What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?

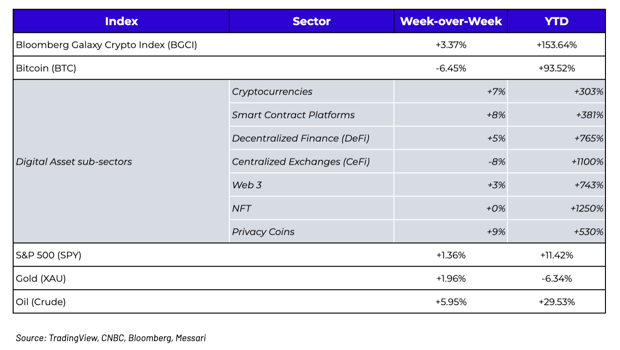

Week-over-Week Price Changes (as of Sunday, 4/18/21)

Wait, DogeCoin Drove The Market Higher?

Before we get to one of the craziest and swiftest weekend selloffs on record, we have to talk about cryptocurrencies. Contrary to popular belief, currencies are just one of many sub-sectors in the digital assets market, but it just so happens to be the largest and most well known due solely to Bitcoin’s inclusion in this sub-sector. Most of the other legacy currencies from 2017 (XRP, XLM, BCH, BSV, LTC) have not found anywhere near the audience Bitcoin has, or anywhere close to the traction DeFi, Web 3 and other sub-sectors have. Yet these assets continue to boast large market caps due simply to their growth and popularity amidst traders long before other digital assets existed, and before anyone knew or understood how to value digital assets. Normally, as Bitcoin goes, so do the other currencies, but last week was a bit of an anomaly. The Currency sub-sector gained +7% week-over-week, while Bitcoin itself was -6%.

Dogecoin (DOGE) drove these gains, with a staggering +374% week-over-week move, rising to a $43 billion market cap. And many other currencies followed suit in what can only be described as a knee-jerk reaction to the gains in DOGE. A trader likely logged into Robinhood (where DOGE trades), saw huge outsized gains in DOGE, and immediately snap bought the only other tokens from the limited pool of assets available on the Robinhood app -- causing large gains in LTC, BSV, BCH and ETC as well. And just like that, you have a Bitcoin-less rally, while the efficient market hypothesis gets thrown out the window because different buyer bases have different access to different tokens depending on which venue they trade.

.png?width=560&name=unnamed%20(97).png)

Source: Messari

So What the Hell is Dogecoin?

Honestly, I have no idea. It’s now the 6th largest digital asset by market cap, even though it started off as a purposeful joke (really, read the history) and there doesn’t seem to be a single reason to own or use DOGE. That said, at this point, I’ve learned to be open-minded about EVERYTHING rather than laugh and dismiss. Unlike pass-thru tokens and asset-backed tokens, which actually accrue real economic value to token holders via revenues and utility, cryptocurrencies (including Bitcoin) exist solely to protect purchasing power and to transact in a fast, cheap and trustless manner without a financial intermediary (like a bank or brokerage). And even though Bitcoin has hundreds of other traits that are superior to DOGE and every other cryptocurrency (security, developers, history via longest chain, infrastructure, brand, wallet dispersion, decentralization, etc), at their core, they are still simply belief systems -- so if a handful of crazy people want to will DOGE into the mainstream, who are we to stop them? With exceptionally high interest on social media, spurred somewhat by Elon Musk’s regular and mysterious DOGE tweets, DOGE has become the 2nd most popular cryptocurrency on Twitter, accounting for 23.2% of total crypto tweets.

.png?width=562&name=unnamed%20(98).png)

Source: Coinbase / The Tie

So will DOGE actually succeed? There is almost no chance that it does. But, for all you math majors out there, one minus almost no chance equals some small chance. And the market is telling you what that chance is. The total market cap of all tokens in the cryptocurrency sub-asset class is $1.25 trillion, of which Bitcoin makes up $1.07 trillion (or 86%). Dogecoin is $43 billion, representing 3.4% of the total digital currency market cap. So the market is basically pricing in DOGE’s odds of succeeding at 3.4% (with XRP, LTC, XLM, BCH, etc priced with slightly greater than 10% chance, combined). Now, those odds seem way too high to anyone who studies blockchain usage, but again, this market has taught us not to bet against underdogs. One can look at Gamestop (GME) for proof that social investing is often more powerful than fundamentals. Essentially, these other cryptocurrencies are perpetual call options with infinite time to expiration, a 0 risk-free rate, and high volatility… which makes them attractive long-tail options.

Black-Scholes Model and Crypto Optionality

(written by Arca Trader Mike Geraci)

The Black-Scholes model requires five input variables:

- the strike price of an option

- the current security price

- the time to expiration

- the risk-free rate

- and the volatility

Cryptocurrencies can thus be compared to owning cheap call options with no time decay and high volatility. Time value is the key metric in an option’s value. For example, as Bitcoin is currently trading at $57K, the BTC May 28th 2021 $80k strike calls are trading at $1400, while the BTC June 25th 2021 $80k strike calls are trading at $3100. Why would any investor be willing to pay such a premium for the option to buy BTC at $80k if the intrinsic value of the option is worthless? The entire value of the $80k call comes from its time value; the market’s perception of how much the asymmetric proposition of being able to buy BTC at 80k at a time far in the future might be worth given the underlying volatility of BTC. The more volatile BTC is, the more likely extreme outcomes become. Further, when volatility is going up, this implies the market is willing to pay more for options because they are expecting a greater range of potential price outcomes.

Perhaps more importantly, there is an inherent difference in the capital structure of a cryptocurrency versus a publicly traded equity. A company’s enterprise value is the aggregate value of its outstanding debt, equity and cash. But as soon as a company has a cash crunch, the time value starts to decay and the clock starts ticking. A company only has so much time to tread water before the value of its stock depreciates and bond principal payments and interest come due, potentially leading to default and bankruptcy. Time works against traditional companies. Cryptocurrencies, on the other hand, are vastly different. The underlying blockchain technology is typically open source, transparent code carried out by a decentralized network with a potentially limitless number of miners and developers that further a cryptocurrency’s chain. Cryptocurrencies don’t carry such enormous debts and operating expenses as do traditional companies. Therefore cryptocurrencies don’t suffer the same consequences of bankruptcy or being dissolved if the expansion of their chain or even the application of the coin’s core mission doesn’t get expressed in a timely manner. These factors make owning spot cryptocurrencies similar to owning a cheap call option with an infinite time to expiration.

There is a very beneficial aspect of a self-fulfilling prophecy in the cheap option theory. As a coin is in its infant stages of growth and evolution, it doesn’t have to be burdened with the same restrictions of survival that constrict most public companies. A cryptocurrency has the freedom to grow and adapt to the market in an unbridled manner.

You can apply this same methodology to other sub-sectors as well. For example, in the smart contract protocol race, Ethereum is by far the most active and most well known protocol as measured by active addresses, transaction fees, TVL, dAPPs and any other metric you choose to use to evaluate. The total market cap of all smart contract protocols is $445 billion, of which Ethereum represents $260 billion (or 58%). The other 42%, which is made up of tens if not hundreds of competitors (Cardano, Tezos, Solana, Binance Smart Chain, etc), are all call options on future success.

Active Wallet Addresses of Select Smart Contract Platforms

.png?width=592&name=unnamed%20(99).png)

Source: CoinMetrics

Again, this doesn’t mean any of these protocol tokens warrant the prices that they are trading at -- startups with little to no traction carrying multiple-billion dollar market caps may seem absurd. But you also cannot fully dismiss these values simply because they will never die, and the upside of being part of a revolution that upends the financial system is so enormous. Time and volatility are worth something, and in digital assets, the market is telling you that it is worth a lot even if intuitively it makes little sense.

Speaking of option value, even Bitcoin itself can be thought of as one giant trillion-dollar option. Our friend Greg Foss recently came up with an actual price for Bitcoin based solely on its option value, viewing Bitcoin as an insurance policy against the collapse of all other fiat currencies. Using similar methodologies to that of the Credit Default Swap (CDS) market, you can come up with an actual value for what that option is worth.

So Why Did the Market Crash 20% Over the Weekend?

Oh yeah -- we should probably address this. Well, for starters, when hundreds of billions of dollars are being thrown at these high-priced, but still potentially cheap options, it can lead to a LOT of excess speculation. It’s one thing for you to buy insurance on your house, it’s quite another for millions of people to buy insurance on your house.

.png?width=512&name=unnamed%20(100).png)

And this rampant speculation leads to leverage, and leverage always leads to washouts. A series of incorrect, unsubstantiated, and misleading tweets led to one of the largest selloffs and highest futures liquidations ever recorded. During a 24-hour period, there were over $10 billion in futures liquidations (a new record) before the market found its footing and recovered.

It was a bloodbath, and yet, it also ended very quickly with most digital assets still finishing the week higher (and in some cases much higher).

Systemic Risk Versus Price Risk

Naturally, the volatility over the weekend will have most investors and the media questioning the volatility of digital assets. But this is what happens in free markets where volatility isn’t artificially suppressed by the governments and central banks around the world. Which begs the question, which is better?

Would you rather have constant price risk with massive, frequent drawdowns and a few players getting periodically wiped out, but where the overall marketplace and infrastructure work fine without any interference? Or would you rather have no price risk but periodic systemic malfunctions leading to huge blow-ups (Archegos, Credit Suisse, Nomura, Melvin Capital, LTCM, Lehman, Bear, MF Global, commercial real estate, etc)?

I, for one, prefer price risk, because you can plan for that and manage outcomes. If a bunch of traders want to aggressively ape into assets like DOGE, or use 100-to-1 leverage gambling on BTC, that’s fine -- we can see these transparent metrics on-chain and make decisions based on the expected outcomes. It can lead to excessive risk taking which ultimately gets washed out (like Saturday night), but it also probably prevents the seemingly once per year storms that we see far too frequently in the debt and equity markets. Those that were liquidated suffered large losses, while everyone else still marched along with week-over-week gains in their portfolios.

And oh by the way, outside of “Cryptocurrencies”, many real companies in the digital assets space continue to do amazing things with the use of digital assets, that have nothing to do with money, or sharp moves up or down in price...

Entering the Ring - Fan Tokens

(written by Arca Head of Research, Katie Talati)

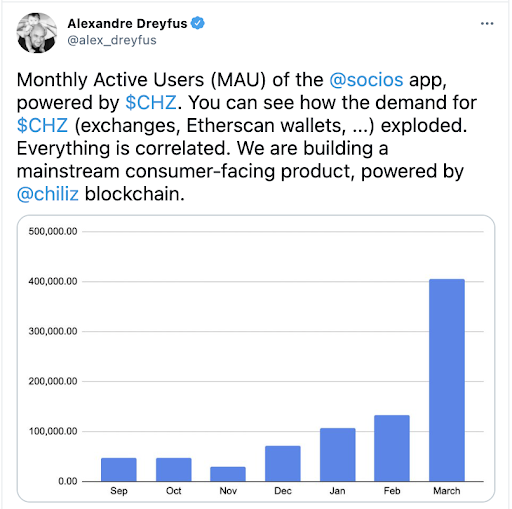

While everyone in crypto was marveling at how a meme-coin like DOGE pushed its way into the top 10, projects with real traction and usage flew under everyone’s radar. One of these projects, Chiliz, has continued to build its business adding real users and real partnerships, such as last week’s overlooked announcement of Chiliz’s partnership with Rakuten, which will now offer its European users (part of its 1.4 billion worldwide user base) the ability to use their rewards to buy fan tokens.

Chiliz is a platform and exchange that issues Fan Tokens tied to real-world sports teams and leagues that offers the holders special perks such as voting power over team decisions, and Socios is the mobile app where users can interact with Fan Tokens and participate in votes, competitions and fan discussions. To date, Chiliz has partnered with 25 sport teams and leagues including FC Barca, Manchester City, Juventus, and the UFC. Underpinning it all is the CHZ token, which users must use to purchase Fan Tokens and which Chiliz burns based on its revenues.

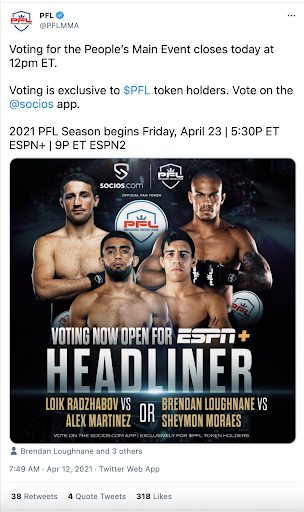

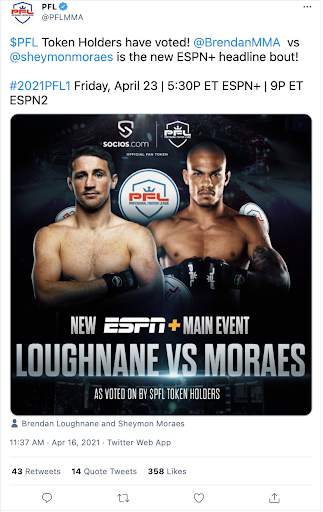

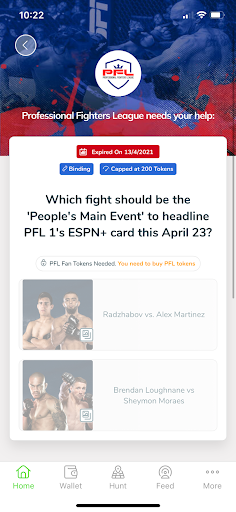

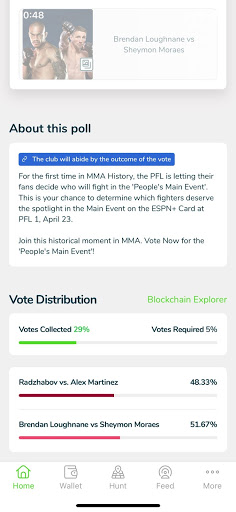

One of Chiliz’s latest Fan Tokens is PFL, representing the Professional Fighters League, an American MMA league. Last month, Chiliz held a Fan Token Offering (FTO) for PFL, which sold out in under 10 mins and raised $500,000. Following the sale and secondary listing of PFL, a vote was held on Socios to determine which fighters would compete in a match this upcoming Friday on ESPN+, marking the first time in MMA history that the PFL is letting its fans decide who will fight. The outcome of the vote matters less than the fact that 29% of token holders participated in the vote, representing 1,684 users. This number might sound like a one-off stroke of luck, but across Chiliz’s 18 launched fan tokens over the last 12 months, votes on the Socios app on average saw 21% participation rates. Not only is that showing a massively engaged user base, but it also demonstrates the power that tokenization is giving to fans. For years, fanbases have been the driving force behind sport teams, musicians, actors and other celebrities, generating revenue and success for these groups and now they finally have the ability to decide on outcomes for communities that they’ve long been a part of.

Source: Twitter / @alex_dreyfus

Beyond that, Chiliz is creating a model for governance that actually works and has staying power. Defi communities have consistently struggled to get token holders to participate in governance with many claiming decentralized governance won’t work at all. Chiliz just destroyed all those assumptions and showed that governance tokens work when there is something actually worth governing.

Source: Socios App

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodard- Analyst

Mike Geraci- Trader

To learn more or talk to us about investing in digital assets and cryptocurrency