Three Reasons Macro Factors Are Less Important Today

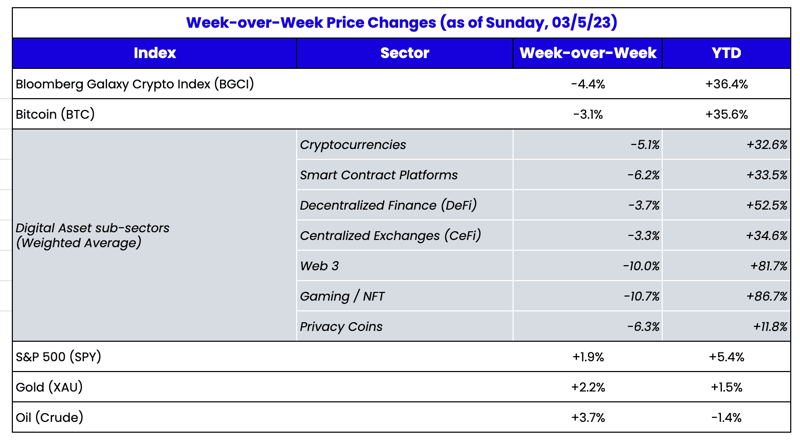

Last week provided more evidence that digital assets are back to being an uncorrelated asset set as digital assets reversed and equities gained. While ETH and BTC were only modestly lower week-over-week, many smaller-cap tokens fell 10-20% week-over-week, even as other risk assets, like equities and commodities, gained. The selloff came sharply on Friday, days after the news that Mt. Gox distributions (142K BTC) would begin in 2Q and 3Q, and Silvergate delayed its 10-K filing. The delayed reaction suggested that this was real selling pressure that potentially triggered some futures liquidations rather than an algo-driven response to a series of news. Moreover, the fact that the market largely flatlined and stabilized immediately after the Friday selloff suggests that it may have been just a single seller (or small group of sellers) rather than a market-wide panic. Regardless, it once again demonstrates the idiosyncratic price action of tokens and coins.

One of the most considerable changes to our investment outlook since the start of the May 2022 LUNA/UST-triggered digital asset market correction is that macro market conditions would have less impact on digital asset prices than we saw in the first half of 2022. Essentially, macro was driving the bus alone in 1H 2022, whereas it is now only a back-row passenger on a crowded bus. The reason for this change is three-fold:

- The rate of change at which macro conditions are changing relative to expectations is much lower today than in 1H 2022. Namely, 4 consecutive 75 bps rate hikes followed by multiple subsequent 25 and 50 bps hikes were multiple standard deviations away from the beginning of the 2022 year expectations of three 25 bps hikes. In contrast, today, the market is squabbling over a 25 bps delta. It’s just small potatoes.

- The negative and positive events in digital assets are so unique and far-reaching that their impact dwarfs anything else. On the negative side, we’ve had blockchain-specific implosions (LUNA/UST losing a combined US$30B market cap), service provider implosions (FTX, BlockFi, Genesis, Celsius, Voyager, and now Silvergate), and regulation-driven implosions (Kraken’s staking service, Paxos’ BUSD stablecoin, etc.) And on the positive side, every competitor to the walking dead mentioned above has increased market share at the expense of their fallen comrades, including Ethereum and DeFi applications. ETH has also benefited due to the success of the Ethereum merge, and Bitcoin has re-emerged as a viable investment thesis thanks to Ordinals and NFTs.

- Correlations between digital assets and equities have subsided, partially due to 1 and 2 above, but also because 2 of the biggest macro hedgers (Alameda/FTX and Three Arrows Capital) are out of the market, and many other macro funds with digital asset trading arms have pulled back substantially from the market. Often correlation has less to do with the assets themselves and more with the players, and many of the biggest correlation traders have left the market.

The 60-Day Correlation Between S&P 500 and ETH Has Fallen to Pre-May 2022 (LUNA Collapse) Levels

This past week, overall macro conditions took a back seat to two major events—the delayed 10-K report filing from Silvergate and the Yuga Labs NFT launch on Bitcoin.

Silvergate Is in Trouble Because its Customers Are in Trouble

Not long ago, market participants praised and envied companies with first-mover advantages in the digital assets arena. Those days are long gone, and Silvergate Capital (SI) may be the latest victim.

Silvergate Capital, a friendly banking partner for digital asset firms, is now on the brink of collapse. The California-based company, which at year-end saw 90% of its deposit base from blockchain and digital asset companies, made a few announcements last week:

These announcements follow the firm’s release of its

preliminary 4Q22 financial metrics on January 5, which revealed total deposits from its digital asset clients fell to US$3.8B as of end-4Q22 compared to US$11.9B as of end-3Q22.

In addition, Silvergate experienced another rush of deposit withdrawals from its digital asset clients, such as Coinbase, Paxos, Galaxy Digital, and others, which attempted to disassociate themselves from the bank. These withdrawals likely caused more losses for Silvergate as they needed to sell longer-dated bonds and other assets—presumably at a loss due to rising rates—to meet the withdrawals. The losses reduce its capital ratios further, likely leaving Silvergate undercapitalized. If Silvergate failed to meet certain capital requirements, it would receive a corrective action notice from the FDIC and its chartering authority or the California Department of Financial Protection and Innovation. Silvergate would have 90 days to raise capital or sell itself to another bank.

The SI stock fell 60% last week.

Source: TradingView

Banking is supposed to be a simple business. You borrow short-dated, you lend long-dated, and you earn a Net Interest Margin (NIM) assuming a positively sloped curve. And if you get in trouble from an asset-liability mismatch perspective, you can draw on various federal programs to maintain your solvency. Many pseudo “banks” in crypto got in trouble last year because they were greedy—they refused to run the simple business and instead made aggressive bets with customer money that did not pan out. But as Matt Levine puts it

rather eloquently, Silvergate looks to have done everything right as a bank but got in trouble because all of its customers messed up:

“... Silvergate is having a real run on the bank! It has lost money, not by making dumb Bitcoin loans — the Bitcoin loans are fine — but by doing the normal business of banking, borrowing short (taking deposits from crypto firms) to lend long (buying Treasuries and munis). Silvergate’s assets are real boring normal stuff, and if its depositors had kept their money at Silvergate, its bonds would have matured with plenty of money to pay them back. Instead, the depositors demanded their money back all at once, and Silvergate had to dump its long-term assets at big losses to repay them. The story today is that Silvergate’s customers are withdrawing their money because they are worried about Silvergate, “in light of recent developments & out of an abundance of caution,” classic bank-run stuff. But that's not why they were withdrawing their money in late 2022, when the trouble started. Then, they were withdrawing their money because crypto had collapsed: Silvergate’s crypto-exchange customers faced withdrawals from their customers, so they took their money out of Silvergate. The customers — crypto exchanges — were the problem, not Silvergate.

Whether Silvergate is ultimately seized by regulators or forced to sell itself to a stronger bank remains to be seen. But Silvergate is now relatively small, so a collapse will likely mean little to the market. Instead, the more significant and critical question for the markets is: who will replace the banking business that Silvergate dominated? Competitors have easily absorbed every other major failure in digital assets over the past 12 months. But since Silvergate was a U.S. bank operating for mostly U.S. crypto customers, and the U.S. regulatory environment is increasingly challenging for digital asset industry participants, it’s hard to envision that another bank will immediately gobble up this lost business.

BTC Ordinals and Yuga Labs

We have hesitated to write about Bitcoin Ordinals because it is a complex and new technological innovation on the Bitcoin network that we are still trying to comprehend fully. But one thing is clear—Bitcoin needed a jolt regarding use cases and narrative, and this development is certainly packed with new energy. See

Galaxy Digital’s detailed white paper for a primer on BTC ordinals.

In early February, the total number of “inscriptions” created was just over 1,000. Roughly one month later, that aggregate total is over 250,000, and users have paid over US$1.4M in fees to miners to include those inscriptions in bitcoin blocks. While this growth has been impressive enough as it is, enter the most successful NFT project to date.

Yuga Labs, the facilitator of Bored Ape Yacht Club, MAYC, Meebits, and many other NFT collections, announced its intention to build on Bitcoin.

Yuga Labs described TwelveFold as a limited edition, experimental collection of 300 generative art pieces inscribed onto satoshis on the Bitcoin blockchain. These pieces represent a complete art project and will not have other utility, interact with, or be related to any previous, ongoing, or future Ethereum-based Yuga projects. The collection explores the relationship between time, mathematics, and variability. When measuring time, the calculation base used is not uniform and varies from base 60 (60 seconds in a minute, 60 minutes in an hour) to base 12 (12 months in a year) and so on. TwelveFold is a base 12 art system localized around a 12x12 grid, a visual allegory for the cartography of data on the Bitcoin blockchain.

Yuga Labs' art team crafted the generative pieces in-house using 3D modeling, algorithmic construction, and high-end rendering tools. To participate in the auction, a buyer must have:

- A self-custodial wallet that holds the Bitcoin they want to use for bidding

- An empty Bitcoin address to receive the piece

The Yuga auction started Sunday at 3 pm PST and ends Monday at 3 pm PST. The current top bid (at the time of writing) was 0.63 BTC. This number will likely run higher throughout the auction but is still a bit lower than many, including us, expected. The top 300 bids at the end of the auction get the NFT. The market has its eyes on how quickly the auctions conclude, what price users are willing to pay, and whether users can figure out how to participate and properly handle their inscribed ordinals.

A few comps of this project are detailed below, which can help guide the pricing expectations:

BTC Ordinals Current Orderbook

|

Project

|

Top Bid (USD)

|

Top Bid (BTC)

|

Top Bid (ETH)

|

Ask (USD)

|

Ask (BTC)

|

Ask (ETH)

|

Supply

|

|

Ordinal Punks

|

$105,569.10

|

4.5

|

64.11

|

$106,742.09

|

4.55

|

64.82

|

100

|

|

BTC Rocks

|

$84,455.28

|

3.6

|

51.29

|

$23,459,800.00

|

1000

|

14,245.86

|

100

|

|

Inscribed Pepes

|

$24,445.11

|

1.042

|

14.84

|

$37,535.68

|

1.6

|

22.79

|

69

|

|

Timechain Collectibles

|

$93,839.20

|

4

|

56.98

|

$234,598.00

|

10

|

142.46

|

21

|

ETH Fine Art

|

Project

|

Top Bid (USD)

|

Top Bid (BTC)

|

Top Bid (ETH)

|

Ask (USD)

|

Ask (BTC)

|

Ask (ETH)

|

Supply

|

|

Fidenza

|

$80,000.00

|

3.41

|

48.48

|

$118,800.72

|

5.06

|

72.00

|

999

|

|

Chromie Squiggles

|

$18,150.11

|

0.77

|

11.00

|

$21,120.13

|

0.90

|

12.80

|

9734

|

|

Beeple Genesis

|

$49,500.30

|

2.11

|

30.00

|

$118,289.22

|

5.04

|

71.69

|

102

|

|

Checks Original

|

$2,904.02

|

0.12

|

1.76

|

$2,772.02

|

0.12

|

1.68

|

7780

|

|

Crypto Punks

|

$97,350.59

|

4.15

|

59

|

$104,759.13

|

4.46

|

63.49

|

10000

|

Considering comps, this fine art piece should be in line with (if not more valuable than) the current top Ordinals collections despite being 3x the supply.

More importantly, it will be yet another catalyst for the growth and future use cases of the Bitcoin blockchain, which hasn’t seen much creativity or new usage in several years.

Source: TradingView, CNBC, Bloomberg, Messari

Source: TradingView, CNBC, Bloomberg, Messari