Source: TradingView, CNBC, Bloomberg, Messari

Bipartisan Issue

If you love politics and crypto, this is your industry. But assuming you love digital assets and not politics, strap on your seatbelt because a big political storm is coming. As we

pointed out last week, the U.S. regulatory outlook has softened quite a bit in recent weeks and has created a more positive (or at least less negative) stance. That said, this is far from over. At the end of last week,

Biden followed through on his threat to veto Staff Accounting Bulletin No. 121 (SAB 121). While not the most consequential, it again highlights digital assets' Bipartisan nature. The Biden administration is unwilling to lay down even as members of its own party are laying down their arms.

While digital asset enthusiasts are wading deep into the Republican corner, let’s take a step back and apply some common sense. Crypto is making a mistake by wading into partisan politics beyond the issues relevant to our space. It’s one thing to support digital assets and lean towards supporting those candidates who agree with your ideals. That’s the perfect rationale and fine.

Crypto wants to be a single-issue vote this fall, but defending a convicted criminal who is notoriously fickle and prone to reversing course on topics is also risky. Right now, crypto doesn't have many enemies. It has a lot of supporters and many more who don’t care about digital assets at all, but it has very few actual enemies. And those outspoken enemies that do exist are quickly losing ground. This industry already has the support from the general public as underdogs who are trying to fix a broken system. And the industry is gaining political support on both the right and left. Crypto should not be partisan. There is no real reason to create enemies that don’t currently exist simply because we’re extrapolating a single issue vote into new issues.

We all want a fairer regulatory approach for digital assets in Washington. Still, it will almost certainly backfire in the long run if the industry loses support and creates a division within the country.

Calculating The Bankrupt Supply

One day, we’ll discuss the demand for digital assets more than the supply. I look forward to the days when the market cheers on supply shocks so that there is more to buy because demand is too strong.

But today’s market is still too focused on supply over demand. This is largely due to the sheer number of tokens coming to market and the insane VC lockups, but also partially because of bankruptcy re-org plans.

In the last week, we learned the following:

- In-kind Mt.Gox repayments worth around $9.8 billion, while telegraphed, are getting closer to repayment. Wallets tied to Mt. Gox were on the move last week.

- In-kind Gemini distributions worth around $2.2 billion have begun distributions.

- The cash settlement of the FTX estate, worth between $14.5 billion and $16.3 billion, will begin to be repaid next year.

These supply-side headwinds are already interfering with the relatively constructive view of digital assets. But it’s important to distinguish what is happening today from what is a relatively benign overhang.

To start, the FTX distributions are going to be in cash. While the debtor has celebrated a high recovery, the fact is that the cash distribution of 118% + post-petition interest is peanuts compared to what an in-kind distribution would have been. Over the past 18 months, the digital asset rally has far exceeded the recovery plan. But more importantly, these creditors will receive cash, and we already know that these creditors like digital assets. The majority of this distribution will likely be poured back into the market, creating a demand-side shock.

Gemini distributions were different. Most Gemini Earn customers were long-term believers in crypto, willing to lock up their assets to earn a yield. These creditors received a massive payday, in-kind distributions, and the highest bankruptcy recovery in history. Since the outcome was more favorable than expected, these creditors may sell at least a portion of their distributions.

Finally, the Mt Gox distributions are a mixed bag. While a massive amount of BTC and BCH is being distributed next year, the market may be overstating how much of this supply will

hit the markets and be sold. In layman’s terms, Mt Gox users in 2014 were REALLY REALLY REALLY into crypto. These owners owned crypto before ANYONE cared about it. These are power users. These are evangelists. These are people who know WAY more about crypto than you do. Thinking that they will give up on crypto now is a little misguided. That said, NONE of these users care about Bitcoin Cash. The BCH fork happened in 2017, after Mt Gox filed for bankruptcy. I think it’s safe to assume that almost all of the recovered BCH will be sold, but I don’t think that will greatly impact the overall market.

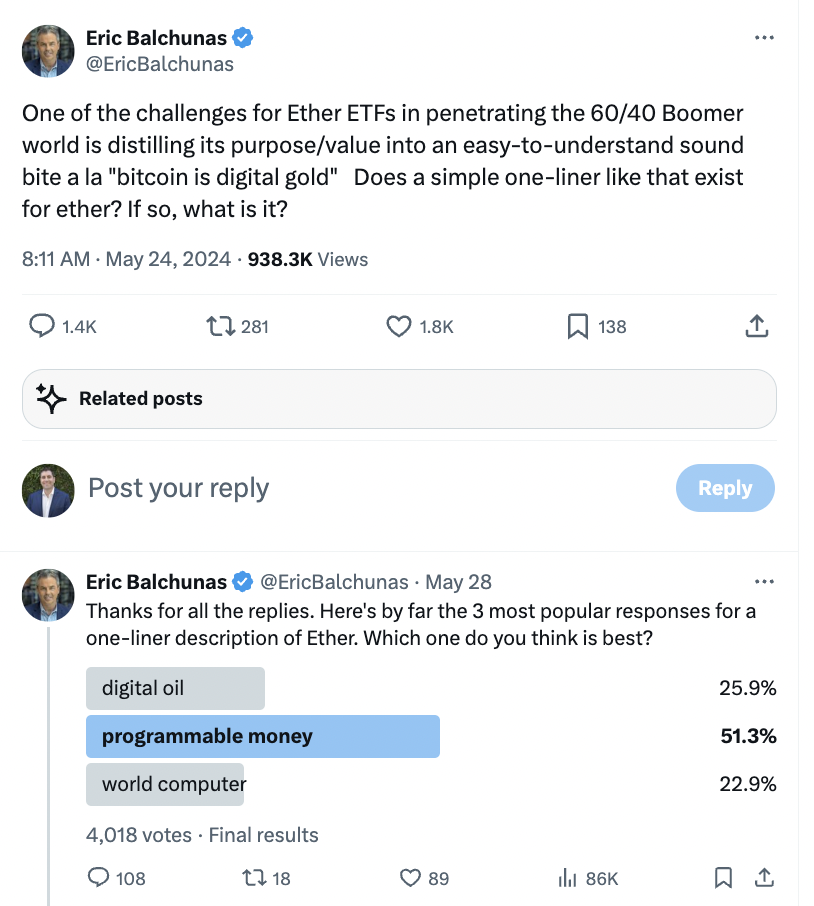

The ETH ETF

All eyes are on the upcoming ETH ETFs after the SEC approved the issuance last week, and S-1 filings have begun. Of course, the question remains, “Will there be demand for this product?” So, let’s break it down.

Let's compare the total assets under management (AUM) for the Grayscale Ethereum Trust (ETHE) from the beginning of the year at $7.3 billion to the Grayscale Bitcoin Trust (GBTC) at $28.9 billion before U.S. spot bitcoin ETFs were approved). That ratio is roughly 25%.

The Bitcoin ETFs witnessed roughly $13 billion inflows over the first 6 weeks. Assuming ETH experiences roughly 25%, you’d be looking at roughly $3 billion in inflows. Is this reasonable? Well, it depends.

Arca has been loud, vocal, and adamant

about our thoughts. And if marketed correctly, we believe ETH will have more demand over time than Bitcoin. Because EVERY investor cares about technology, whereas very few care about gold. From our blog:

“ETH has been categorized in a variety of ways, from “ultrasound money” for its supply burn mechanism to the “internet bond” for its non-inflationary staking yield to a “Supercomputer”. With the expansion of L2s and restaking, narratives like “settlement layer asset” or a more esoteric “universal objective work token” have also come to light. But ultimately, we don’t think these characterizations can holistically capture ETH’s dynamism on their own. In fact, we believe the increasing complexity around ETH’s use cases has made it difficult to define singular metrics of value capture. Instead, the confluence of these narratives may even appear negative as they can detract from each other – distracting market players from the token’s positive drivers.

These terms do not resonate with investors. At all. It is confusing at best, and inaccurate at worst. The analogy that makes the most sense is that Ethereum (and all smart contract protocols) are App Stores. Like any app store, upon launch, it is a blank canvas with some speculative value based on what could one day be built inside, but the true value comes over time as new apps are built and launched. Your phone has banking apps, games, maps, and much more. Similarly, Ethereum has banking apps (DeFi), gaming apps (Axie, Illuvium, etc), NFTs, maps (DePin) and much more. As these apps get used and interact with each other, ETH is your “Apple Pay”, and the transactions that occur drive transaction revenue back to the app store (Ethereum). Any investor would happily invest directly into the Apple app store if it were a separate, publicly traded entity. Investors understand how Apple generates revenue from the listing and usage of apps. The same is true for Ethereum. And if Ethereum is Apple IOS, then Solana is Android.”

Regardless, the idea that ETH ETF inflows must be at least ¼ of BTC ETF inflows is flawed. Bitcoin is still run by miners who control the supply. That supply (or inflation) schedule is fixed, and this selling pressure is constant. To offset this supply, constant buying pressure is needed (via an ETF creation or elsewhere).

But Ethereum works differently. Ethereum supply is not constant, and in fact, during high periods of blockchain economic activity,

Ethereum is often deflationary. Said another way, it takes much less demand to keep the price of ETH constant, and ANY new demand function will have a big impact on price. Even if the ETH ETF flows are a 1/10 of BTC, it will have an even greater impact on price than BTC ETFs. The BTC price rose +75% upon the ETF announcement and subsequent flows.

Updates from Singapore

“I just wrapped up an incredibly successful week in Singapore, where I met with several allocators, founders, custodians, exchanges, and sovereigns in the digital assets and blockchain spaces. I learned a great deal about how Singapore views the crypto world, and what projects various institutions are engaged with. Settlement is top of mind and coalition building is how you achieve the desired results.

One thing that surprised me was how the mindset of Singaporean regulators has shifted since 2019/2020 regarding the establishment of Family offices in Singapore. Back then, families from China and India could easily set up a family office, in many instances, in just a matter of weeks or a month.

There was a major trend of such vehicles being set up, particularly as investors and family office wealth managers preferred leaving Hong Kong as their primary residence and jurisdiction for various reasons.

As of April 2024, the application process to establish a family office in Singapore can now take up to 18 months, and opening a private bank account can take 3–6 months. While some will tell you that this is due to a backlog of applications, the reality is that the regulator has imposed stricter regulations due to concerns about money laundering and a lack of oversight that can often lead to financial turmoil. Whereas the minimum AUM was previously $500,000 or so, I am told that The Monetary Authority of Singapore (MAS) has now imposed a minimum limit of $20 million in AUM. Further, there is a greater due diligence effort as to whom is managing a family office, their backgrounds and whether or not they are qualified to be in such a position.

This has led to fewer attempts by wealthy families, particularly from China and India, to set up bases in Singapore.

In nearby Hong Kong, family offices are still concerned about being under the oversight and grip of China to a certain extent. And, while some Chinese officials were reportedly approving Hong Kong’s pro-crypto efforts in early 2023, perhaps using it as a test bed or launching pad for crypto so long as it did not threaten the country’s financial stability, folks in Singapore consistently encouraged me to look deeper as I assessed which jurisdiction would ultimately win the battle for family offices and capital inflows - and, ultimately, the crypto race. Namely, they said, the Hong Kong Securities & Futures Commission has compulsory insurance/comp arrangement requirements to help protect clients and a 98% cold storage wallet requirement that licensed corporations must comply with. That naturally impedes upon a family office’s ability to trade in and out of positions in the space at a lightning pace.

Where will the money go?”