash flows that are making investors a ton of money. LEO is now up 85% in 3 weeks since being issued, and BNB is up over 400% YTD. Both are issued by revenue producing companies, with enormous margins and high FCF, and their tokens look and feel like real securities that can be valued using traditional financial modeling techniques. They both offer cash flow sweeps (token paydowns) based on a proportion of revenue, giving investors a form of a dividend and a higher “downside floor”. Everything about these tokens scream “Financial security” -- except to those who are still waiting for regulated security offerings, and those who deny their very existence.

Now, you can argue all you want that the underlying companies (Binance and Bitfinex) wouldn’t exist if not for Bitcoin, and certainly wouldn’t exist if crypto somehow went away. But until that happens, there is no denying that these tokens have real economic value. And these are just two examples of many where value is accruing in crypto, and how the market is changing and adapting away from just underlying technology and towards financial engineering.

So instead of arguing about why Bitcoin should or should not exist, or why we need to tokenize the world, a much more rational response is to accept that crypto does exist, and find opportunities like BNB and LEO that spawned from this great monetary and technological achievement. It’s time to think rationally and not emotionally.

BNB & LEO Tokens are Rewarding Investors

Welcome Arca’s Newest Intern - A Case Study for Modern Times

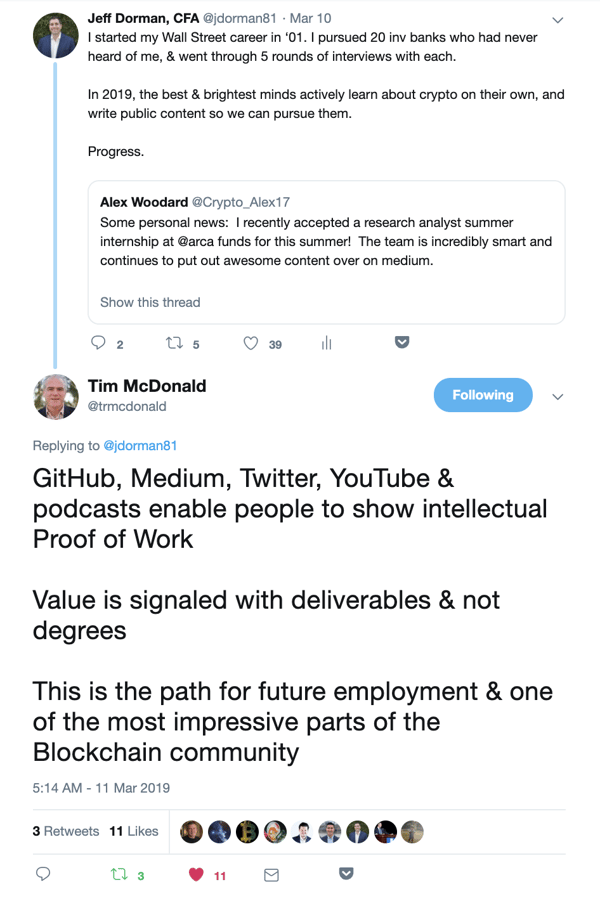

Last week, Arca welcomed its newest intern, Alex Woodard. Alex is a remarkable young student at Whitman College, studying Economics and Finance. But Alex didn’t send resumes or cover letters. In fact, he didn’t even apply at all. We found him on Medium, writing about digital assets in his spare time. When we first reached out to Alex, we had no idea he was even a student -- we simply wanted to get to know the person who wrote succinctly about this new space, and pick his brain on his investment thoughts.

Crypto was built on open-source code, democratization, and the removal of middlemen. It’s only fitting that crypto recruitment is open source as well. Tim McDonald said it best: “Value is signaled with deliverables and not degrees.”

Notable Movers and Shakers

As Isaac Newton’s Third law infers, all things that go up must come down. Gravity is not escapable - not in physics, and not in the digital assets space. Since April, Bitcoin has been on a tear (+87%) and as such it is easy to get complacent with the gains and irritable whenever those gains subside. Therefore, with Bitcoin finishing last week down 11%, it is prudent to take into account the run we have had in these last few months. That being said, there were notable outliers in this downward move that stood out:

- Unus Sed Leo (LEO) has shrugged off the market this week, moving on its own terms (+24%). The Bitfinex ecosystem token has been on a tear since listing at $1.00 in May, with the Bitfinex CTO tweeting about a transparency page coming for LEO and other exchanges beginning to list LEO for trading. This token continues to be a hot topic, and we very well could be seeing more from it in the coming months.

- Tron (TRX) and Bittorrent (BTT) both had a humbling week (-20% and -25% respectively) after Justin Sun, the CEO of both projects, tweeted that his big announcement was that he won a $4.5M bid for the 20th annual charity lunch with Warren Buffett. Many were left disappointed, pointing out that the bid frivolously used investor money. Buffett has been outspoken on his negative attitude towards cryptocurrencies, most notably stating that they will “come to bad endings” at his annual shareholder meeting in 2018. It remains to be seen what the outcome of such a sit-down will be, but what is worth noting is that Justin Sun effectively tied his projects to this outcome.

- World Asset Exchange (WAX) came out of the woodwork last Friday, as volume went up from $1M to $40M before settling back down into Sunday. This volume spike did not come without rewards (+17%), as the WAX mainnet approaches on or before June 30th. The WAX team explained what the mainnet will mean for both the token and the ecosystem in a blog post a few weeks ago.

What We’re Reading this Week

Another sign that the world of crypto is slowly seeping into traditional finance: Cadence, a blockchain-based debt instrument, was assigned a Financial Instrument Global Identifier (FIGI). FIGI records metadata in Bloomberg’s trading terminal meaning it will make it easy to research and trade Cadence. Cadence puts high yield, short-term commercial debt into ERC-20 tokens allowing investors easy and transparent access to this asset class.

Late last week, a severe crash in the price of the CLAM token caused margin traders to lose $13.5m. In response to the liquidations on traders accounts, Poloniex froze the accounts of the borrowers until they are able to pay back the amount owed. Poloniex explained the losses were incurred due to a combination of illiquidity in CLAM and the “velocity of the crash”. Exchange risk remains the biggest risk to crypto investors right now, but this was just outright irresponsible. Small, illiquid tokens like CLAM should never have been available on margin in the first place.

Startup Moneybutton launched a new feature last week -- Paymail, which allows users to substitute an email address for a bitcoin address. To send or receive digital assets, individuals must use a public key consisting of a long string of random numbers and letters looking something like this - 4dEICdk367mndDfu7noxk592nfdDOKue48wt. These public keys are difficult to remember and are easily mis-typed. Paymail allows senders to use an email address instead of a public key to send cryptocurrency. Though this feature has only been implemented on Bitcoin SV, this is an advancement that many argue is needed for mainstream adoption of crypto.

The company behind the blockchain-based MLB game, Lucid Sight, just signed a deal with CBS for the rights to bring Star Trek into its gaming universe. Specifically, the U.S.S. Enterprise and other Star Trek ships will be available in Lucid Sights’s space-based multiplayer game, Crypto Space Commander (CSC). Eventually Star Trek items will be available for purchase within the CSC game.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

To learn more or talk to us about investing in digital assets and cryptocurrency

.jpg)