Source: TradingView, CNBC, Bloomberg, Messari

An FOMC Rally

Towards the end of August, we talked about the green shoots we were seeing in the market and how it was

inevitable that crypto would catch up to the persistent rally in Gold, Treasuries, and global equities. Instead, crypto tanked -20% over the following week. Many, including ourselves, were thrown aback by the late August / early September price action. But the FOMC came to the rescue. While the world debated 25 bps vs 50 bps, ultimately, it did not matter. The play was long either way. The rate cuts have finally begun, and Powell was firm in his press conference that the Fed wanted to be ahead of the curve instead of behind.

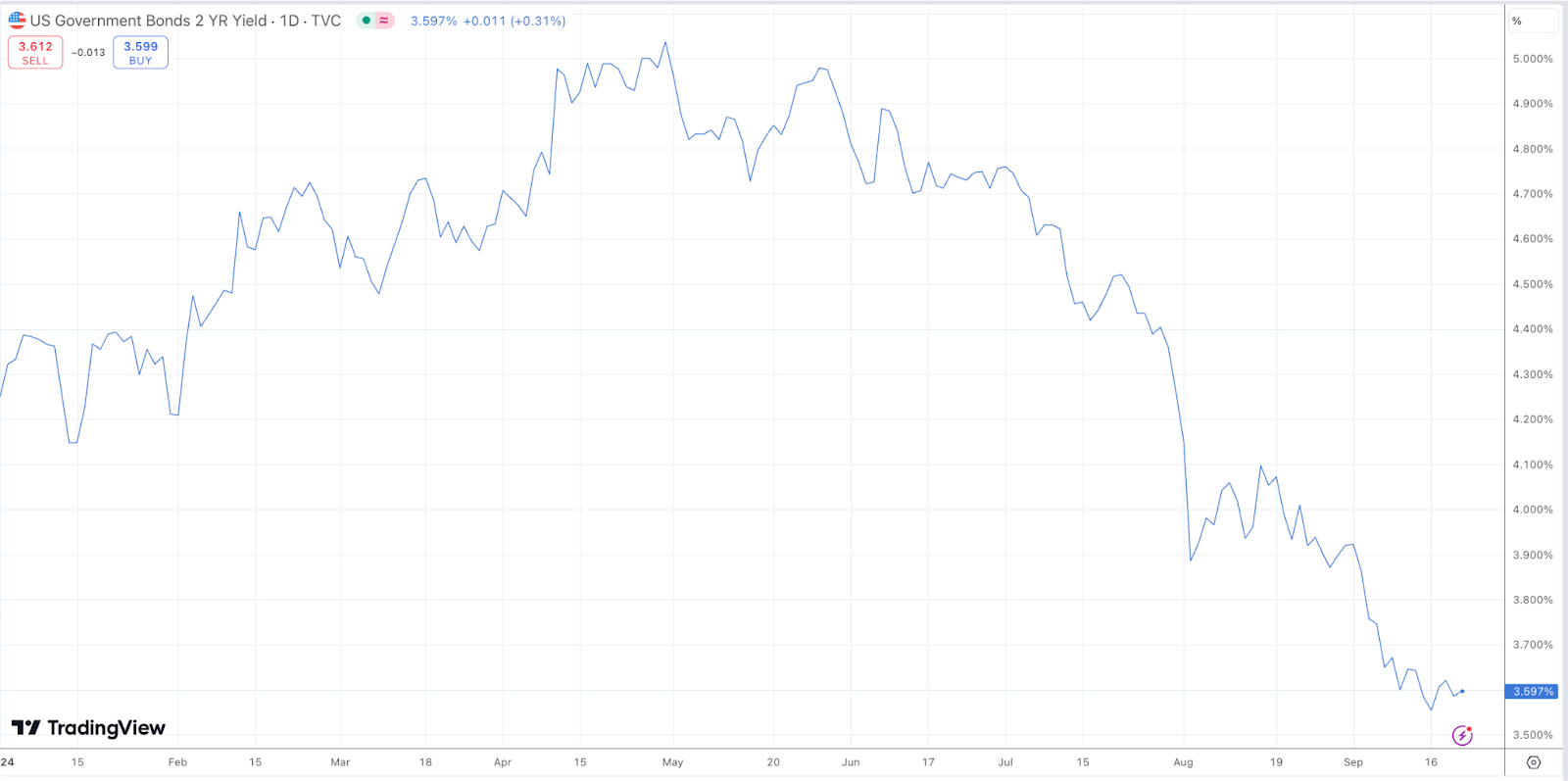

Treasury yields have anticipated this cut for a few months. The 2-year Treasury yield has fallen by over 150 basis points since May.

Source: TradingView

While Treasuries, gold, and equities simply needed confirmation of what they already knew, crypto needed an actual catalyst. And while it’s not the most exciting reason for digital assets to rally, it was the spark the market needed.

But interestingly, in a year led by Bitcoin, Solana, and a handful of memecoins and newly issued tokens, the market took the Fed’s cue to buy beaten-up “altcoins”. Now, I hate the term “altcoins” because it fails to differentiate between sectors, themes, and individual tokens adequately. But alas, this past week it is probably an accurate description of last week’s rally. There really was no theme, sector, or rationale for the sharp moves higher in many non-major tokens. If it was beaten up, it was probably higher last week.

Given the many head fakes we’ve seen this year, it’s natural to question whether or not this rally has legs or not. So, let’s look at some of the factors that should help determine the answer:

Macro - Extremely Bullish

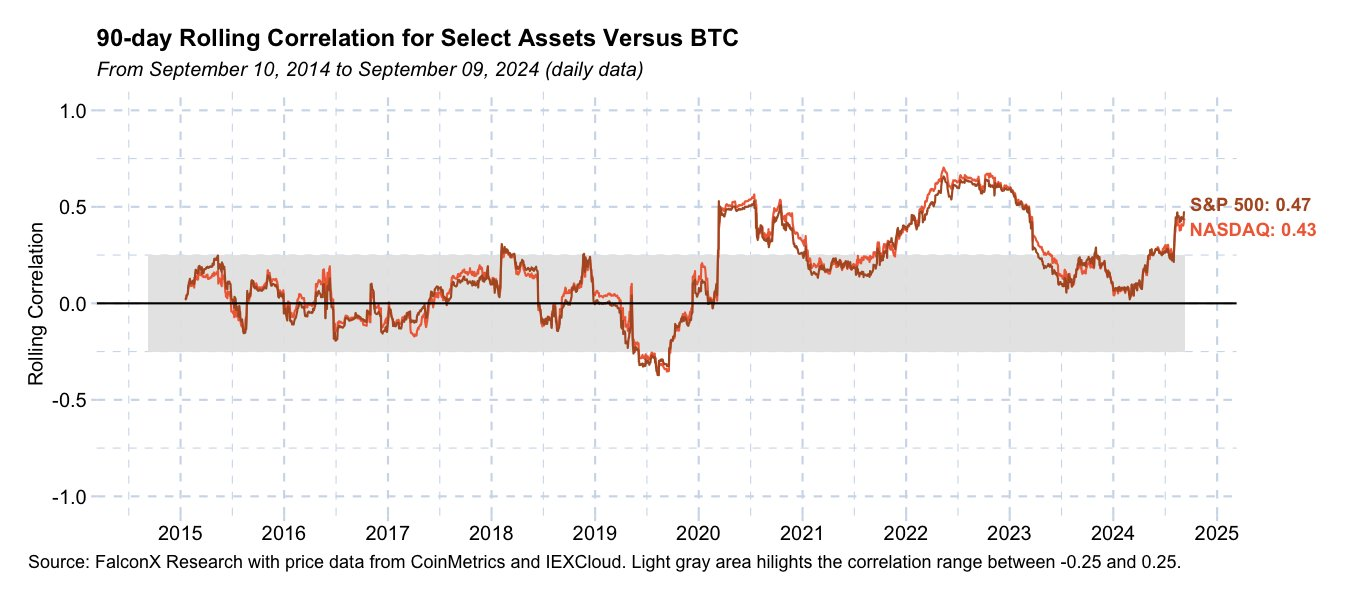

The correlation between digital assets and equities is at a 2-year high, so there is no doubt that macro is driving the bus right now.

Source: FalconX

And it’s a pretty clean sweep of positive macro factors currently.

- The VIX has once again fallen back into the mid-teens after a few upward scares

- Equities and gold are at all-time highs

- Treasury yields are once again falling, with the 10-year now comfortably below 4%

- The U.S. Dollar continues to trend lower

- Corporate credit spreads are back close to the tights

- Geopolitical risk is fairly muted, relatively

- The Fed left no doubt in the market’s mind that it was going to cut rates to stay ahead of a recession aggressively.

All of these factors are pretty bullish, without much doubt. Obviously, the next few quarters will tell us whether or not the Fed really did execute a soft landing or not, but for now, it’s pretty clear sailing, at least, until the election. Of all of these factors, I believe the high crypto/equity correlation is probably the least bullish, as it means the digital assets industry doesn’t have a lot of crypto-specific catalysts at the moment.

Crypto-Specific: Mildly Bearish

While the macro paints a bullish picture, the crypto-specific factors are much harder to get excited about. On the positive side:

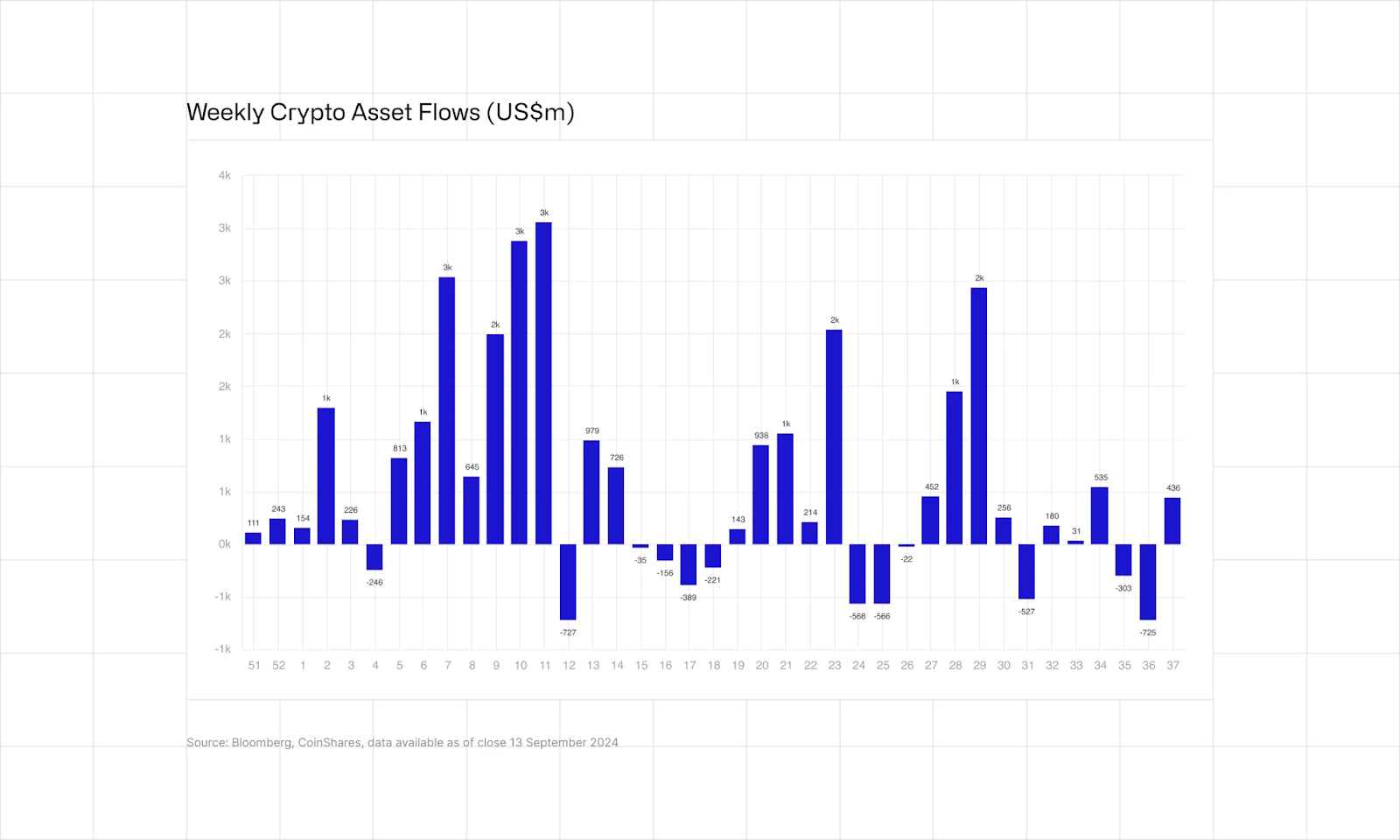

- ETF inflows have been a mixed bag. While they have been positive lately, they have ebbed and flowed and cannot be relied upon.

Source: Coinshares

- Supply overhangs from crypto bankruptcies like Mt. Gox and Celsius and selling pressure from the U.S. and German governments have largely dissipated. The lack of continued sell pressure can be considered a modest positive.

- Dispersion has increased. We’re starting to see a mini “alt rally”, led by a seemingly random collection of tokens. For example, in DeFi, Aave (AAVE) is now +37% MTD, but other DeFi tokens really haven’t followed suit. Bittensor (TAO) leads all AI coins, now +97% MTD. Sui (SUI) has become the layer 0, 1 or 2 VC token du jour, now +106% MTD. Immutable X (IMX) is really the only gaming token rallying, +37% MTD. Aerodrome Finance (AERO) is +65% MTD, as it is the only way to gain exposure to the rapid rise in activity on Base. Drift Protocol (DRIFT) is +58% MTD, partially due to Multicoin announcing an investment and partially because there is no way to invest in Polymarket, and Drift is the next best thing in prediction markets. The fact that there is some real separation between tokens is definitely a modest positive.

But that’s really where the crypto-specific positive factors end. The biggest problem with this rally is that there has been no real news other than the Fed.

- The Token 2049 conference in Singapore and the Solana Breakpoint conference failed to reveal any major initiatives. Given the high attendance, these takeaways from the event are about as mundane as possible. Arca’s own boots on the ground, Katie Talati, barely checked in with the mothership, because there was nothing newsworthy to report.

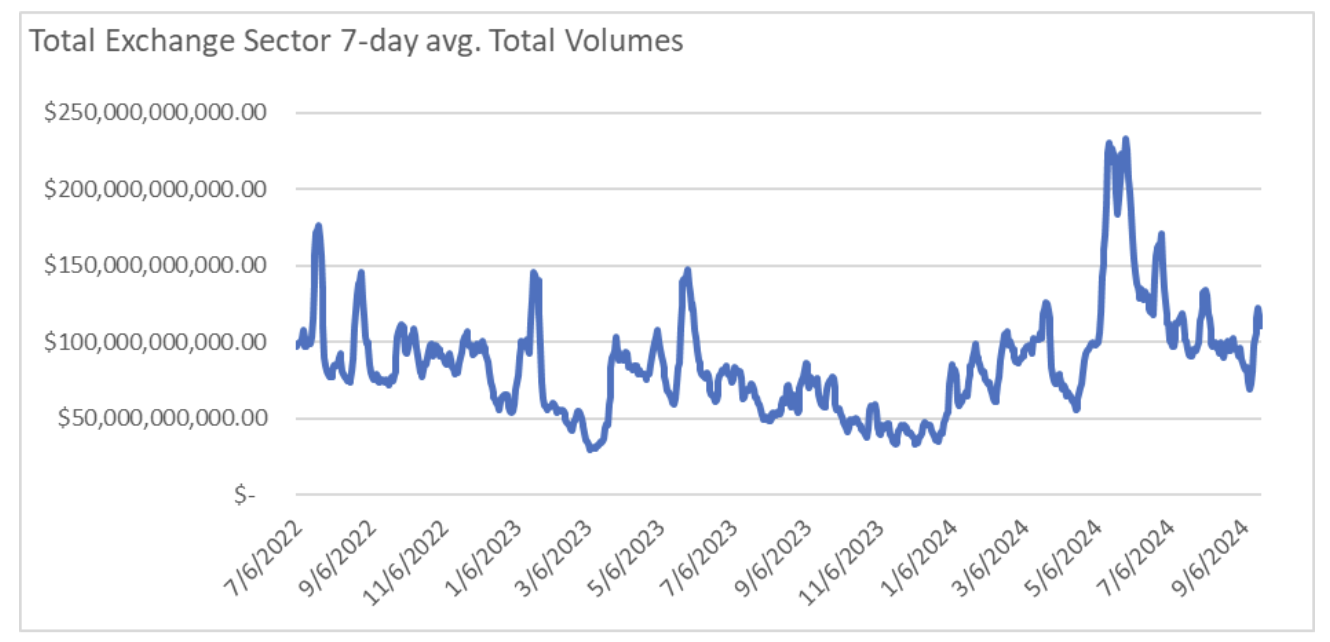

- Exchange volumes, while off the lows, remain nowhere close to the levels we normally see during more long-lasting, significant rallies.

![]() Source: Arca Internal Calculations

Source: Arca Internal Calculations

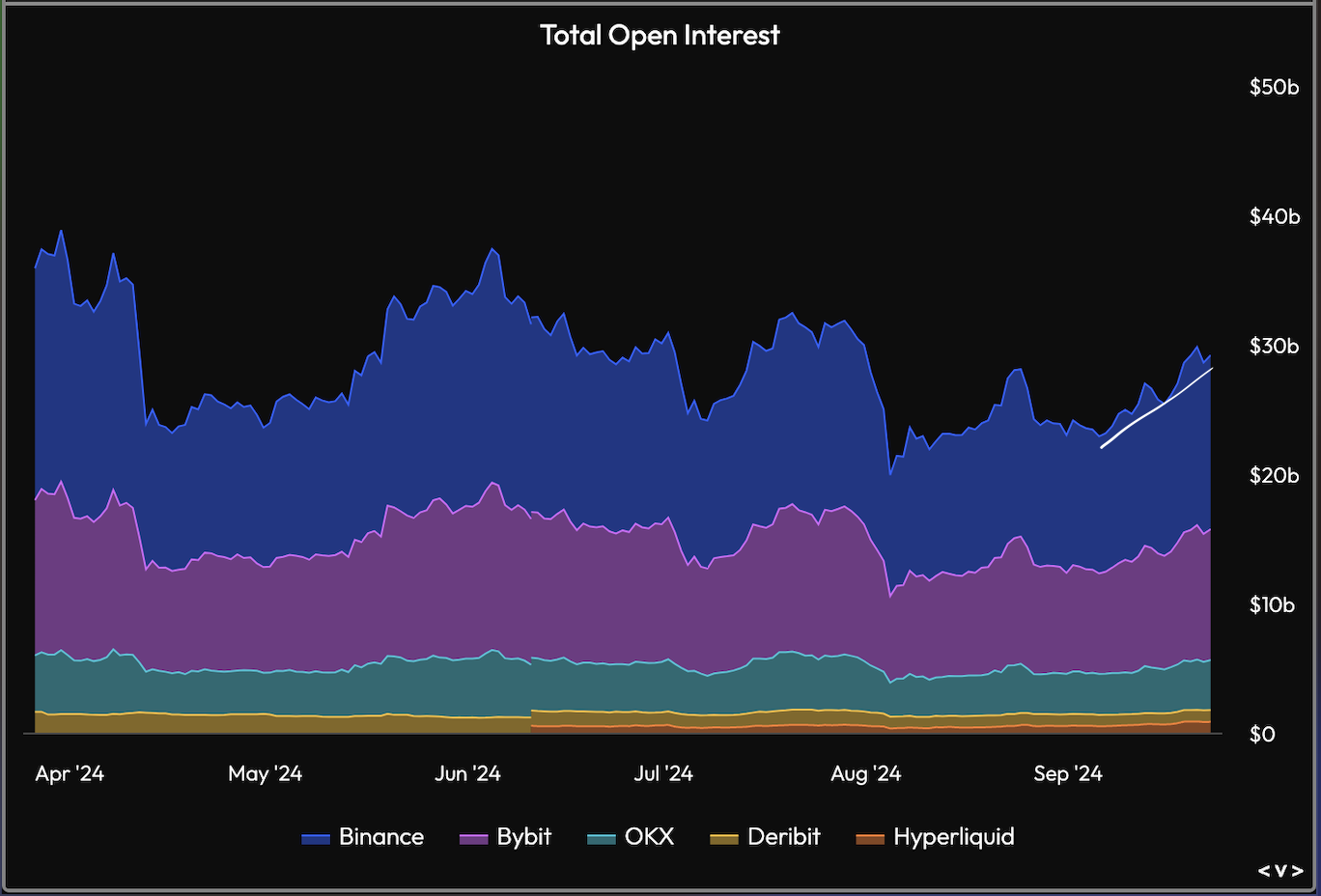

- And much of the buy interest has been futures-based rather than spot-based. This means there really isn’t new money entering the asset class. Instead, most of the buy pressure is speculation using leverage. Open interest in futures and funding rates are elevated.

Source: VeloData

While the market can certainly go a lot higher simply buoyed by relative underperformance versus other asset classes and a bullish macro background, we need to see some real money enter the system, coupled with some crypto-specific positive events. The election in November could be that spark, as so many good crypto ideas are currently non-starters due to regulatory pressure.