What happened this week in the Crypto markets?

Source: TradingView, CNBC, Bloomberg, Messari

A Jam-packed Week but Little New Information

Last week there was a plethora of data to parse through, but ultimately, only a few pieces of new information are driving digital asset prices.

Let’s start with a continuation from last week. Regulatory concerns remained the main driver of dispersion among digital assets last week with MATIC, SOL, and ADA among the biggest laggards following delistings on Robinhood, eToro, and Bakkt. (Watch What’s Driving Token Prices for More Information). Some of these so-called securities also came under pressure due to new updates in the Celsius and Voyageur bankruptcies, which suggested that many tokens would be sold into USD stablecoins or Bitcoin and ETH in the coming weeks. This selling pressure was definitely new information, and weighed heavily on prices.

Next, the Fed. The June FOMC meeting resulted in rates staying unchanged as expected, but the new dot plot accompanying this statement suggested that another two 25-basis point hikes may be possible this year. The dot plots were new information, and in a vacuum, it can be viewed as a negative for all risk assets including digital assets. But as we’ve argued in the past, at this point, the rate of change versus expectations is still quite small relative to last year when there was a 400 bps+ difference between expectations and reality. The fact that global markets seemed to react more to traditional economic data last week than inflation/Fed data suggests that markets are now keying in more on recessionary fears versus inflation fears.

Next up, Washington and regulatory status. The House Financial Services Committee held a full committee hearing titled “The Future of Digital Assets: Providing Clarity for the Digital Asset Ecosystem”, which was largely a non-factor for prices since most of the discussions were reiterations of past debates, and any Congressional action would be years away anyway. There was one strange piece of new information though. A broker-dealer, Prometheum, which was recently granted a special purpose license from the SEC to handle crypto asset securities, argued that no additional legislation or regulatory authority was required, which sounded a lot like an SEC puppet. This Prometheum story is VERY strange, though it had no impact on price.

Next, in the ongoing SEC versus Ripple legal battle, the long-awaited emails between SEC members ahead of a 2018 speech by former SEC Head of Corporate Finance, Bill Hinman, were finally released. While not powerful enough to likely change the outcome of Ripple’s case, or add any value to the XRP token, it did shed light on the fact that Hinman did not act alone as some rogue “opinions are mine and not the SEC’s” actor. It was clear that many members of the SEC across different divisions had views on what is and is not a security, and that this speech had been very carefully crafted and reviewed. This has the potential to be mildly positive for ETH as it further cements its status as something other than a security, but, currently, it has mostly not been relevant to prices broadly.

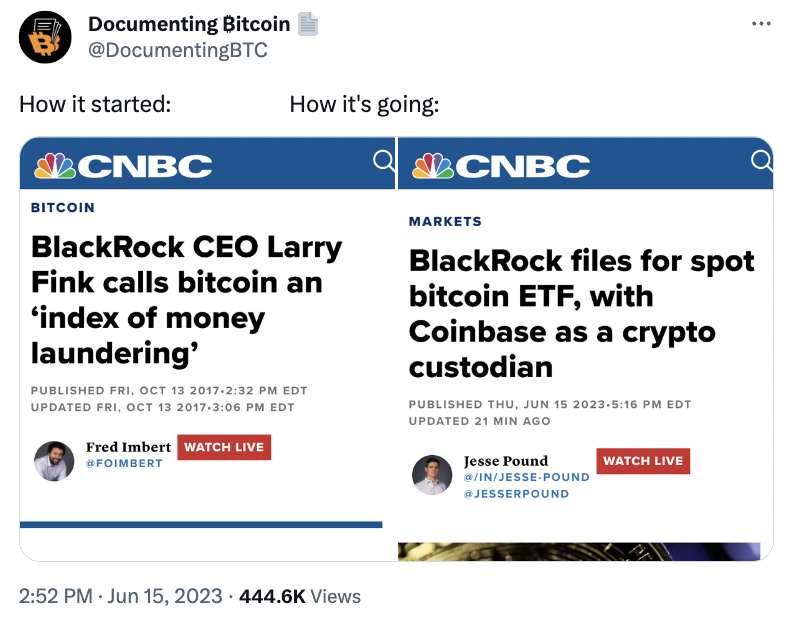

And finally, in a rare bout of positive news, Blackrock announced that it filed an application with the SEC for a Bitcoin ETF, which I believe was the 60th+ attempt at a Bitcoin ETF filing. This was very unexpected, and was undoubtedly new information. Blackrock has an almost perfect record with regard to ETF application success. The SEC has almost 9 months to review this application, but it will certainly lead to some new information regardless of the outcome (either it is approved, and we have to question why Blackrock versus the others, or it is denied again and we’d be left to question Blackrock’s decision). As is always the case, crypto twitter was fast in pointing out the hypocrisy.

The real story is that TradFi is slowly but surely beginning to take advantage of the demise of crypto-native startups. BlackRock filed for a spot Bitcoin ETF, Soros Fund Management said crypto is ripe for a takeover from Wall Street, Fidelity continues to grow its crypto trading and wealth management services, and the Citadel-backed digital assets exchange EDX is planning to go live later this year. We had argued recently that in a U.S. regulatory stalemate, the large market leaders (Coinbase, Binance, dYdX, Uniswap, Aave, etc) would keep growing since competition and new startups were being stifled. Now it’s clear that competition could be coming in a different form.

A 1-Year Lookback

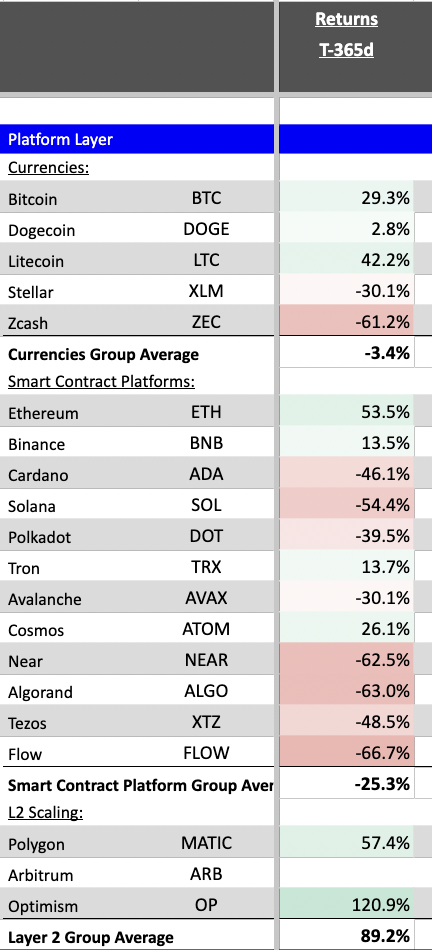

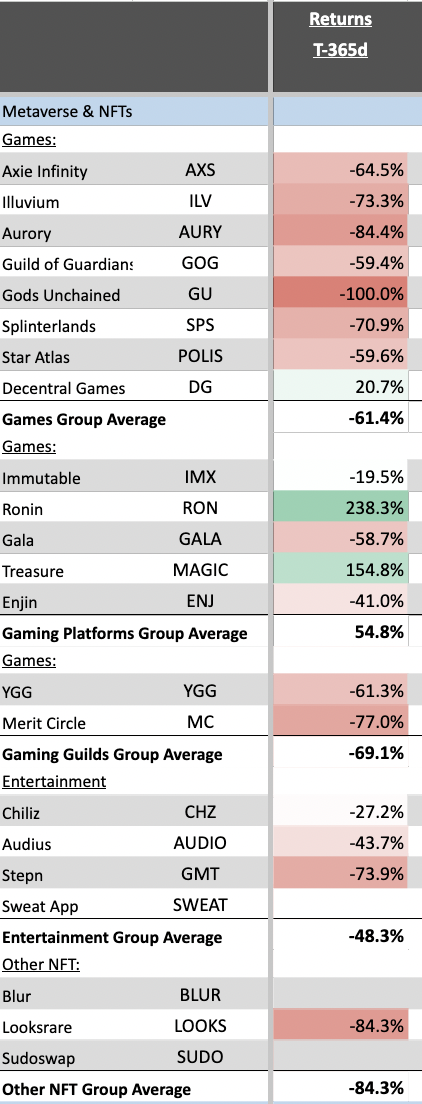

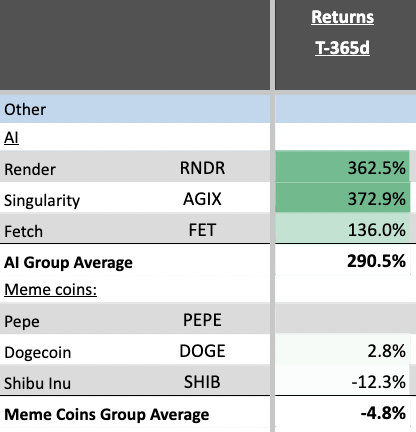

As we approach the end of the 2nd quarter, it’s an interesting time to start reviewing where the digital assets market has been over the last 12 months, because mid-June 2022 marked the beginning of the post-LUNA/3AC/Celsius recovery (mid- July is when prices started going higher again, but the market stopped going down in mid-June). While a lot more bad news ultimately came out in the 2nd half of 2022 (BlockFi, Genesis, and ultimately FTX), most of the damage, as it pertained to investable, liquid tokens came in the 1st half of the year. The successful Ethereum merge in 3Q 2022 also sparked a real rally in between massive detrimental events.

With that said, while digital asset market participants, especially those with an ax to grind, spent most of the past 18 months talking about how all digital assets were going down in a highly correlated vacuum, the actual data says otherwise. There has been quite a bit of dispersion in prices over a 12-month period, with certain sectors like Gaming and NFTs getting hit especially hard, and layer-1 blockchains (besides ETH) falling precipitously from the 2021 highs. Strength in Bitcoin, Ethereum, memecoins, AI-related tokens, decentralized derivative tokens and liquid-staking provider tokens bucked this trend.

We often get caught up in week-over-week and month-over-month trends and correlations, but ultimately, over longer time periods, the “haves” and the “have nots” show up in digital assets just like in every other asset class.

Source: Coingecko and Arca Internal Calculations

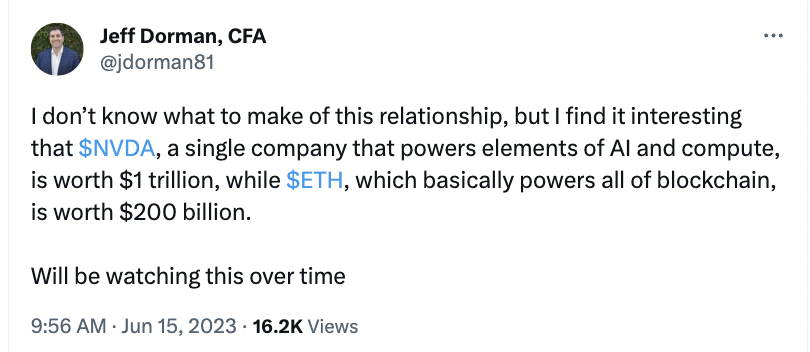

Nvidia Versus Digital Assets

I posed this question over Twitter last week, and I was fascinated by the traction and the responses.

One of the more interesting responses was as follows:

- The AI total addressable market (TAM) is greater than the blockchain TAM.

- ETH regulatory risk > NVDA regulatory risk

- ETH competition > NVDA competition (right now)

Hmm. Point 1, maybe. I’m not sure anyone really knows yet, and I certainly doubt investors are making a conscious decision right now to segregate the two. Point 2, maybe, I guess. But AI is going to start getting regulated at some point for a majority of its use cases. And Point 3 made little sense to me, as it will always be easier to create a product supplier similar to Nvidia than it will be to create core infrastructure that is part of everyone’s daily workflows (like ETH or Apple).

Regardless, it just struck me as an odd relationship, and I’m very interested to look at this again in one year’s time.