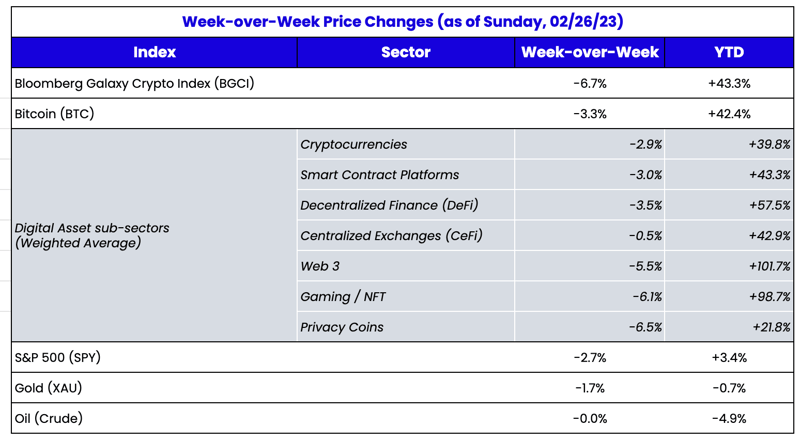

Digital Assets dipped but continue to outperform equities in February

After one of the strongest January’s on record for just about every asset class, the equity and fixed income markets turned on a dime in early February following the FOMC meeting, subsequent press conference, and the

much better than expected payroll report. Much of the January gains have been erased. The S&P 500 has now fallen for three straight weeks, and the 10 year U.S. Treasury yield has risen 55 basis points since the first few days of February. Digital asset prices meanwhile have slowed from their January pace, but are mostly unchanged month-to-date. Last week was no exception, as digital assets fell at a relatively muted pace even as U.S. equities fell sharply.

As our friends at Cumberland pointed out in a weekly note to clients, the price action thus far seems quite different than that of 2022, whereby one of the most successful strategies was “reversion to the mean.”

“The best performers would always mean-revert, and a strategy of selling outperformers and buying underperformers did extremely well. That does not seem to be the case so far this year. As an example, Optimism (OP) was among the best performers in January, up 140% in that month. In February, it was the best performer in the L1/L2 space, adding another 35%. Similarly, in the DeFi space, Lido (LDO) was January’s top performer (+120% in January) and it was February’s top performer as well, adding another 50%. I can’t recall any coin which led its sector in back-to-back months this way during 2022. Both LDO and OP have performed on the back of extremely strong narrative themes. In the case of LDO, the entire liquid staking derivatives sector has rallied ahead of the Shanghai upgrade expected at the end of this month. In the case of OP, the narrative of L2s expanding their use case via partnership has been in full effect since Polygon won Q4. The entire narrative of the past week has revolved around Coinbase’s Base L2, which will not only be built on the Optimism stack, but will also tie deeply into other apps on the Optimism chain.”

Coinbase, Layers 2s (L2), and Valuation

Written by: Nick Hotz, CFA and Robert Valdes-Rodriguez, CFA - Vice Presidents, Research

Coinbase is still the 800 pound gorilla when it comes to digital assets, especially in the United States,

delivering better-than-expected Q4 results last week. Total revenue came in ahead of

street expectations driven by a rise in interest income partially offset by lower trading revenue. Adjusted EBITDA also outperformed in the quarter primarily due to recent cost cutting initiatives. The company saw an elevated number of institutional customers onboarding onto Coinbase Prime in the quarter. While Coinbase did not provide much color on this institutional group, they

did mention on the analyst call that

“companies who had been potentially self-custodying, and holding assets at less transparent platforms really brought their assets to Coinbase in the fourth quarter and look to onboard.” We view this as another example of Coinbase picking up market share in the aftermath of recent industry carnage.

Looking into 2023, the company mentioned a strong start to the year with $120M of transaction revenue in January, though we wouldn’t be surprised to see a deceleration in February based on

February volumes. Additionally, Coinbase is now targeting positive adjusted EBITDA in all market conditions versus the prior plan to run at breakeven across market cycles, which in theory should have been well-received by investors.

In theory, anyway. But Coinbase stock is not well loved by Wall Street. The COIN stock has a steadily rising 25% short interest, its BB-rated bonds are trading at CCC-rated yields (north of 12%), and Wall Street analysts are extremely bearish on the market leader of one of 2021’s hottest industries. COIN fell -11% last week even after the earnings beat.

So it’s not entirely surprising that equity analysts completely ignored the massive news that came 24 hours after earnings…

Source: Bloomberg

… the Base Announcement

Coinbase shocked the digital asset ecosystem last week when they announced a new Ethereum Layer 2 chain, called Base. Built in partnership with another L2, Optimism, Base’s rollup is no half-hearted foist into Web 3. Rollups are seen by many as the gold standard for security and Optimism is one of the longest-standing efforts to scale Ethereum. In

Coinbase’s own words:

“Base – a secure, low-cost, developer-friendly Ethereum L2 designed to help scale the web3 crypto-economy. Base is being built on the OP Stack in collaboration with Optimism, has no token, leveraging ETH as the native asset for gas. The overarching goal of Base is to be a development hub for Coinbase’s on-chain products and foster an open crypto ecosystem for third party wallets, dapps, and developers. By creating a trustworthy and easy-to-use L2 environment, Base aims to accelerate the development of dapps with real utility. Coinbase is targeting a mainnet launch of the Base network in 2Q23.”

While equity analysts may not know what to make of this news, there are clear winners, including Coinbase itself.

Winners:

Optimism (OP): +13% last week

The Base announcement demonstrates that Optimism is not just a single rollup, but rather an entire ecosystem of Layer 2’s that will eventually share a collective network effect. This is a very real, deep partnership with Coinbase, who is becoming the second core developer on Optimism’s OPStack. Optimism will also receive a portion of revenue derived from operating Base.

It is important to understand that Optimism and Coinbase are working on building a joint “sequencer,” the computer or network of computers that orders transactions within the blockchain. Applications built on blockchains that share a sequencer have seamless composability in the same way that applications within one chain do. For example, traders on Uniswap’s deployment on Base would be able to access liquidity both from Base and from Optimism, significantly improving UX. Optimism is calling this idea the “Superchain,” and making it a reality by adding a top-tier partner like Coinbase.

Coinbase Users

In their first day media tour, Coinbase noted it would incentivize users to try out Base by potentially paying them to move assets. Optimism also said it would incentivize adoption of Base possibly with OP token grants to applications.

Base also improves on many rollup designs by implementing Account Abstraction, a new technology that doesn’t exist in Ethereum currently that allows for much greater flexibility around how accounts interact with the blockchain. Despite ETH being the native token of Base, Coinbase could, for example, allow users to pay fees in USDC, which would then be converted back into ETH by the chain. The implementation of Account Abstraction can improve the blockchain onboarding and user experience dramatically, making it much easier for new users to get started.

Coinbase Shareholders (COIN): -11% last week

While Coinbase and Optimism eventually plan to move to a shared sequencer model, for the time being, Coinbase will earn transaction fees for running the Base chain. This can actually add up to be a significant source of earnings.

Optimism did $20M in annualized fees in January from running the sequencer for its rollup with only 45k daily active users. Meanwhile, Coinbase has 108M users to draw on, will heavily incentivize Base usage, and has immediate buy-in from the whole suite of blue chip projects. To be clear, most of the fees are currently paid back to Ethereum for security, but this will change after

proto-danksharding is implemented this summer.

Coinbase also has lock-in for most of its users who are not crypto-native and likely will be onboarded only via Coinbase’s own wallet. These users can be monetized in ways crypto-natives cannot, for example, via in-wallet transaction fees, extra fees in a Coinbase native decentralized exchange, or with advertising spend/pay for order flow.

Ethereum (ETH): -4% last week

The installation of Base as a Layer 2 on Ethereum provides further validation of Ethereum as a settlement layer and

ETH as a currency. Coinbase said it has no plans to issue a token and will use ETH for gas fees.

Source: Twitter

Coinbase has previously expressed interest in directly interfacing with crypto applications.

“The Coinbase Secret Master Plan” laid out its plan to eventually move into the decentralized interface/app space way back in 2016. The barrier has always been ensuring top-notch user experience and security, which they finally addressed as an Ethereum rollup built using Optimism’s tools.

Source: Coinbase

Source: Coinbase

Coinbase has also worked with Optimism to propose and test EIP-4844, proto-danksharding, which will dramatically reduce costs for users and operators of Ethereum rollups. Prior to their involvement, proto-danksharding was expected sometime in 2024, but with their efforts it has been moved up to summer of this year.

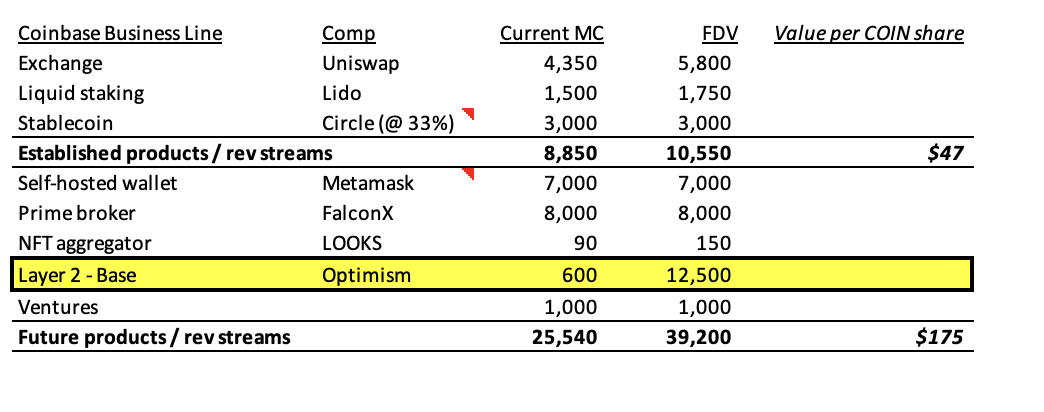

So what does this mean for one of Wall Street’s most hated stocks? A Sum-of-the-Parts Analysis

As

Noelle Acheson wrote,

“This makes Coinbase the *first listed company* to launch a blockchain. Equity analysts will be scrambling to understand zk-rollups, bridges and more, which should deepen Wall Street interest in and familiarity with the on-chain world.”

Coinbase has an Enterprise Value of less than $13B, or roughly 4x EV/Sales. Most of Wall Street treats this as a monolithic company with a high fee exchange business, and gives Coinbase virtually no credit for the other business lines that it has incubated or acquired. It’s a fun thought experiment to look at a sum-of-the-parts analysis of Coinbase, using industry comps in each vertical. While we don’t expect equity analysts to give Coinbase the benefit of the doubt anytime soon, the addition of Base, in theory, adds a lot of value to an already undervalued stock.

Source: Arca internal calculations

Source: TradingView, CNBC, Bloomberg, Messari

Source: TradingView, CNBC, Bloomberg, Messari