Source: TradingView, CNBC, Bloomberg, Messari

Not An Exaggeration

Last week, I mentioned to a colleague that this was the most important, positive week in digital assets capital markets history. Immediately after saying it, I assumed that I had fallen victim to recency bias and that I was exaggerating. After all, I’ve been focused exclusively on digital assets for a long time, and there have been a lot of positive events in its short history:

- The first successful ICOs

- The Coinbase direct listing

- Paul Tudor Jones calling Bitcoin the “fastest horse” as it pertains to inflation hedges

- Tesla adding Bitcoin to its balance sheet

- CME BTC and ETH futures listings

- Bitmex launching perpetual swaps

- The rise of Crypto Kitties as the first real successful decentralized application

- Facebook releasing its Libra white paper

- The Uniswap airdrop

- The launch and subsequent rise of stablecoins

- JP Morgan Coin

- The Covid bump

- DeFi summer

- Record NFT sales

- The Ethereum merge

- And, of course, Blackrock applying for a Bitcoin ETF and subsequent ETF approval and launch

(There were plenty of negative events too – multiple China bans, Mt Gox bankruptcy, the BCH fork, countless hacks, the bankruptcies and fraud of 2022, operation choke point, etc – but we’re talking about last week’s POSITIVE events).

But as I thought about it over the long weekend, I doubled down on my original thought. This past week was UNDENIABLY the most important string of positive events in digital assets history.

The U.S. regulatory and political attitude towards digital assets, up until May 2024, was hostile. It was not uncommon to see the phrases “the SEC hates crypto” or “anti-crypto army” under the Biden administration over the past four years. It was perceived as normal to hate crypto inside of Washington. It was perceived as normal to hate crypto inside of Washington. But behind the scenes, numerous crypto advocacy groups and individuals worked hard to create change. And the Biden administration may have made one of the largest miscalculations ever with their anti-crypto stance.

|

Fifty million Americans own and love crypto.

A few hundred million people are pretty indifferent about crypto.

There are, what? Maybe a few hundred people who actually hate crypto and care about it enough to vote for anti-crypto policies?

|

This was a YUGE miscalculation.

“Perhaps the Presidential election will become that catalyst, as crypto has become a topic in political conversations. Mark Cuban has been outspoken about crypto's use cases and the unfriendly regulatory environment in the U.S. and last week stated that Biden could lose the election because of his anti-crypto politics. Former President Trump said, “If you’re in favor of crypto, you better vote Trump” at a recent Mar-a-Lago event. The election is still a way out, and markets are not positioning for the event yet, but this may prove to be a positive catalyst in the near future.”

We had no idea how right this would be. So, back to why this was the most important week (or weeks) in digital assets history, let’s review the timeline of recent events.

- May 8th: Donald Trump states, "If you're in favor of crypto, you better vote for Trump." These 11 words set off a political storm.

- May 16th: The Senate voted to repeal SAB 121, an accounting rule regarding how public companies (or their subsidiaries) should account for digital assets. A dozen Democrats joined 48 Republicans, showing the first of many cracks in the Democratic anti-crypto stance.

- May 18th: Anti-crypto FDIC Chair Martin Gruenberg steps down. While this decision had nothing to do with digital assets gaining steam in Washington, it was undeniably bullish for digital assets given the FDIC’s harsh pushback regarding crypto in recent years, including this joint memo from the FDIC, OCC and Federal Reserve following the collapse of FTX.

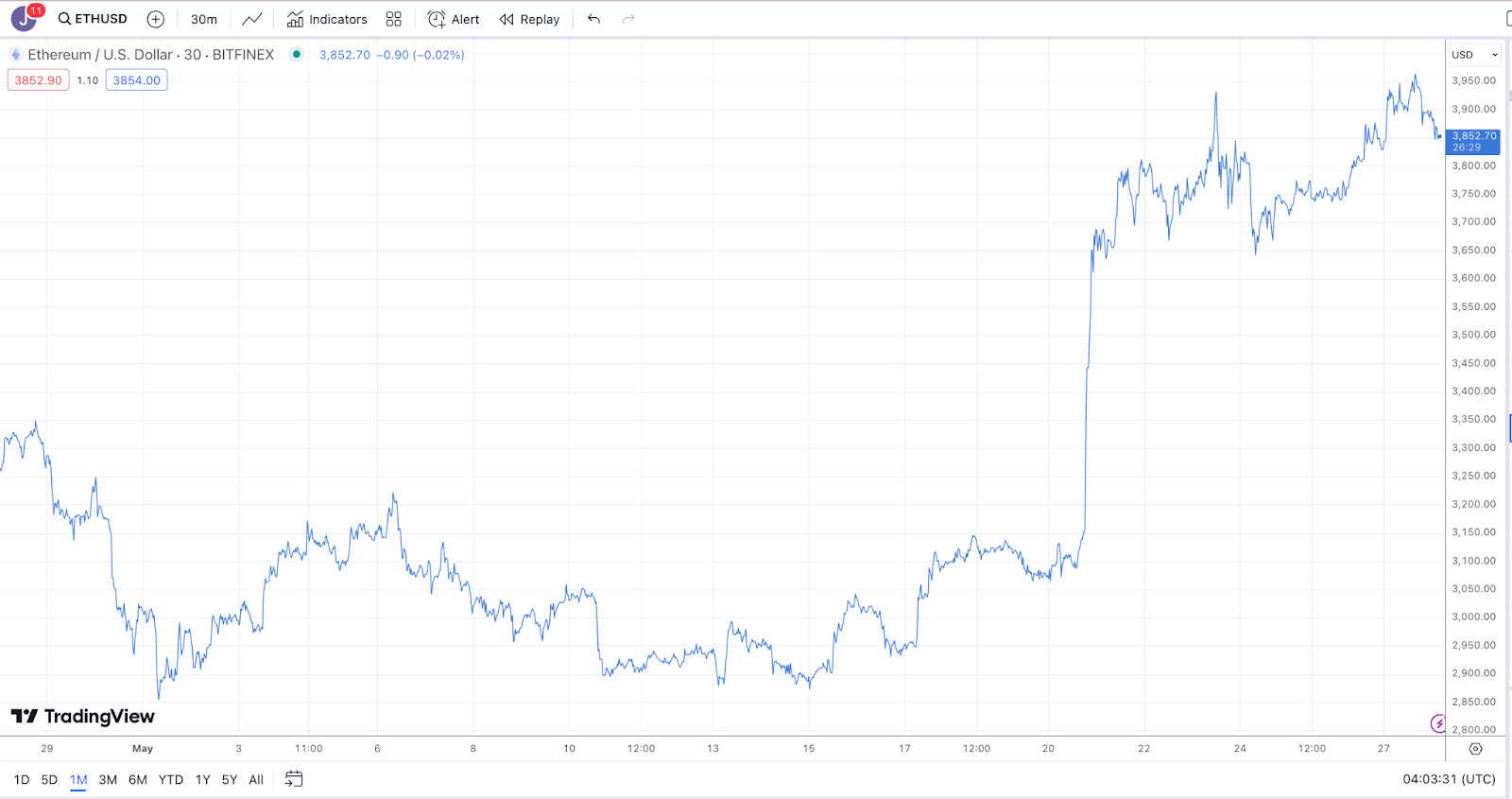

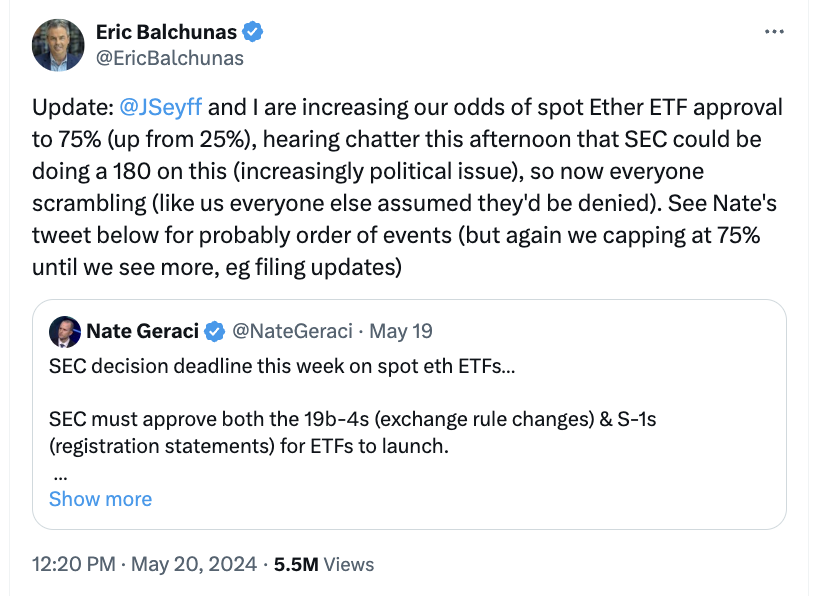

- May 20th: The incredible Bloomberg research team covering all things Bitcoin (and now Ethereum) ETFs tweeted that they were raising their expectations of an Ethereum ETF approval from 25% to 75%. This was a complete 180-degree pivot, and it was not an original miscalculation by the Bloomberg team. This about-face was based on new, and completely unexpected, chatter in Washington at the last minute ahead of the May 23rd deadline for the Van Eck ETF filing. It was this news that sent the price of ETH soaring.

Until this news, most traders were still hesitant to go risk on ETH after almost 3 years of underperformance versus Bitcoin and other major smart contract platforms like Solana (SOL). But ETH skyrocketed on this news. There was a lot of short-covering, and many traders were positioned “long anything, short ETH.” These large ETH/BTC and ETH/SOL shorts were looking to close these positions opportunistically, and many other investors were just trying to add to ETH given a general under-exposure.

Source: TradingView

- May 21st: Trump piled on the “pro-crypto” stance and launched a website that accepted crypto donations. It would be an understatement to say that crypto Twitter was donating fast and furiously.

- May 22nd: The House passes FIT 21. This bill paves the way for a federal regulatory framework for the crypto industry, fulfilling a long-standing industry demand. Importantly, it would allow most digital assets to be treated as commodities and thus regulated by the CFTC, not the SEC. A whopping 71 Democrats joined House Republicans to pass the FIT 21 Act. While this is just a bill, and it still needs to pass the Senate, and will likely see a lot of iterations before it becomes a law in its final form, it was an undeniably positive event and removes a lot of the U.S. regulatory uncertainty that just about every digital asset prospective investor has cited in recent years.

- May 22nd: The White House opposed FIT 21 but did so in a constructive tone that avoided a veto threat.

- May 23rd: The main event. The SEC approves 19b-4 filings of eight spot ether (ETH) exchange-traded funds (ETFs). The issuers must now wait until the SEC’s Corporate Finance division approves their S-1 registration statements, but we are likely to see spot ETFs go live in the next 4-8 weeks.

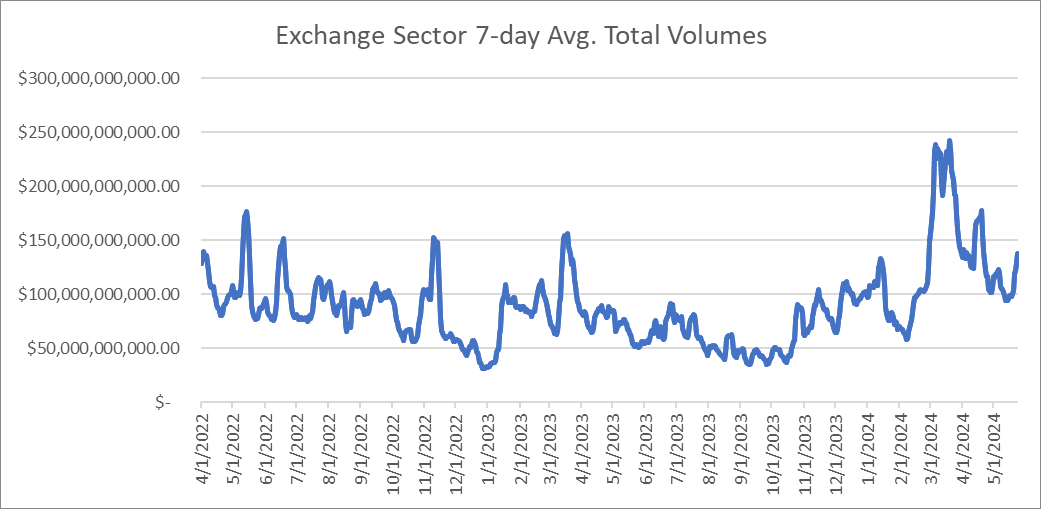

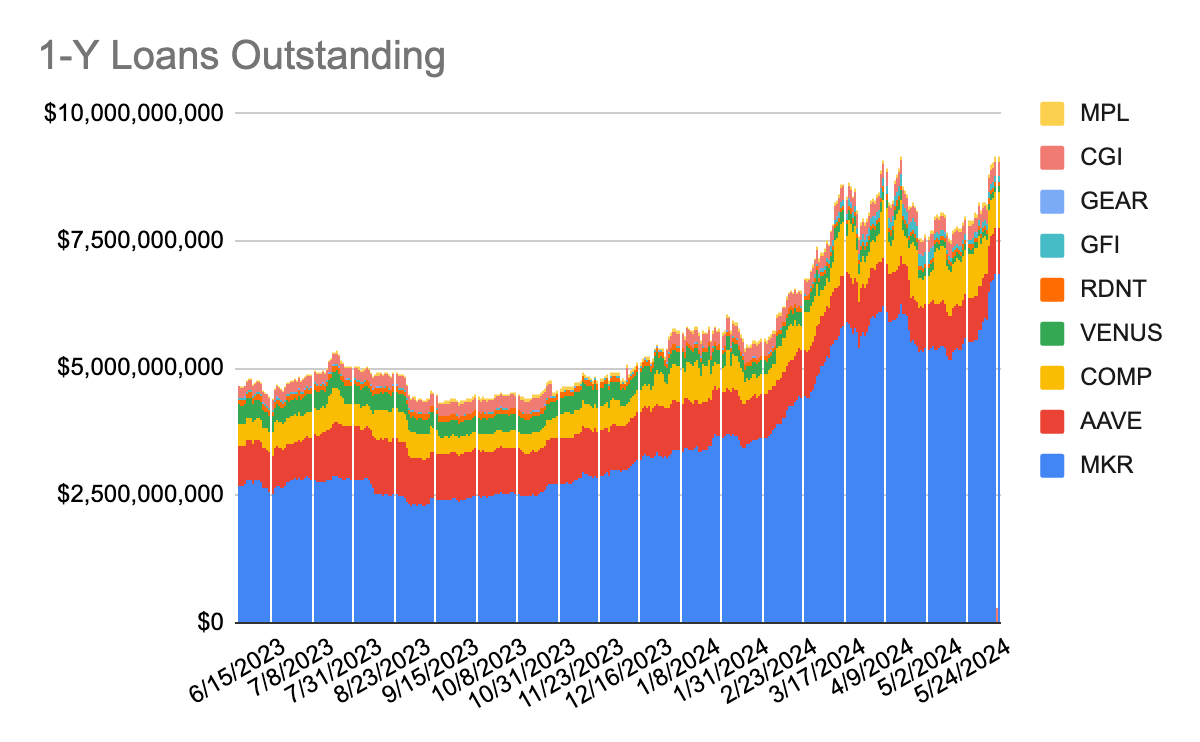

Make no mistake about it. This past week showed monumental progress on the U.S. regulatory front. The market reacted as expected, with solid gains across the board, especially in ETH and ETH-adjacent tokens (DeFi, staking, layer-2s). Total exchange volumes reached $977 billion, rising 42% week-over-week due to increased price volatility around the ETH ETF approval. Total decentralized trading saw the largest growth, with DEX volumes up 80% and DDEX volumes up 55% WoW. Coinbase was the largest outperformer, with volumes up 54%, which makes sense since Coinbase should receive additional volumes from custody of most ETFs. The news also pushed lending activity up last week, with deposits up +14.85% WoW and new loans up +5.67% WoW, with Aave leading the pack.

Source: Artemis and Arca Internal Calculations

Many investors' reasons for avoiding digital assets are being broken down and washed away one by one. Soon, investors will have to start making lists regarding why they need to own digital assets.