What happened this week in the Crypto markets?

Source: TradingView, CNBC, Bloomberg, Messari

“Bear Market” Rallies Are Just Low-Confidence, Low-Volatility Bull Markets

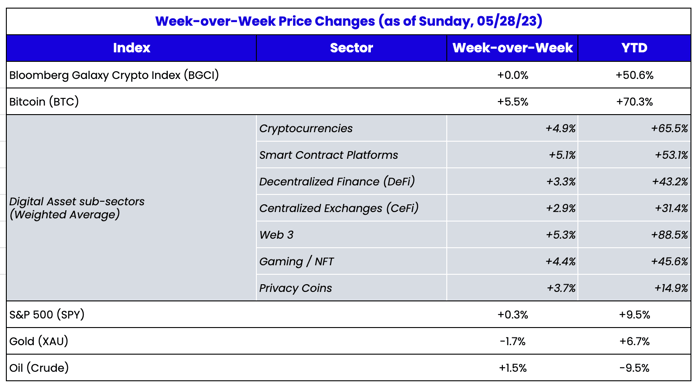

For all the doom and gloom, global markets keep chugging along. U.S. major indices closed the week in strong fashion with a 1.3% rally for the S&P 500 Friday and a more than 2.0% move higher for the Nasdaq. Nvidia, the world’s largest GPU manufacturer, saw its stock price surge over 25% after beating earnings and raising Q2 revenue guidance an astonishing 50% higher than Wall Street estimates, citing demand from AI customers. Other semiconductor companies and AI-focused crypto protocols rallied in sympathy. Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla are up a whopping 40%+ YTD, with the rest of the S&P 493 up a mere 1% YTD. The YTD performance gap between the cap-weighted versus equal-weighted S&P 500 has grown to the largest spread since 1999.

Elsewhere, of course, everyone knew the debt ceiling was a joke. Yet the resolution was still a sigh of relief for markets. Over the weekend, President Biden and House Speaker McCarthy compromised and reached a debt ceiling deal that offered little in the way of fiscal discipline. The deal suspends the debt limit until January 2025. It includes spending caps for the 2024 and 2025 budgets, reclaiming unused COVID funds, expediting permitting for energy projects, and introducing work requirements for food aid programs. Equity sentiment will likely respond positively to the news as it removes a large, though low-probability tail risk, assuming that the deal doesn’t fail at the last-minute vote on Wednesday. Meanwhile, rate cuts have been rapidly priced out, with June hiking odds back up to 70%, versus just 10–15% earlier in the month. Furthermore, the Treasury will immediately look to replenish its cash balance as soon as any debt deal is reached. It could potentially withdraw up to ~$400B in liquidity (via T-bill issuance) swiftly from the system.

Does any of this matter for digital assets? Not really. Most tokens have largely flatlined in recent weeks due more to a lack of participant interest than macro correlations. Bitcoin, for example, hasn’t posted a daily move of 6% for over 70 sessions—the longest streak of calm since October 2020. As NYDIG pointed out in their weekly bitcoin writeup:

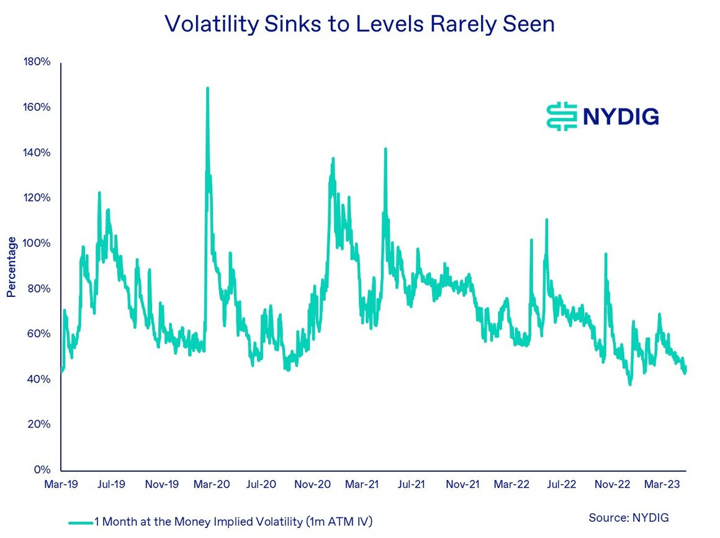

“Bitcoin’s volatility, as measured by the implied volatility of at-the-money options expiring in one month’s time (1m ATM IV), continues to fall, reaching levels rarely seen over the past few years. We noted this a few weeks ago, but with the bitcoin price continuing to languish since the fireworks of the regional banking crisis subsided a few weeks ago, the trend of declining volatility continues. This week the measure fell below the first percentile of observed 1m ATM IVs since March 2019.”

Source: NYDIG

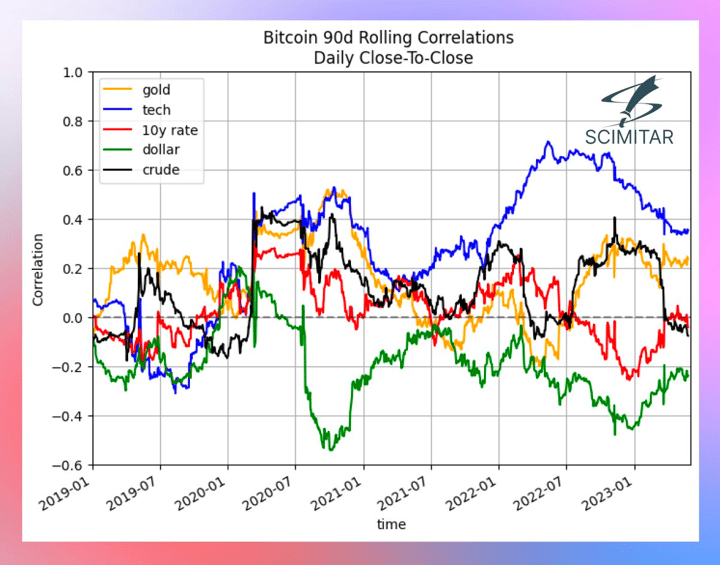

And it’s not just volatility that has collapsed. Correlations are disappearing too. We’ve talked at length about how bitcoin’s correlation to macro events has evaporated this year, with the only notable correlation being a negative correlation to regional banking stocks. And while that’s quite a shock compared to 2022’s “everything selloff,” it’s more in line with historical correlations (or lack thereof) that we were used to before the most aggressive rate hiking campaign in 40+ years. 2022 was the outlier; 2023 is just back to normal.

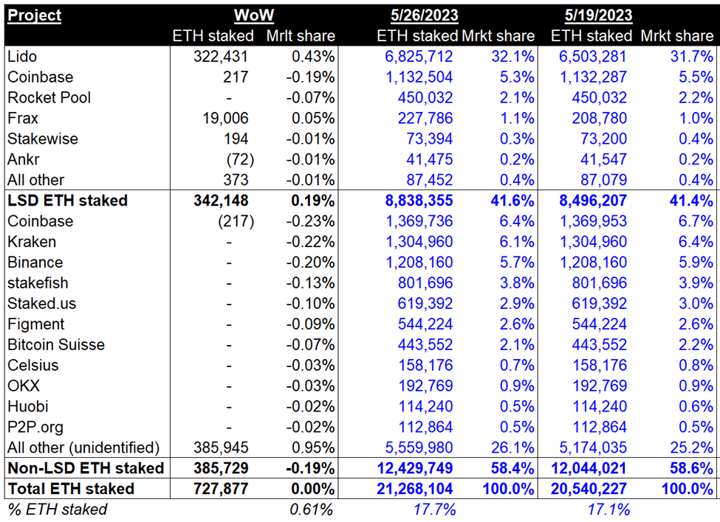

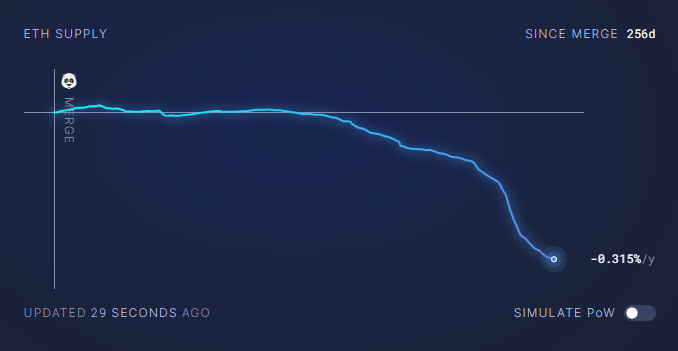

Moving away from bitcoin, however, we can see pockets of interest and strength re-emerging in certain areas of the digital assets market. Liquid staking tokens, for example, continue to benefit from increased interest in ETH staking post last month’s Shanghai upgrade. The percent of total ETH staked increased another 60 bps last week to 17.7% (up from 13% pre-Shanghai), driven by Lido and other unidentified protocols/parties. And the interest in meme coins (like PEPE) has driven ETH supply to new lows as the amount of ETH burned continues to outpace new supply.

Source: Arca Internal Calculations & Dune Analytics

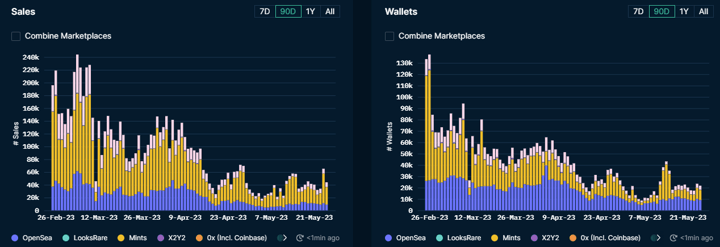

NFT marketplace volumes have also trended slightly upwards recently, as weekly active traders of NFTs have also shown relief. Floor price performance of top collections is varied, but the projects with strong momentum/narrative generally outperformed. Perhaps it's too early to call it a total reverse in course for our market, as NFT trading is still well below January 2023 marketplace numbers. But the convergence of collectible projects pivoting, gaming projects gaining steam, and AI's relationship with art are all potential positive narratives for the next 6 months and a glimmer of hope for NFT traders and collectors.

Last week, Sotheby's hosted the first wave of NFT auctions for the portfolio of Three Arrows Capital’s defunct NFT Fund, Starry Night Capital. The portfolio holds some of the most valuable and desired pieces of NFT art in existence. For example,

Ringers #879 (known as the Golden Goose) will be sold in the next wave of auctions. This piece is regarded by many in the art community as the most valuable NFT in any sector. Starry Night Capital originally purchased the piece in 2021 for ~$6M (1800 ETH). We expect the auction to clear between $1.5M-$3M. NFT auctions at Sotheby's typically have not done well in the past, but the first wave of auctions cleared at much higher prices than expected.

Put it all together, and you have:

- A low-vol environment with few, if any, macro headwinds ahead (1Q earnings and debt ceiling now behind us).

- Bitcoin has moved back to being completely uncorrelated to other markets.

- Sectors like AI and liquid staking are giving digital assets a bump.

- ETH tokenomics continue to move in the right direction, which may result in a huge demand/supply in balance when/if digital assets become popular again.

- NFTs are showing signs of life.

Maybe the bear market rally is really just a bull market.