Source: TradingView, CNBC, Bloomberg, Messari

Source: TradingView, CNBC, Bloomberg, Messari

There Are Still Pockets of Strength Amidst Some Broader Weakness

Facts:

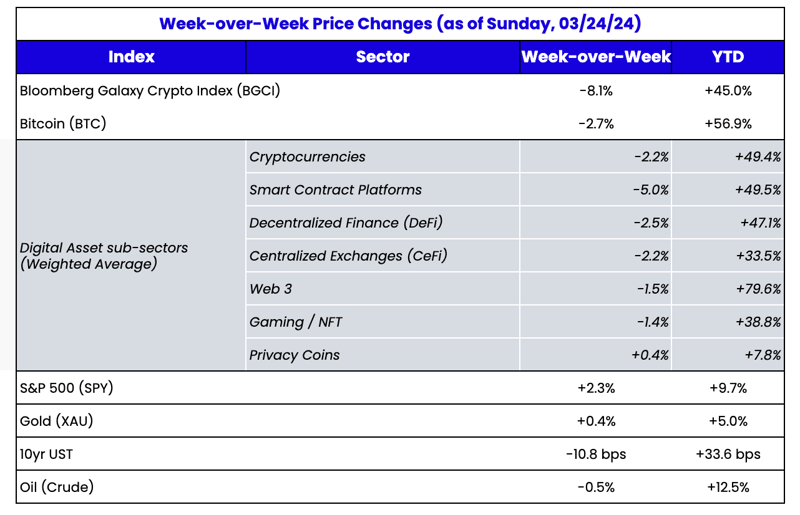

- Bitcoin is now up 59% YTD.

- The Bloomberg Galaxy Crypto Index (BGCI) is up 45% YTD.

- The S&P Cryptocurrency BDM Ex-MegaCap Index (SPCBXM) is up 45% YTD.

Yet the headline is that crypto has fallen for the past two weeks as Bitcoin spot ETF net inflows dry up. Which is true, but not at all material. After 7 straight weeks of inflows, bringing

YTD inflows to almost $13 billion (way ahead of the full 2021 inflows of $10.6 billion), Bitcoin inflows have finally

stalled, at least for one week. Bitcoin is now down a whopping 2% from the weekly close two weeks ago.

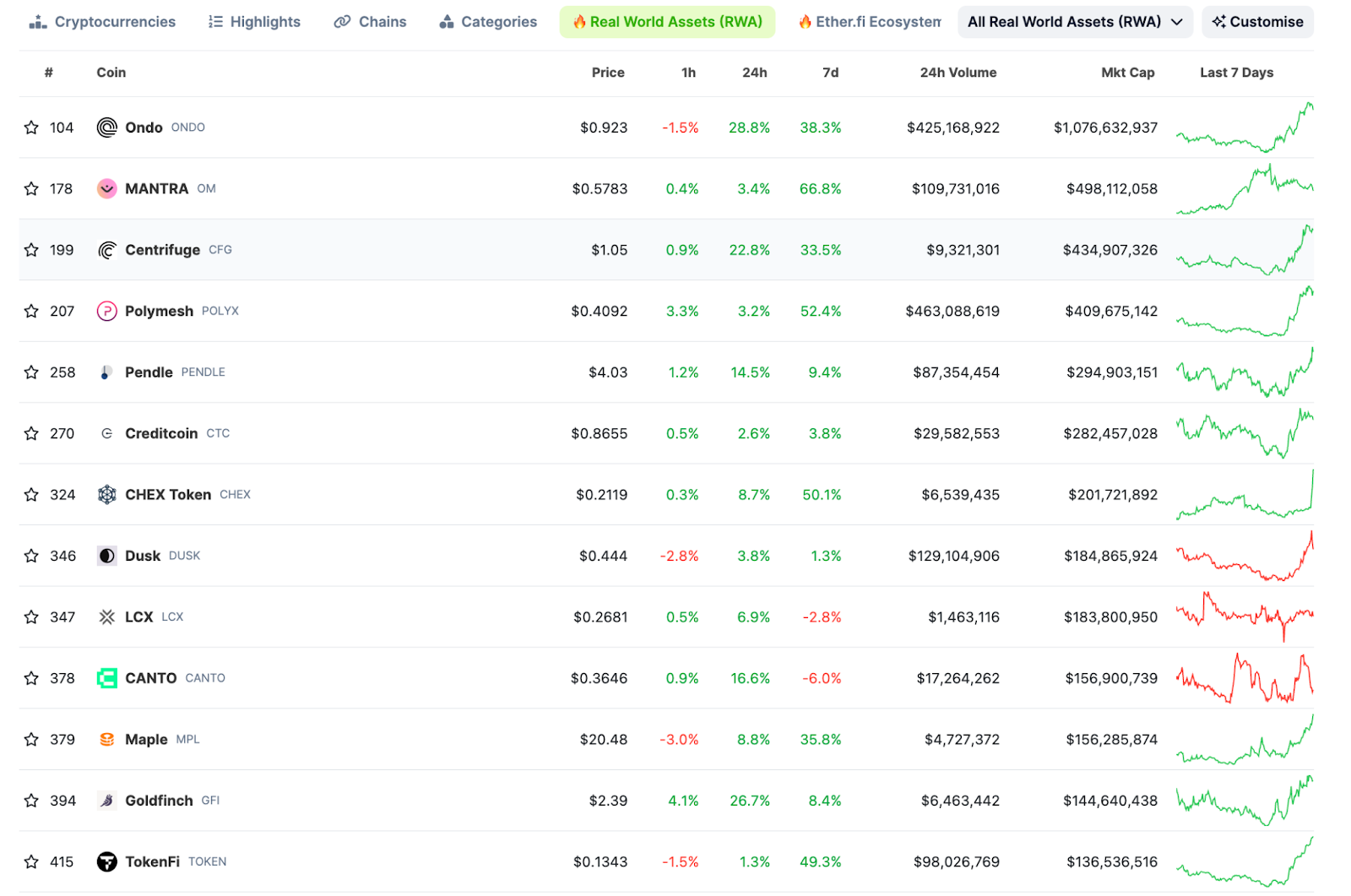

While all eyes were on Bitcoin and Ethereum, this is far from a broad-based selloff. The sign of a healthy market is dispersion and last week, it was real-world asset (RWA) tokens that took flight on the heels of yet another Blackrock announcement. This tim about its first foray into tokenized funds. The BlackRock USD Institutional Digital Liquidity fund (

BUIDL) will tokenize U.S. dollar yields on the Ethereum blockchain by investing 100% of its total assets in cash, U.S. Treasury bills, and repurchase agreements. Basically, it’s a yield-bearing stable token.

Ondo Finance (ONDO) is a competitor. Its brand-new token rose +35% last week and is now up 75% in the last 30 days.

Maker Dao (MKR), one of the oldest stablecoin projects tokenizing yield-bearing Treasuries, rose +8% last week and is now up +52% in the past 30 days.

Basically, anything labeled “RWA” is flying. As has been the case all year, Bitcoin generates the headlines and inflows, but other sectors are showing the depth and maturity of digital assets.

A Conversation with Steve Kurz of Galaxy Digital and Ari Paul of BlockTower

Last week, Arca hosted a roundtable titled “Investing Beyond Tokens” with myself, Blocktower CIO Ari Paul, and Galaxy Digital Global Head of Asset Management Steve Kurz. All three firms offer actively managed funds, and we discussed where this subset of investment strategy is headed. While the full video will be posted shortly, we wanted to highlight a few snippets from our conversation that we found insightful. It is important to note that these are just the opinions of Ari, Steve, and myself and should not be taken as investment advice. We do not believe investing in actively managed funds is correct for every investor.

- So far, it’s safe to say that the Bitcoin Spot ETF has been all the rage in 2024, with retail and institutional investors scrambling to get exposure to Bitcoin. With the success of the Bitcoin spot ETFs, it’s not hard to extrapolate that firms will be scrambling to release passive crypto products. We’re already hearing murmurs of an Ethereum ETF and passive token basket products.

- The tokenization and financialization of assets will be the biggest long-term opportunity. Though not the “sexiest” theme and not the ones that will have 20x returns and gain international media attention, real-world assets will become the future of finance. For those unfamiliar with the term, real-world asset tokenization refers to converting the rights of an asset into digital tokens on a blockchain. Real-world assets can include everything from real estate, bonds, stocks, or even illiquid assets like art. Though the full manifestation of real-world tokenization might take 10+ years, we’re starting to see investable projects already solving some of these issues in the current financial system. Ari Paul summarizes:

“Everyone sees the writing on the wall, BlackRock, JP Morgan, [etc]. They all know that most things are going to be tokenized in a decade, partly because regulators are going to require it and because you can embed compliance within the token itself. You can have complete real-time transparency… and we think there's probably 50 to 150 basis points of cost savings, depending on the kind of market, just by eliminating a lot of back and middle office inefficiencies.”

- Digital assets are starting to function like traditional finance. Though multiple crypto cycles have occurred over the past 15 years, the last two years have resembled traditional cycles. There have been many bankruptcies, including amazing investing opportunities from the FTX estate. There are publicly traded stocks now with many Bitcoin miners and companies like MicroStrategy (MSTR), Coinbase (COIN), and Galaxy (GLXY.CN). Some companies have issued convertible bonds, creating capital structure arbitrage opportunities. There are governance/”activist” opportunities where tokens have been trading 20- 30% below book value.

- This asset class Is still not fully professionalized. With clear regulation still lagging in this industry, there are no requirements for standardized reporting. Crypto companies do not have to give video conferences like other public companies; instead, you find information about a company from an AMA at 2 a.m. There’s a lack of solid benchmarks because the space doesn’t even know which assets will exist in 5 years. Many projects issue publicly traded tokens that are effectively pre-product stage, yet host multi-billion dollar market caps.

- Risk Management will continue to be the key to success for active managers. If you examine the cohort of crypto fund managers that started in 2018, a large majority have gone out of business. It may seem that in crypto, especially now, money is falling from heaven, but managing risk is the most important job. You need to understand counterparty risk, smart contract risk, compliance and regulatory risk. Unlike traditional finance, where buttoned-up counterparties are taken for granted since most firms have been around for decades, finding the right partners in digital assets is much more difficult. You must spend countless hours finding the right custodians, exchanges, and OTC desks - and determine the tradeoff of making money versus keeping assets safe. In fact, all three of us believe that potential LPs should ask funds about their risk management procedures and ensure that the answers are well thought through before even considering their return profiles.

- What should institutions do before investing in digital assets? Before you decide which crypto investment vehicle to invest in, you need to have a stance on the digital assets space. As Steve Kurz puts it:

“Develop a view that's clear about this space. And that doesn't mean defending all of crypto, that doesn't mean understanding all of crypto, that doesn't mean getting distracted by the different threads or the public things… If you start with a clean slate today, and you look at everything that's going on… whether it's real-world assets…whether it's Bitcoin, whether it's a theory on whether it's the venture bet on the rails, whether it's DeFi.”

In addition to covering the topics above in greater detail, we dove into what actively managed funds can offer that passive products cannot.