What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

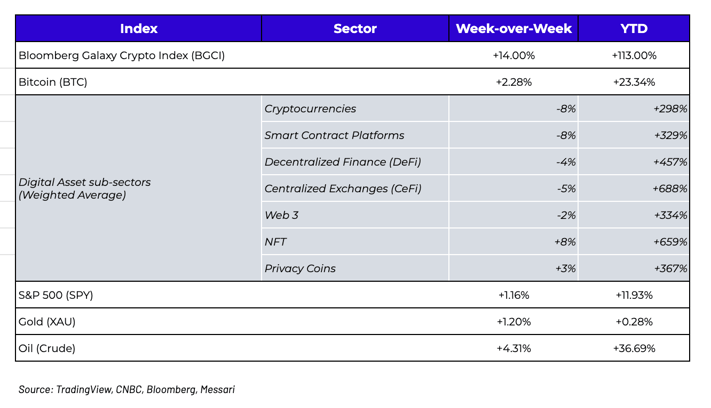

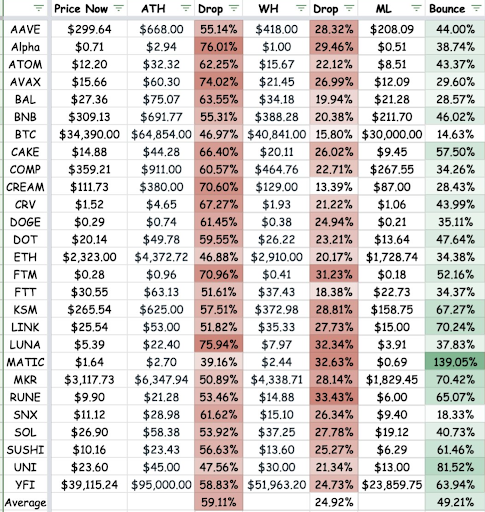

Week-over-Week Price Changes (as of Sunday, 5/31/21)

The Negative Bitcoin Vortex

On the heels of one of the worst weeks in digital assets history, all attempts at a rebound last week were quickly met with selling pressure. But one asset performed particularly poorly… Bitcoin. Not necessarily in terms of absolute performance per se, as BTC bounced with the market and fell with the market multiple times during a very volatile and highly correlated week. But in terms of upside and downside beta, very few digital assets performed worse than Bitcoin.

The table below, courtesy of Darren Lau, shows the breadth of the declines and the ferocity of the snapback during May. On average, digital assets fell 59% from their all-time-highs (ATH) this month, and fell 25% last week from their weekly highs (WH), but bounced back 49% from their monthly lows (ML) a week ago Sunday. From an upside / downside standpoint, it means most assets bounced back pretty aggressively, in almost a 2:1 ratio last week, from their sharp declines, while Bitcoin fell 15% and only bounced back 14%, a ratio of 1:1. Risk/reward investing is all about ensuring that your downside risks are commensurate with your upside risks, and for the time being, the data shows that Bitcoin has equal downside risk, but less upside, than other digital assets.

Now, this does not mean Bitcoin is a bad long-term investment. Bitcoin is still a very binary investment, akin to a call option. Bitcoin will either become a global currency/store of value in which case the price of Bitcoin should go up 10-25x to reach the size of the gold and fiat currency markets, or it’s going to fail miserably and eventually go down close to 100% in dollar terms. From that standpoint, BTC still has a very asymmetric positive return profile, and the path it takes to get to either extreme scenario ultimately doesn't matter much even if last month’s negative news lowered the probability of success and increased the time it will take to succeed (thus decreasing the option value). But it does mean that everything you’ve heard and read about Bitcoin versus other digital assets is empirically false. Bitcoin is not safer than other digital assets, nor does it protect or shield you during selloffs. In fact, currently, you could make the opposite observation -- that many other digital assets are shielding you from the negative Bitcoin vortex.

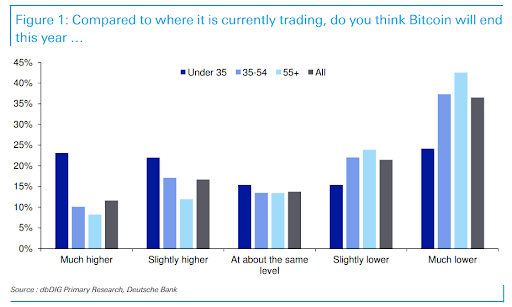

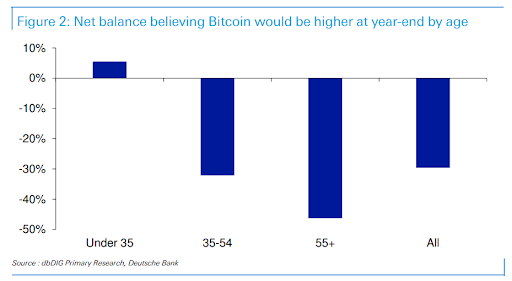

And this change in up/down capture makes sense, intuitively. All of the negative news lately, which has weighed heavily on sentiment, is pointed directly towards Bitcoin. The ESG crowd is pointing solely towards Bitcoin’s energy usage and proof of work mining, government regulation and the Chinese crackdowns are pointing solely towards Bitcoin mining, and the Fed-induced taper tantrum fears will disproportionately affect Bitcoin as a macro asset. With that backdrop, it makes sense that Bitcoin is struggling (short-term), especially since no one can value Bitcoin and it’s largely just guesswork, driven by pre-existing biases. Per Deutsche Bank:

“Overall, a net 30% thought Bitcoin would be lower than the current levels into year end. However, that masks a big divide by age. For over 55 year olds, a net 46% thought it would be lower and 43% of these felt much lower. However, for the under 35 year olds, a net 5% thought it would actually be higher. So a huge swing.”

Source: Deutsche Bank survey

So Why are non-BTC Digital Assets Going Down?

We often compare digital assets to ETFs, in that the underlying structure (a token) is similar to the underlying vehicle (ETFs), but price performance is driven by what is inside the structure, not the structure itself. Meaning, you’d never hear someone say “ETFs are down this week”, because that wouldn’t make sense. Were healthcare stock ETFs down? Or were Gold ETFs down? Or were high yield bond ETFs down? Each of these different types of ETFs are affected by different factors. Digital assets should be similar. The factors affecting ETH are different from those that affect BTC which are different from those that affect gaming tokens, NFT tokens, and Web 3.0 tokens, and the only commonality is that they are all tokens.

In April and through the first half of May, we did in fact see Bitcoin struggle at the expense of other assets, as the selling pressure (and the negative news flow) was targeted towards Bitcoin. It was only over the past two weeks where the weight of Bitcoin’s declines finally caught up with the rest of the market. The question is, “why”?

If this selloff was entirely at the expense of Bitcoin, we’d expect at least a greenshoot or two from other assets or sectors that have nothing to do with the success or failure of Bitcoin and digital currencies. The factors driving growth and adoption of gaming, DeFi, NFTs, smart contract platforms and CeFi have very little to do with Bitcoin, and the returns reflect this bifurcation. Each of these sub-sectors of the digital asset universe have risen 300% or more YTD, while BTC itself stands at just +23% YTD.

This return dichotomy was somewhat masked in the first quarter as every asset went higher, but now that Bitcoin is declining, the digital assets industry is about to see its first true bifurcation test. Can other pockets of this industry still grow even if Bitcoin temporarily lacks positive catalysts? They should, as fundamentals for every other type of digital asset other than currencies are flat out exploding higher right now.

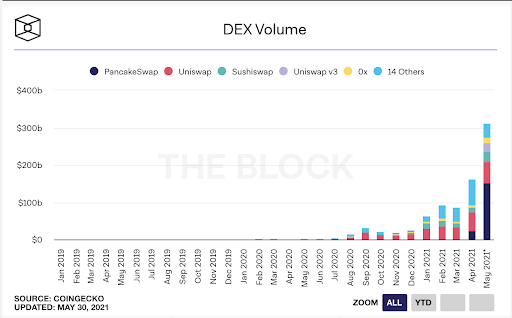

For example, decentralized exchanges (DEX) are growing faster than ever. Not only are volumes at record-breaking levels, but DEX volume as a percentage of traditional centralized exchanges (CEX) is also at all-time-highs. The same argument is true for NFTs, DeFi, gaming and plenty of other sectors, and the tokens issued by these companies and projects are outperforming BTC as a result. With more eyes than ever on this asset class, this should lead to value investors flocking to these other sectors even if traders and macro funds pullback from Bitcoin. And the fact that digital assets just withstood a nasty correction, and emerged unscathed as a financial system with no outside assistance, is being heavily discussed in institutional circles.

The only rationale for the recent spike in correlation is that this has nothing to do with the underlying assets themselves, but rather, it has to do with who owns them. Two seemingly uncorrelated assets can have extremely high correlations if they are owned by the same owners. An example of how this impacts correlations can be seen with the stocks held by Archegos, as correlations changed based on circumstances. On the surface, there was very little correlation between Baidu, Discovery, Tencent Music, and Viacom/CBS stocks. But these correlations rose once a single investor (Archegos) owned all of them and was forced to sell all at once. This is a similar dynamic to what is happening with Bitcoin and other digital assets. The more traditional investors try to get exposure to "digital assets" through just BTC and ETH, or through macro trading desks, the more their investments become highly correlated when momentum shifts.

On the flipside, Bitcoin is now owned by the entire world (corporations, individuals, hedge funds, mutual funds, banks, governments) whereas protocol, platform, sports, NFT, Gaming, Web 3.0, DeFi, CeFi and other digital assets are largely owned by an entirely different user base, depending on where they live, and what venues they trade on. For example, Robinhood announced that they have 9.5 million crypto users on their platform now, but Robinhood only lists seven digital assets (largely 2017 legacy tokens like BCH, ETC, LTC, DOGE, BSV in addition to BTC and ETH). Paypal only lists four assets -- BTC, ETH, LTC, BCH. Even digital asset native companies like Kraken, Gemini, Coinbase, Binance and FTX all have completely different tokens available on their platforms. As a result, these assets become related not by what they do, but by who has access to them.

Correlation between assets will naturally go down as ownership groups continue to differentiate. But at the same time, when/, if something changes with regard to one of these specific user groups, like the recent change in retail sentiment and forced leverage, unwinds on futures exchanges, these correlations can pick up quickly and drastically. The commonality right now may just be that a majority of these assets are owned by the same retail investors, and retail investors have been disproportionately hurt by this selloff while institutional buyers have been on strike. As the indiscriminate and forced retail selling subsides, and new buyers begin to put money to work, we should see greenshoots in the assets and sectors that are growing like wildfire.

Gross Domestic Product (GDP) measures a country’s total economic activity, where GDP = C + I + G + (Ex - Im). In theory, these inputs offset each other… as personal consumption rises (C), government spending falls (G). As business investment picks up (I), Imports (Im) exceed Exports (Ex). Similarly, the GDP of network economies like Ethereum are made up of economic inputs like DeFi, gaming, stablecoin transactions, NFT minting, etc. Unless you think the entire GDP of digital assets is declining, there should be pockets of strength that offset weakness. Perhaps DeFi transactions go up as stablecoin transactions go down, or interest in gaming goes up as interest in trading subsides. And the flock of new investors to this asset class will be looking for these diverse economic drivers rather than simply regurgitating past narratives of high correlations.

Money is everywhere

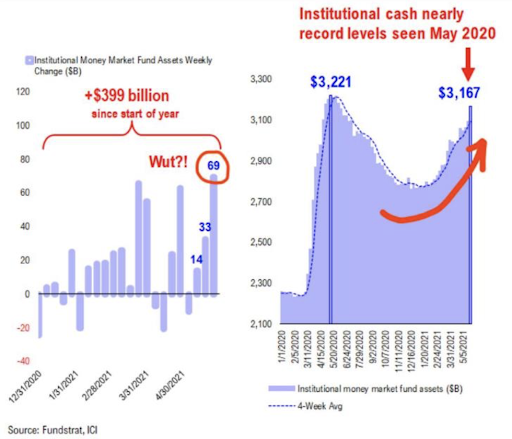

So where are these new investors? First, it takes time for assets to get wired into funds and OTC desks, and just about every institutional onramp is reporting large inflows and new customer business, with the bulk of it coming June 1st. The money is on its way, it’s just delayed. One measure of institutional interest in digital assets can therefore be seen by looking at the returns in the first 10-days of each month this year (using the largest tokens from each sector as a proxy). It’s entirely possible that the selling pressure at the end of May will subside quickly as the calendar turns.

.png?width=800&name=image%20(33).png)

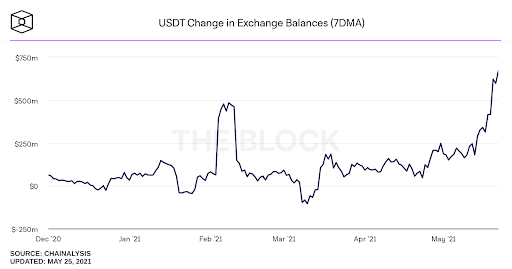

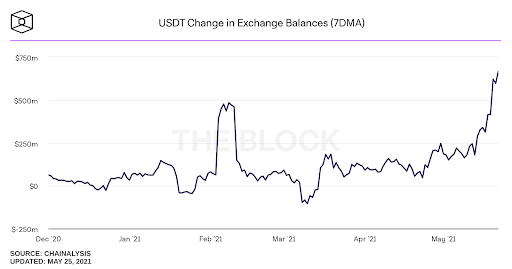

Second, the low rate, low dollar macro environment is leading to a glut of cash. Reverse repo operations saw $433 billion last week, the third highest daily volume ever. Reverse repos are used by institutions with excess cash, and are particularly relevant given the lack of low risk yield opportunities. Meanwhile, total money market fund assets increased by $67.73 billion to $4.61 trillion for the week. And of course, record amounts of US dollar stablecoins are parked on exchanges right now, with virtually no use case other than to buy digital assets when the water is calm.

Source: Chainalysis

Source: Chainalysis

Source: Fundstrat

All of this money has to go somewhere, and both digital assets and equities are expected to run hot for the foreseeable future. It just might not be led by Bitcoin.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

To learn more or talk to us about investing in digital assets and cryptocurrency