Source: TradingView, CNBC, Bloomberg, Messari

The Path Forward Continues to Clear - Just Quietly Do Your Job

We’ll be spending a lot of time over the next few weeks reviewing 2023 and previewing 2024. But one thing is certain – the consensus opinion was dead wrong all year. The global economy did not fall into a recession. There were no rate cuts. And crypto is definitely not dead. Interestingly, most digital assets investors, journalists and market participants either focused on the natural or legal demise of 2022’s bad actors, or on the rapid growth in token prices in the 3rd and 4th quarters. But very few focused on the parts of the industry that are just continuously chugging along quietly with little fanfare. For example:

- Coinbase continues to be a market leader in exchange volumes, venture capital and M&A, leading to it’s stock price being rewarded (+340% YTD)

- Smart contract protocols and DeFi applications continue to work as designed with no down-time and few hiccups

- Tether continues to be the leader in U.S.-dollar stablecoins while racking up record profits

Prior to 2022, Tether was considered the greatest threat to crypto and some even considered it a threat to the global economy. Rumors swirled for years, many completely unfounded, about whether or not the U.S. dollar stablecoin was, in fact, fully backed by dollars and short-duration assets. Many believed Tether was on the wrong side of the law and could be shut down. So how did Tether respond?

By kicking the crap out of its competition. USDT AUM rose steadily throughout the year as its competitors (USDC and BUSD) fell apart or further behind. Meanwhile, Tether is planning to release real-time data on their reserves and has

supported the Department of Justice in arresting illegal activity. The company has also shared letters with the U.S. Senate Banking Committee on how to

fight illicit use of its stablecoin. And Cantor Fitzgerald CEO, Howard Lutnick,

publicly and casually revealed that it custodies much of Tether’s U.S. Treasury reserves.

Step-by-step, crypto is cleaning up its ecosystem. Many questionable players are gone, and a few new players are emerging, but let’s not forget to pay tribute to those who are quietly doing their jobs.

Further, while most people are focusing on the SEC and Congress’ seemingly lack of desire to definitely define and regulate U.S. crypto law, other government agencies are doing their jobs. The Financial Accounting Standard Board (FASB)

issued guidance on how public companies in the U.S. can account for digital assets on their balance sheet. Prior to this guidance, the standard had been to account for Bitcoin as an intangible asset, which is initially held at cost on the balance sheet and written down on price declines, but never marked up unless it is sold. With the new guidance, Bitcoin will now be marked at fair market value, written u

p or down depending on the change in its price. As Galaxy Digital wrote, “FASB previously rejected requests to update the rules on three separate occasions going back to 2017 due to a lack of corporate interest. That changed following a surge of interest from 2020-2022 as companies like Tesla, Square, and MicroStrategy began holding bitcoin on their balance sheets. Globally, at least 28 public companies currently hold bitcoin accounting for 1.2% of the total supply.”

While Bitcoin is likely a terrible asset to own for most corporate treasury departments from a volatility standpoint, it remains a great asset to own for functional purposes. There is little expectation that companies will start buying Bitcoin for their balance sheets solely due to the FASB change, but it should not be dismissed that MicroStrategy (MSTR) stock has risen +293% YTD. Many small companies with little growth prospects but stable businesses (like MSTR) may start to mimic this successful playbook.

Overall, the path forward continues to clear as each roadblock gets knocked down. While the squeaky dysfunctional wheel gets all the press, we offer a holiday “tip of the hat” to the quiet, successful leaders.

Solana – We’ve Seen This Playbook Before

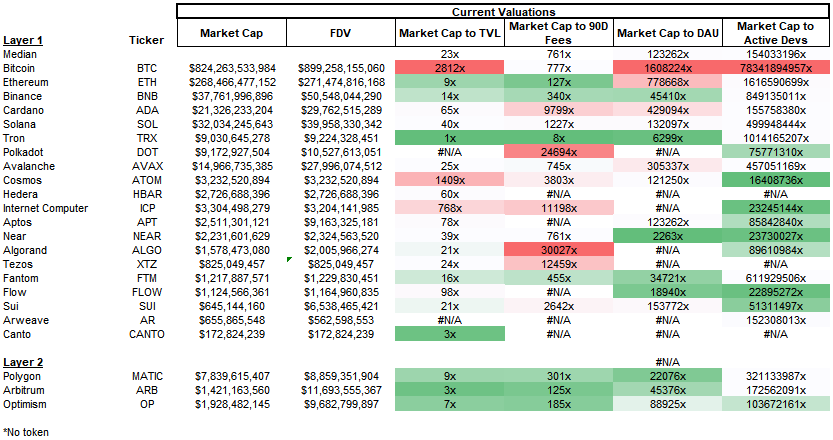

Layer-1 blockchains and smart contract protocols soak up much of the market’s focus. Dispersion was back last week in space with more than 40% variance in performance between top tokens. ICP (+38%) and AVAX (+30%) sharply outperformed the market, with the latter seeing some memecoin-driven hype. SUI (-12%) and NEAR (-8%) underperformed as EigenDA partnered with OP Stack for data availability - a space that Near has been trying to make inroads in. Fees remain high and rising across the blockchain space as Ethereum remains congested with modest activity levels while other chains are witnessing an onslaught of meme-driven ordinal transactions filling blockspace. The market continues to find ways to value these tokens, with metrics like market cap to TVL, and market cap to active users, while others are trying to make sense of the multi-billion dollar valuations.

Source: Artemis.xyz and Arca Internal Estimates

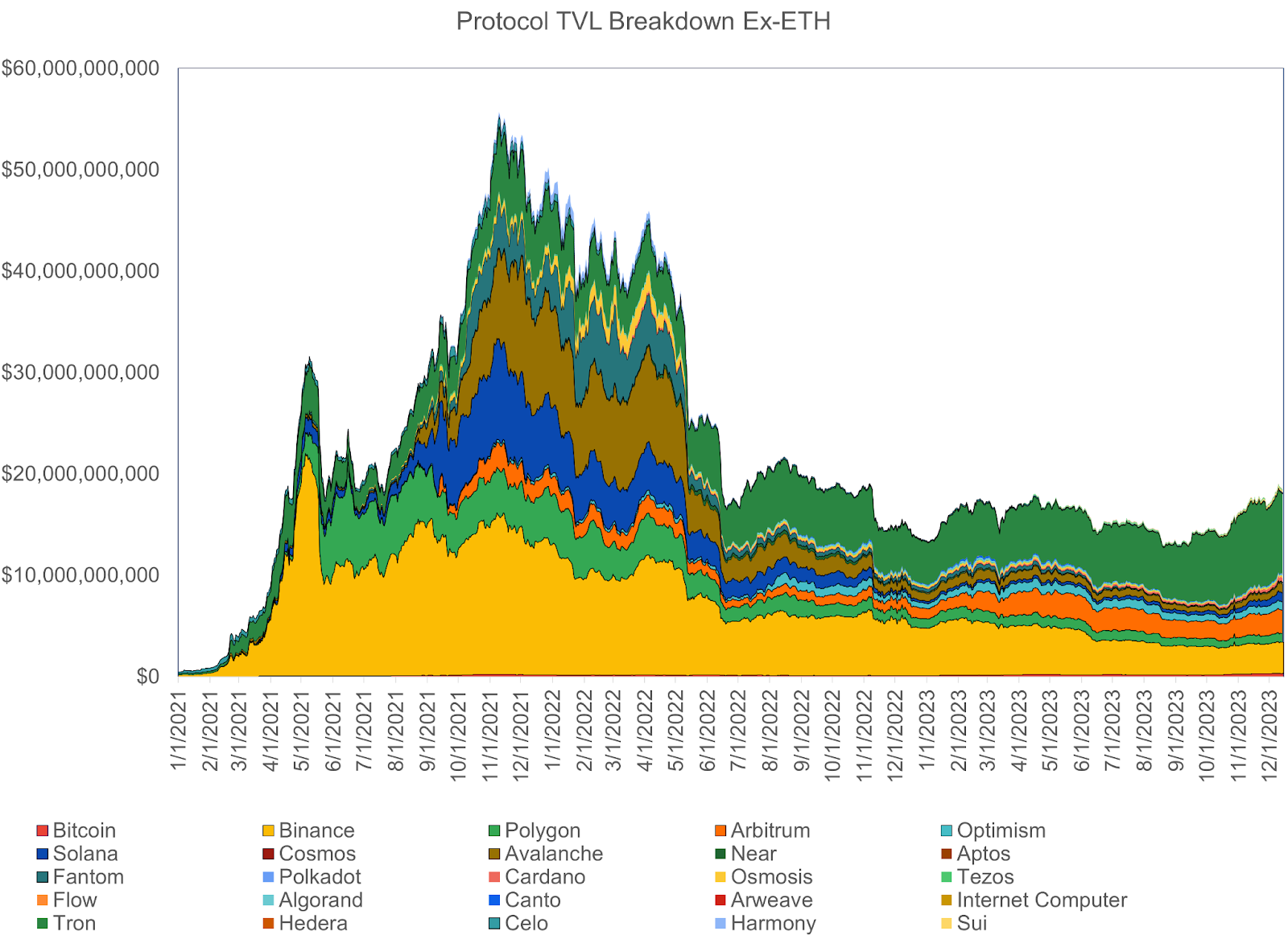

Predicting what drives smart contract protocol prices is difficult, and the relative value between chains sometimes seems almost random. But it is easier to spot growth in activity. Right now, that growth is largely coming from Solana. As

we wrote last week, airdrops are driving interest, which is driving higher prices, ultimately leading to more companies issuing airdrops. We’re seeing the same DeFi playbook and wealth effects that happened on Ethereum in 2020 and 2021, which are currently playing out on Solana. However, one thing we’re not seeing is a real spike in TVL. Total Value Locked (TVL) essentially measures the amount of capital being parked and utilized within a protocol. But the numbers can be very misleading. While some capital in each protocol matters, it often reaches the point of diminishing returns very quickly. For example, if you throw a party with ten people, the first chair you add is additive, and the second chair is probably even more additive. Perhaps even the first 10-15 chairs will lead to more conversation and a few more guests. But adding 1,000 chairs doesn’t change much. While much of the 2020/2021 Ethereum-based rally focused on TVL as an essential measure, this Solana renaissance is occurring without a lot of wasted capital being parked in the ecosystem.

TVL is a fairly worthless metric regarding price gains and ecosystem strength.

Source: Artemis.xyz and DefiLlama

So what is Solona doing differently? It’s using rewards and airdrops. For example, Solana Saga phones sold out on Thursday– not because the phone itself is a real success, but because the associated airdrop from BONK that comes with the phone (previously ~$10) overrode the cost of the phone itself.

And what is Bonk? Well, it's another Solana-based ecosystem with real activity, but not a ton of dead capital parked there. BONK is an app store within the Saga phone. It is similar to an experience on Apple or Google's app stores. For example, for a game in the Apple Arcade, microtransactions can occur within a game to buy artifacts, skins, etc, and all the user has to do is double-click the side of their phone to pay with Apple Pay, which seamlessly connects to the game/app experience. A similar user journey is being attempted with BONK in Saga, where games, using DeFi and Social apps on BONK connect to Phantom, Solana's wallet. Arca’s own David Nage spent some time in this ecosystem over the weekend and provided a first-hand experience:

1) EV.IO game - First-person shooter game where you get BONK skin and earn BONK- it’s essentially Fortnite on your phone. The game is at basic levels right now, but there was real activity on the app throughout the weekend.

2) Bonk or Bust -A betting game. Is the next number being drawn higher or lower than the previous number pulled? You can bet with your BONK.

3) Aurory - Kind of like Pokémon/Zelda play.

4) Photo Finish - A virtual horse betting game that allows users can own the horse (an NFT). You can bet on horses using BONK.

5) Bonk Earn - BONK Earn allows a user to buy back and burn BONK

This is just one example of many where applications built on Solana are being used, but not passively locking up capital. Helium (HNT +70% week-over-week), one of the leaders in DePIN (decentralized physical infrastructure), is another example where daily new subscribers continue to explode as Helium's MOBILE farming token was up 560% last week. At the current prices, people who buy a Helium Mobile subscription are now easily making back their $20 subscription fee for providing their data to Helium Mobile. New subscribers were up 88% last week.

So, while this does feel like a redux of the 2020 and 2021 Ethereum season, the mechanics of how it is occurring are somewhat different. Instead of sending capital into a smart contract and waiting, users are playing games and interacting with products to earn more Solana-ecosystem tokens. Whether or not this is sustainable remains to be seen, but it’s nice to see a slightly different approach to user engagement and growth.