Source: TradingView, CNBC, Bloomberg, Messari

Stablecoins Are Back!

It wasn’t the most broad-based rally, but pockets of the digital assets ecosystem continue to gain, as a combination of new money entering the asset class and continued thematic rotations drove performance upward. Artificial Intelligence (AI) tokens remain one of the hottest sectors, as

we discussed last week. The growth continued this past week, including:

- Akash (AKT): Rose +73% following an upgrade to Mainnet 8, an upgrade that makes GPU deployments to the network simpler. Total GPUs on the network rose by 29 to 174, while capacity utilization increased sharply as fees rose to all-time highs.

- Bittensor (TAO):Gained +65%, as subnets 28-30 out of the max 32 registered this week, with one subnet focused on ZK proof generation and the other dedicated to training models to improve their coding ability. Staked TAO rose to 87.6%, its highest level.

- ImagineAI (IMGNAI): Gained +47% with the app crossing 10K users on the ImgnAI webapp- only 2 weeks after launch.

Source: TradingView

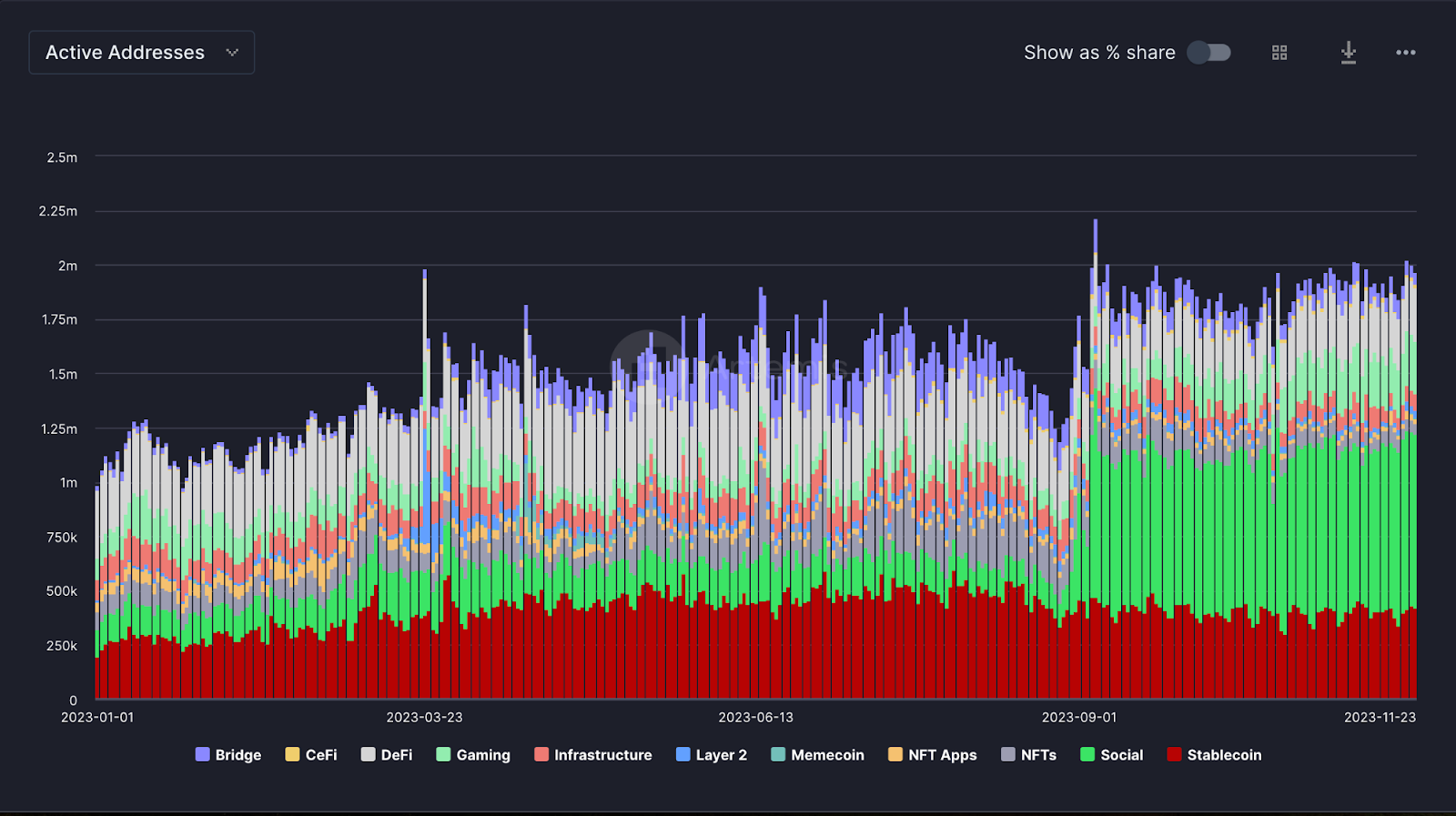

While the AI vertical is showing the fastest growth momentum, old stalwarts are driving the most blockchain economic activity. Social applications and stablecoins remain the largest contributors to market activity (the red and green in chart below).

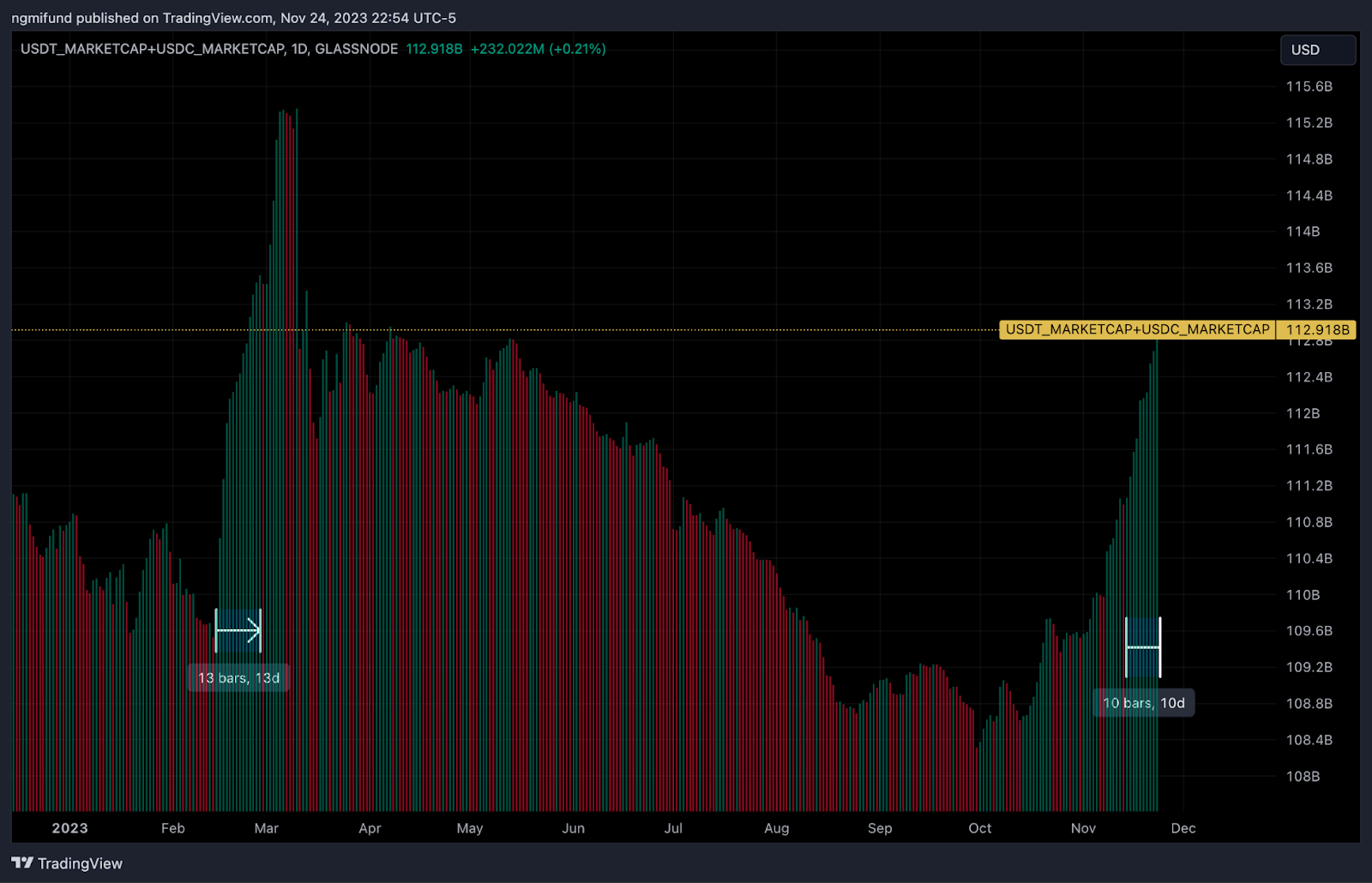

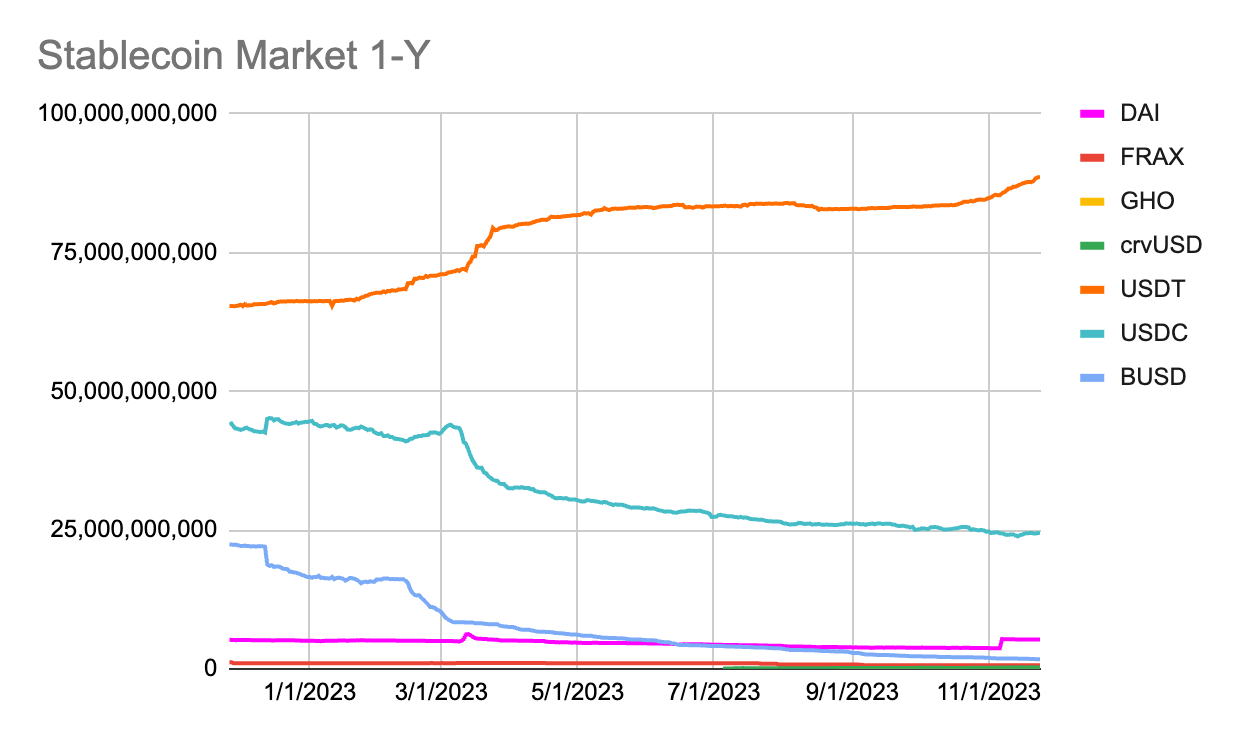

Overall stablecoin AUM increased 87 basis points week-over-week, with Tether (USDT) continuing to gain market share at the expense of USDC.

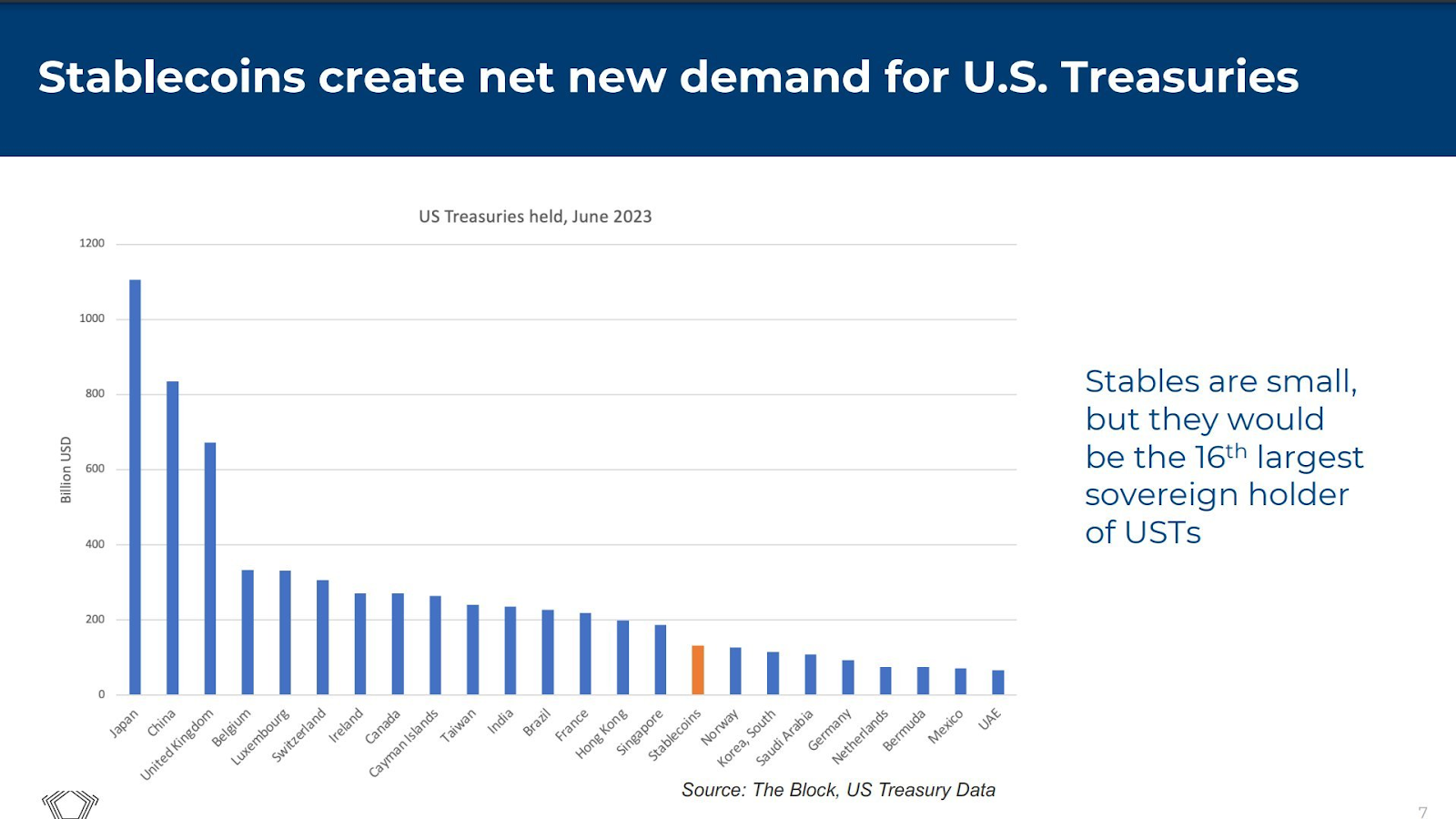

Ironically, amongst the United States government’s continued assault on the digital assets industry, stablecoins are now the

16th largest sovereign holder of global treasuries. Part of the fuel for Bitcoin’s growth specifically is due to unchecked government spending and perpetual budget deficits, and stablecoins are helping to facilitate the borrowing.

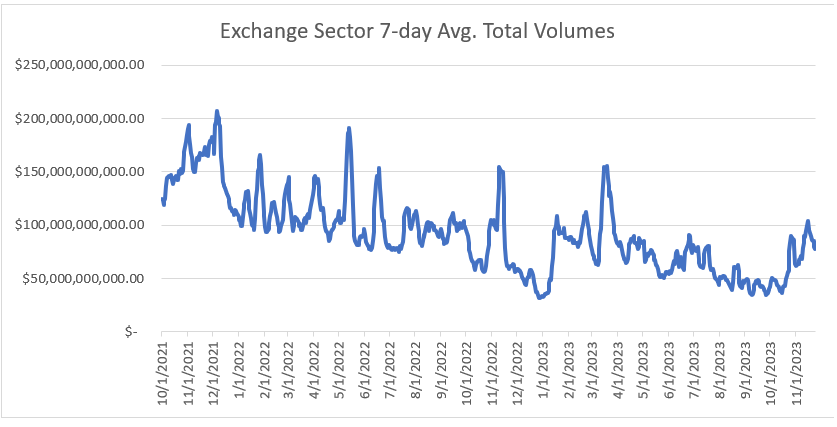

Meanwhile, exchange volumes were not higher last week, but the overall uptrend continues from the October lows.

Source: Coingecko, Token Terminal, Dune Analytics, Arca Internal Estimates

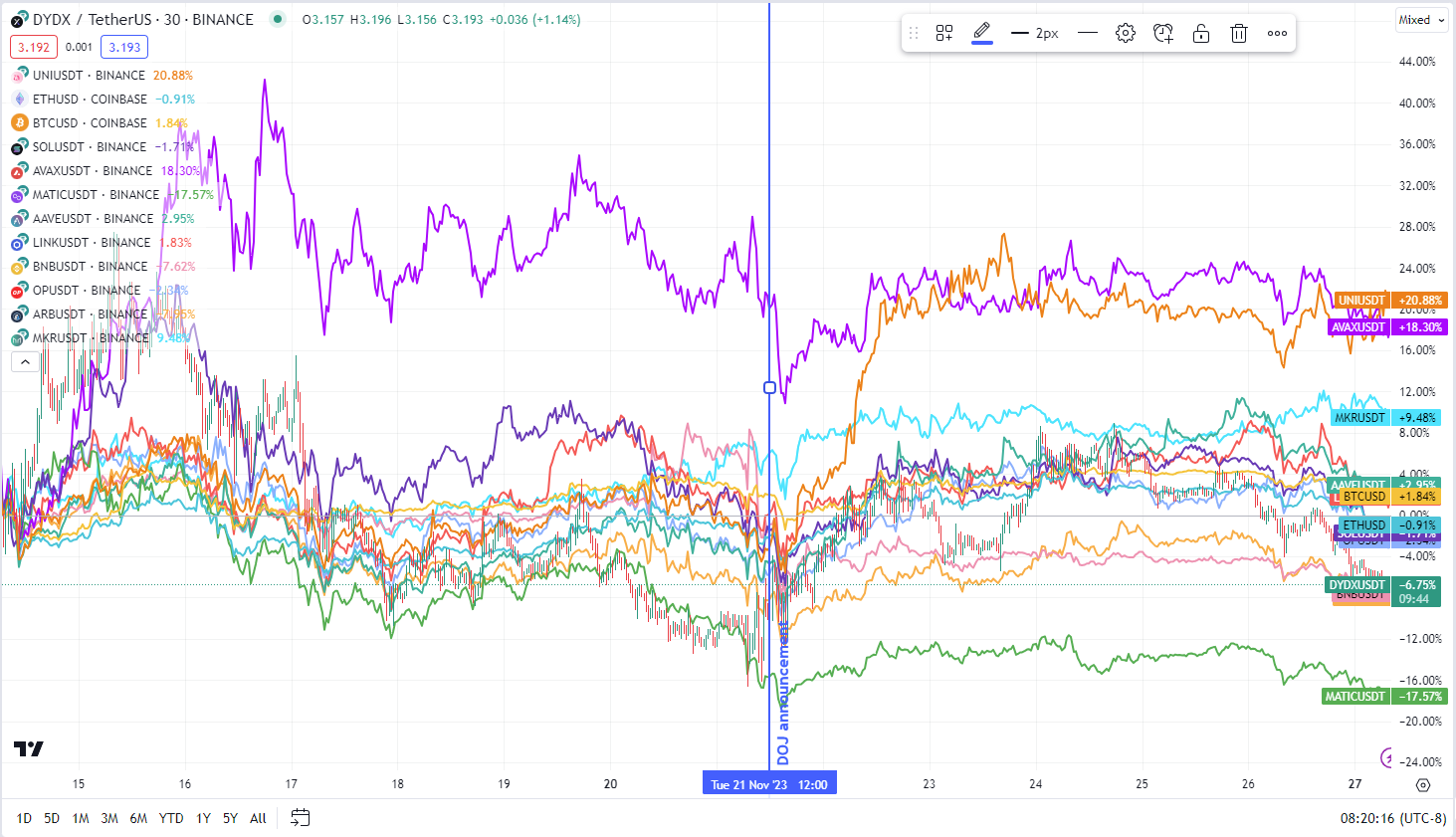

Perhaps more notably, the tokens of the two largest decentralized exchanges, Uniswap (UNI) as the leader in spot volumes and dYdX (DYDX) as the leader in derivative volumes, both rose meaningfully following the Binance/DOJ news, since both exchanges stand to benefit from further market share erosion at Binance.

Source: TradingView

Why the Binance/DOJ Risk Was Never A Real Market Risk

“Binance, the entity, pleaded guilty to felony charges for willfully violating the Bank Secrecy Act, knowingly failing to register as a money transmitting business, and willfully violating the International Emergency Economic Powers Act. Binance must pay $4.3 billion in fines as part of the settlement, review past transactions and report suspicious activity to federal authorities, and also provide Treasury access to its systems and records for five years as part of an ongoing monitoring regime. As part of the settlement, CZ also pleaded guilty to a felony charge for willfully violating the Bank Secrecy Act and stepped down as Binance’s CEO. CZ appeared in the United States District Court for the Western District of Washington on Tuesday to enter his plea. CZ will be replaced by Richard Teng, who previously oversaw Binance’s markets outside the US. Prior to that Teng served as Binance's CEO in Singapore and he also has prior experience working as a financial regulator in Abu Dhabi.”

This story developed for almost a year. Months ago, we discussed that this case may have been

tainted somewhat by the SBF trial, which could explain why it may have taken so long to conclude. Regardless, it's now over, and it removes a substantial regulatory market overhang. While U.S. regulation has long been a sticking point for many new digital assets investors, the Binance risk was, specifically, the most cited example over the past year. Much of this concern was (unnecessarily) elevated by a few crypto influencers and former fund managers who spent most of this year raising non-factual arguments over Binance’s imminent demise. That was never a risk. The most obvious outcome was always going to be a hefty fine and the removal of CZ.

There was never a basis for Binance to be shut down, nor was there a considerable risk of an FTX-style bank run. As

Nic Carter pointed out, Binance has been doing monthly attestations of client reserves for over a year—their wallets control

>$65 billion worth of funds. So, while we would never advocate that any investor leave assets on an exchange in any meaningful size, there was never any evidence that there was additional risk leaving assets on Binance versus any other exchange.

Further, it seems like I

write this every six months, but the Binance outcome ultimately never mattered in the first place for overall markets. In a global industry with perfect substitutes and low barriers to entry, price will never be impacted by government interference of one-off players. We’ve seen countless exchanges, quasi-banks, stablecoins, and other market leaders go out of business, and over and over and over again- only for customers to go to competitors. 2022 may have been an anomaly for market leaders to go out of business- not because they ran out of money, but because many were fraudulently stealing from their customers. That’s VERY different than what happened to Binance. While Binance is accused of many unlawful activities, there is no evidence that Binance customers have ever lost funds.

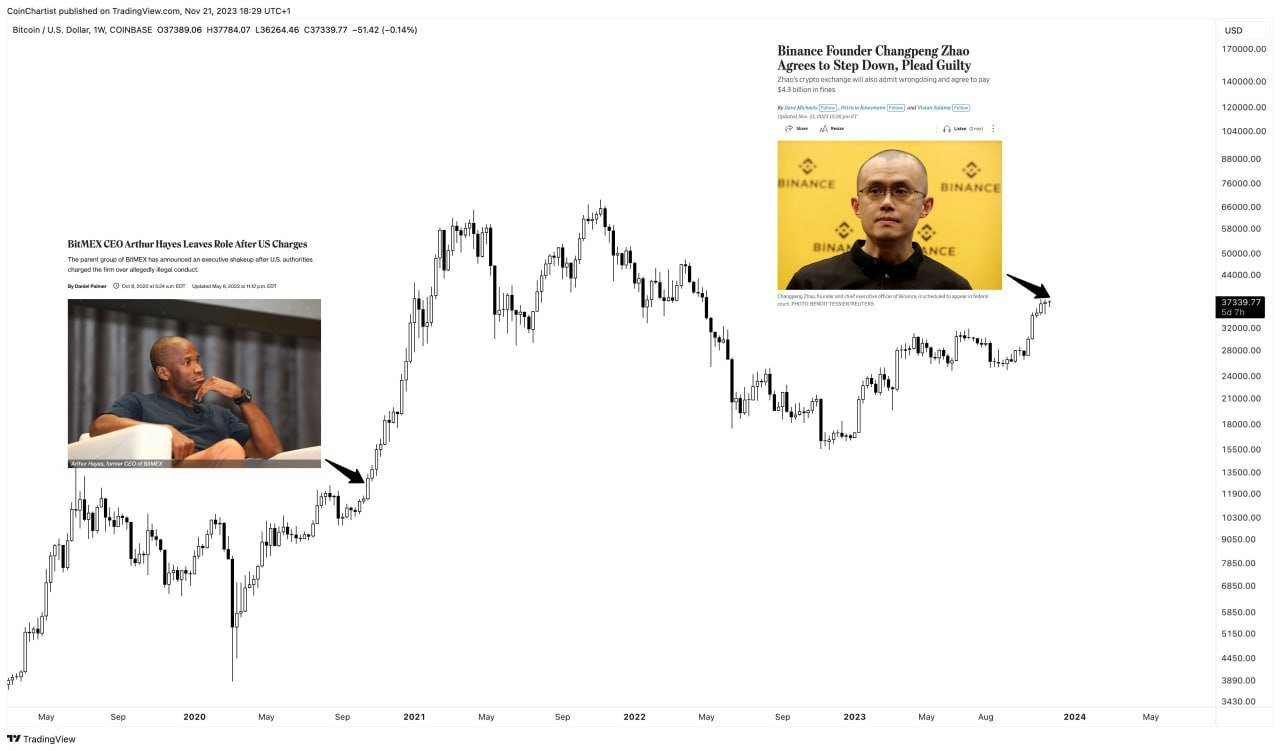

This situation also provides a precedent for how markets react to news of a big fine, a CEO removal, and reduced market share going forward. In 2020, Arthur Hayes, the founder and CEO of Bitmex, was indicted by the DOJ. Hayes was removed, and Bitmex lost market share, but the market itself

carried on with no regard to the changing of the guard. The most significant difference was that at the time of Bitmex’s demise, the U.S. was still a large customer base for Bitmex, so its removal from the U.S. cost Bitmex a lot of business. In contrast, with Binance, the U.S. (and

many other developed countries) have been shut out of Binance for years so that the go-forward Binance business will be largely unaffected. Binance will continue to serve non-U.S. markets, so there shouldn’t be much of a change in liquidity and, therefore, no market impact.

And finally, while this was the

7th largest single financial compliance fine in U.S. history, it’s not as if large financial fines for non-compliance are new to investors. If you thought a large fine would scare away investors, I have billions of J.P. Morgan and Wells Fargo clients on hold, ready to talk you off the ledge. For anyone keeping score, J.P. Morgan has paid over

$38 billion in fines over the past decade, 8x what Binance is on the hook for today, with the largest single J.P. Morgan fine was $13 billion in 2013. And I can’t even source all of Wells Fargo’s penalties because it takes up

multiple Google search pages.

The Binance outcome is the

best possible outcome anyone could not have imagined. Every settlement leads to a new, more compliant regime, and every naysayer is losing their arguments against digital assets. The “

government is going to kill crypto” ludicrous narrative is now gone forever. The U.S. itself is certainly not helping the industry grow, but they will not kill it.

Overall, this is a modest positive for crypto markets because it removes a major overhang. Interestingly, markets didn’t know what to make of this news initially, with a knee-jerk reaction lower before rallying back strongly towards the end of the week. We were more surprised by the initial sell-off than we were by the eventual rally.

Source: TradingView