Source: TradingView, CNBC, Bloomberg, Messari

Increased Global Liquidity is Driving Markets

Stocks and crypto resumed their winning ways last week. We may sound like a broken record this year, because we’re likely going to be singing the same song over and over again. Global liquidity is on the upswing, and against this backdrop, we will continue to see strength in both stock markets and digital assets. In fact, with the upcoming Bitcoin halving, continued spot ETF inflows, U.S. equities at all-time highs, favorable monetary policy in China and the U.S., expectations for lower interest rates but no recession, and a full year removed from the 2022 crypto bankruptcies and fraud, it would not be outlandish to believe that this is the best setup the digital assets market has ever had.

Source: Financial Times, CrossBorder Capital

Interestingly, much like the Magnificent 7 tech stocks continuing to drive nearly all of the positive performance of the U.S. equity market, we’re seeing a similar story play out in the digital assets market. A basket of the strongest tokens and coins from October to December, mostly in sectors like AI, Gaming and DePIN, continues to show the most strength and upside price dispersion. This basket has once again broken out to new highs (blue line on the chart below) even as the total market cap of the entire market is still well below the highs (orange line). This basket has very high up-capture and very low down-capture, a measure of beta. On good market days, this basket rallies the most- and on bad market days, this basket is most immune.

Source: TradingView

Inevitably, this basket will likely change over the year as new sectors and tokens break out, but the sentiment will most likely persist. The strong get stronger.

What We’re Monitoring from the Research Desk

As always, there were a few outperformers and underperformers last week, but for the most part, it was a pretty uneventful week with steady, broad gains across the board. So in lieu of anything specific to highlight, we thought it would be a good week to highlight what our research team focuses on in a given week. While the headlines will always skew towards Bitcoin, Ethereum, Coinbase, and maybe even Solana, there are still thousands of other data points to monitor on a weekly basis. Below are a few:

Market transactions and overall activity were down quite a bit last week, with the week-over-week declines driven by reduced stablecoin, DeFi, and gaming activity.

Source: Artemis

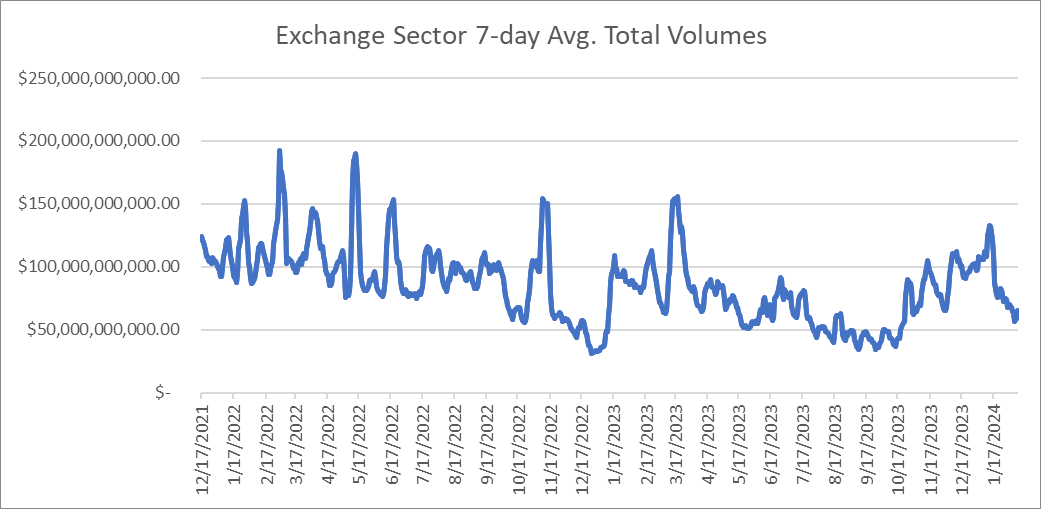

Exchange volumes continued their decline last week, falling 4% week-over-week. These declines were led by DEX volume underperformance falling 16%. Thorchain (RUNE) and Pancakeswap (CAKE) saw volumes decline 25% and 21% respectively. Coinbase was the largest outperformer with volumes up 5%.

Source: Coingecko, Token Terminal and Arca Internal Calculations

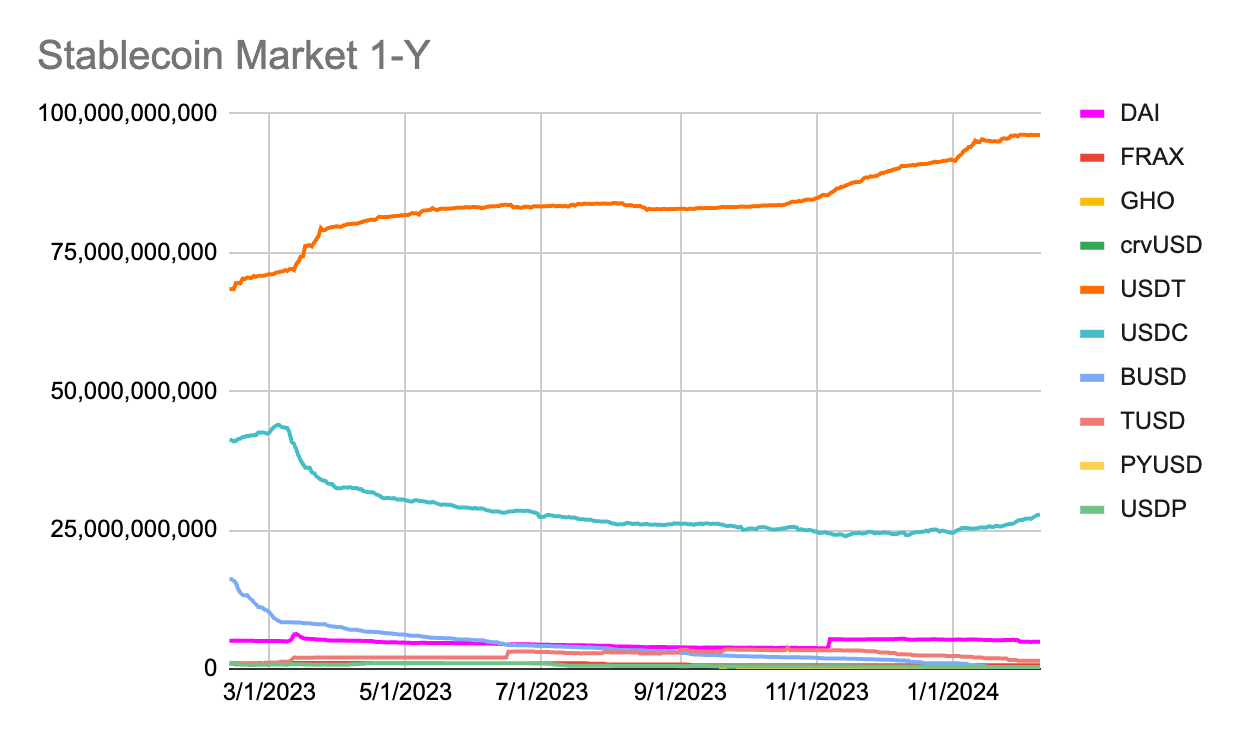

Stablecoin AUM contracted -1.20% week-over-week, led by a continued decline in BUSD (-14.88%) as its full unwind towards $0 AUM continues. GHO, the new stablecoin from Aave, managed to reach its $1 peg after failing to keep its peg since launch.

Source: Coingecko and Arca Internal Calculations

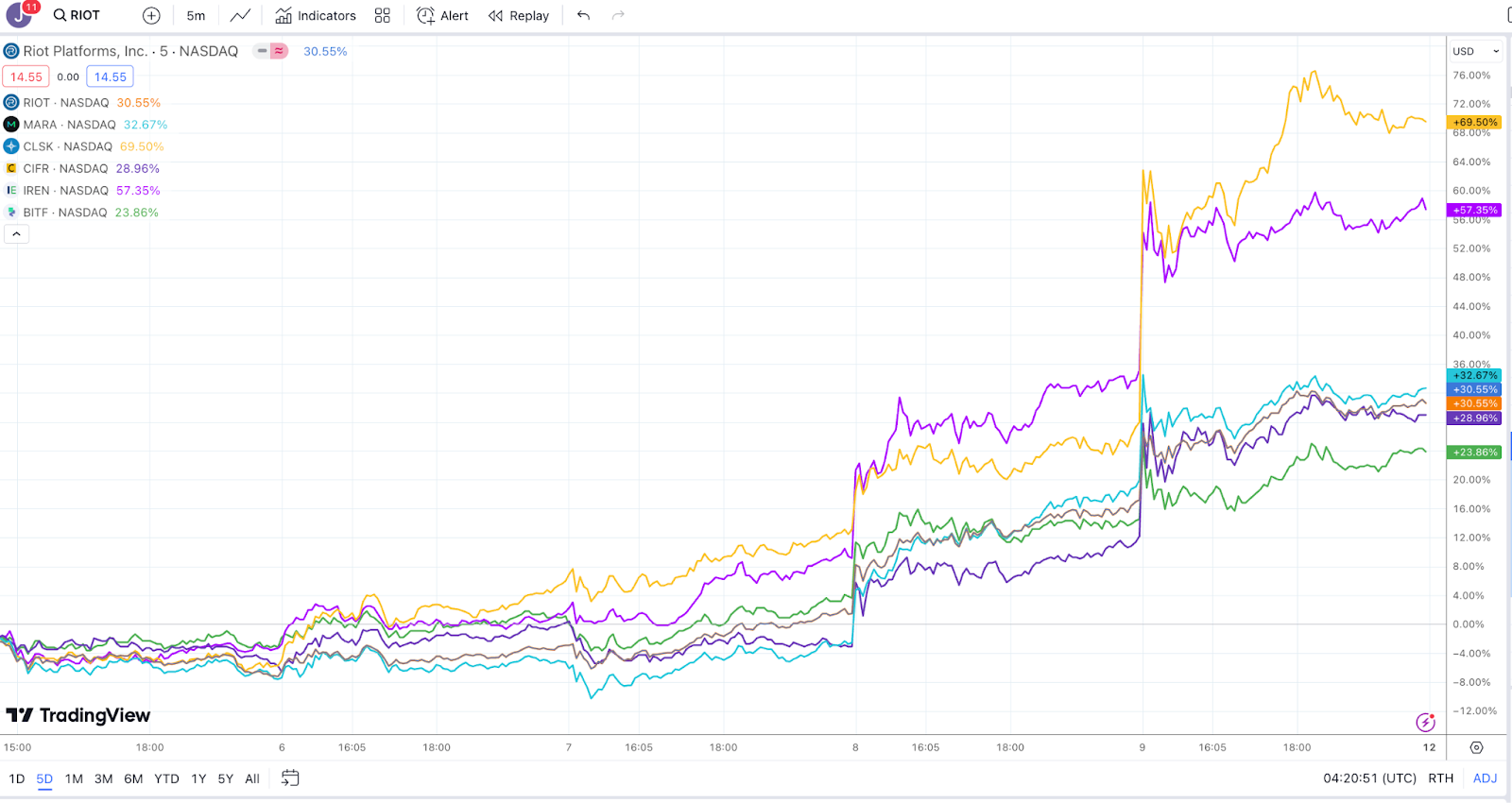

Bitcoin miners had a strong week, with prices rebounding significantly from the steep January sell-off. Most mining stocks gained +20-70% last week. Hash price has improved, rising from $75 to $83. This improvement was primarily driven by growth in BTC price, as transaction fees as a percentage of blocks declined from 7% to 5%, while Hashrate remained unchanged. Cleanspark (CLSK) experienced the most substantial price gains after surpassing expectations on EBITDA and earnings. This beat was propelled by the change in FASB rules, which now allow miners to mark their BTC holdings to market prices. These FASB rule changes will likely lead to outperformance for other miners as well when they report their Q4 earnings.

Source: TradingView

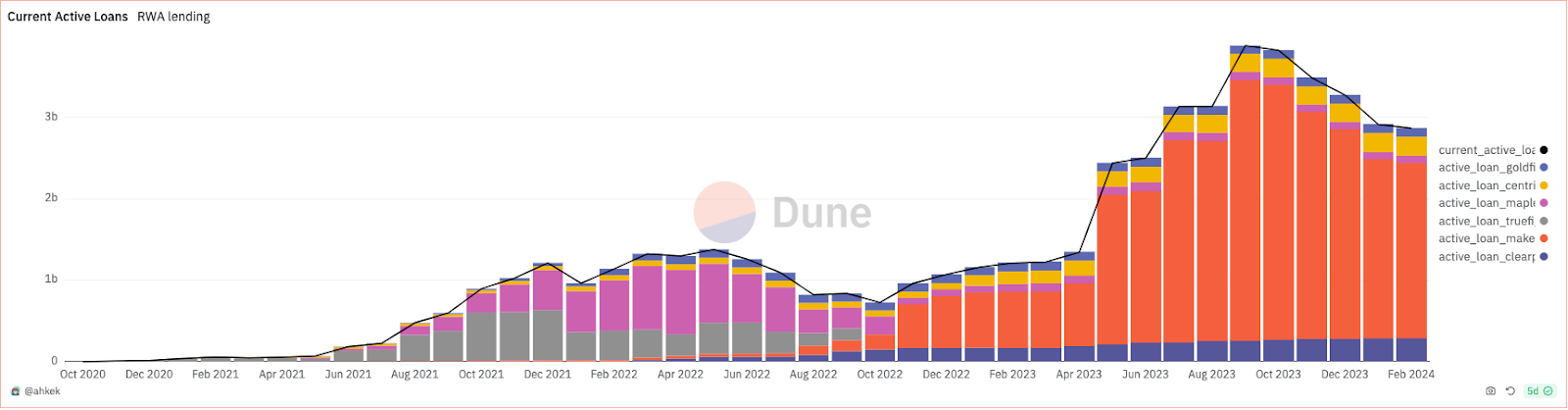

We saw another small move down in real-world asset loans as Maker and Centrifuge saw a small decline while all others remained flat.

Source: Dune Analytics

Smart contract platform tokens posted high single to low double-digit gains. SUI was up 22% as parallelized EVMs continue to be a hot narrative, while OP rose 16% after the announcement of Ethereum's Dencun upgrade on March 13th. APT underperformed (-1%) as the market finally differentiates it from SUI. Global TVL across all blockchains hit new highs, primarily coming from increasing flows into Eigenlayer after they once again raised caps on staking, now reaching nearly $6 billion of TVL.

Source: Artemis.xyz and Arca Internal Calculations

There are now tens of thousands of tokens, but we monitor only about 400-500 tokens with real business models and moderate trading liquidity. And even in an otherwise slow week, there is always a tremendous amount of data to analyze and comp tables to monitor.