Source: TradingView, CNBC, Bloomberg, Messari

What Does a Winner Look Like?

Written by Nick Hotz, Analyst

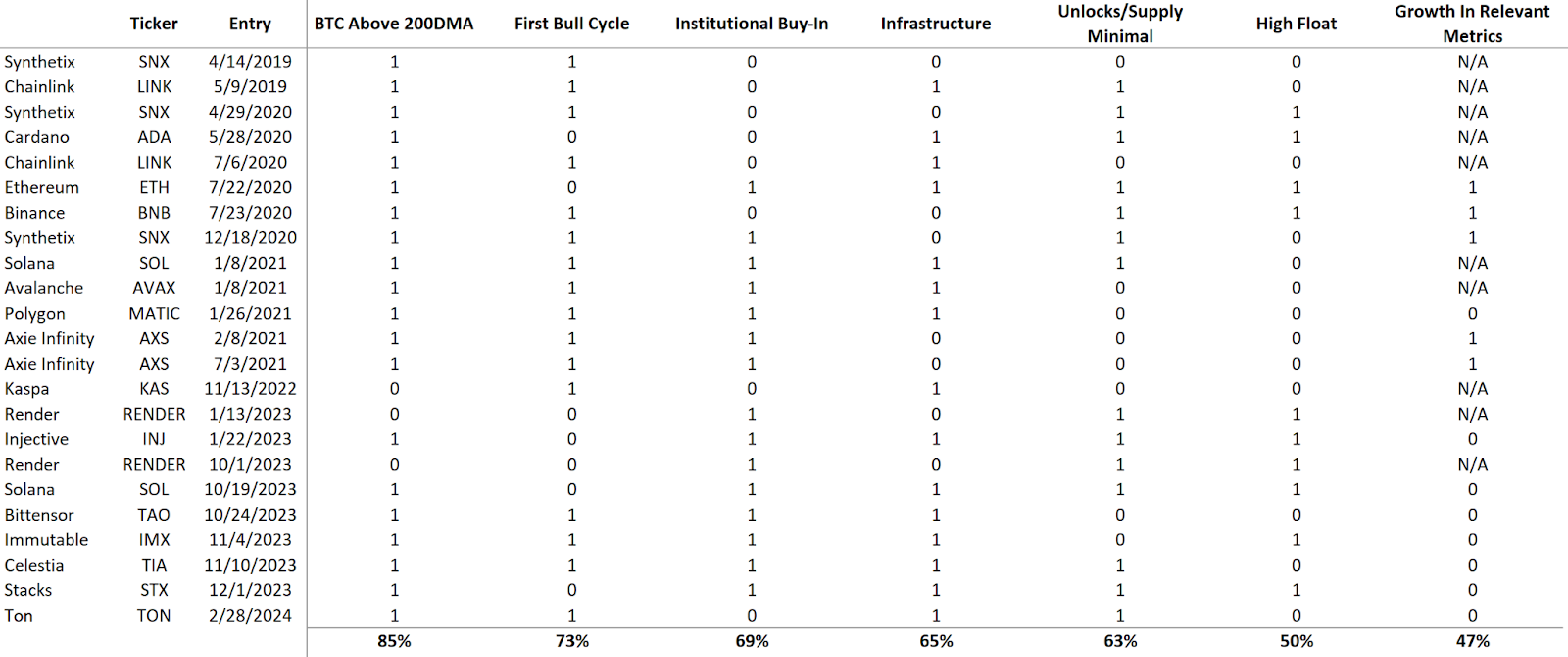

We analyzed several leading tokens from the past that outperformed the broader market, increasing by at least 100% in a minimum of 100 days, and concluding their run in the top 50 by market cap. Here are a few characteristics to look for to spot these types of tokens before their winning run.

Sources: Arca Internal Research, Messari, Artemis, Token Terminal, DeFi Llama, Coingecko, TokenUnlocks

- Market Health – Big winners tended to emerge in strong market environments. 85% of tokens started their run while Bitcoin exceeded its 200-day moving average.

- New Tokens – Historically, 73% of winners never had a big run previously. However, this has not held true since 2023, when only 4 of 9 winners were on their first bull market.

- Institutional Buy-In – Despite a prevailing negative attitude towards crypto VCs on Twitter, monitoring where top VCs invest has been a good starting place if you want to pick winners. 67% of tokens since 2019 and 88% since 2021 were funded or backed vocally by some of the biggest VCs in the space before their subsequent runs.

- Infrastructure—65% of the analyzed tokens were predominantly focused on blockchain infrastructure. Perhaps this is a sign of the space's infancy, or maybe it’s just “base rates” (most larger tokens are infrastructure-related).

- Reasonable Supply/Unlocks – The median token had 1Y forward inflation of 23%, with 63% of tokens having a circulating supply inflation of less than 25%.

- Float Mostly Didn’t Matter – In the heat of a bear market in the long tail of tokens, sentiment around low float/high FDV tokens is incredibly low. Historically, though, the float doesn’t seem very predictive. 50% of tokens had floated over 50% of 10Y forward diluted supply, while 23% were under 25%. However, none of the tokens studied had less than 15% floats, so caution is warranted in extreme cases

- Metric Growth Wasn’t Predictive – Only 47% of winners with historical data had noticeable increases in commonly tracked metrics like TVL, fees, and active users prior to their run. Additionally, nearly half had no metrics available at the time, and most of the tokens where metrics were growing ahead of time were in 2020 and early 2021 when data access in crypto was limited at best. However, almost all winners had fundamental metrics grow during their run.

A Battle Royale Over Stablecoin Dominance

Written by Michal Benedykcinski, VP of Research

Tether recently announced a whopping financial results (

over $5 billion in profit with less than 100 employees). This propelled many of the existing market participants across TradFi, Fintech, and DeFi to publicly announce their own stablecoin aspirations. While Tether and Circle hold the controlling 90% share of total stablecoin supply today, many new entrants continue to look to replicate the success of USDT and USDC and expand the market, which has benefited greatly from the high interest rate environment.

Outside of the competitive forces in the market, significant regulatory headwinds still create obstacles for both Circle and Tether. Markets in Crypto-Assets (MiCA) regulation in the EU, in its current form, is constricting issuers from pocketing interest of any kind, including discounts and bonuses, which makes both USDT and USDC non-compliant. Hence, many trading pairs have already been delisted for the European user base. This created a further opening for new entrants like

Banking Circle, which launched a Euro-backed and MiCA-compliant stablecoin this week. While Euro-pegged stablecoins comprise a drop in the bucket of all stablecoins in circulation, they are expected to grow to $15 billion by next year giving popular eurodollar stablecoins a run for their money.

In the US, we have seen some TradFi players like Cantor Fitzgerald’s CEO Howard Lutnick

extolling the virtues of stablecoins while coming out as the official custodian of Treasuries and commercial paper backing USDT. Fintech giant PayPal has also thrown its hat into the ring with a gradual stablecoin roll-out (PYUSD) across 36 million merchant accounts. While it’s been slow on the uptick since announcing PYUSD over a year ago, some of the commercial potential applications, including discounts passed onto consumers when checking out with a stablecoin, could prove extremely attractive for both merchants and retail buyers.

Finally, synthetic stablecoins like algorithmic Ethena or, most recently, rebranded over-collateralized

MakerDAO’s Sky continue to be a popular default solution for native decentralized finance projects. While it might pale in comparison to results Tether has posted, the attractiveness of yield on USDe and DAI omnipresence in DeFi legos solidifies their lead as seen in the fees posted by those alternative stablecoin issuers. Results are even more impressive when you consider the respective product launch dates (USDe from Ethena - February 2024; USDC from Circle - May 2018; Dai/Sky from MakerDAO - December 2017; and USDT from Tether - October 2014).

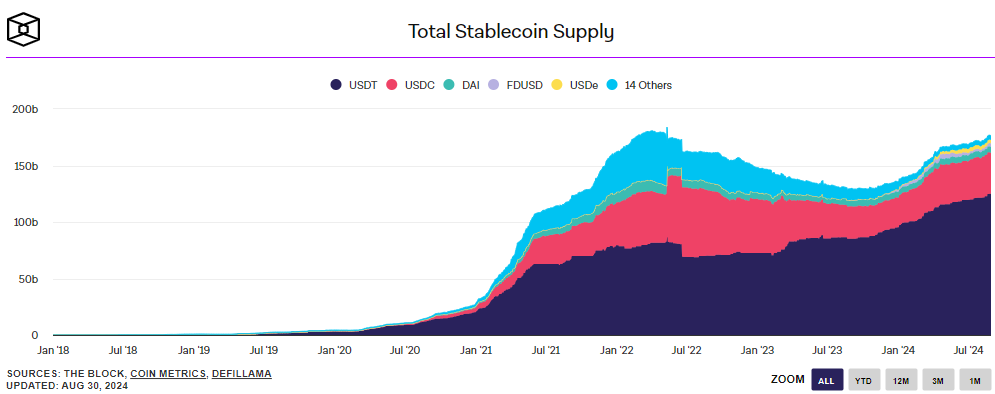

Source: TokenTerminal

Stablecoin growth continues, and it shows no signs of slowing down, driven largely by the product market fit it found within digital assets capital markets (as a popular trading pair), FX storage of value reserve (specifically within emerging markets of South America, Africa and Asia) and finally a better mode of payment (faster and near instant settlement). The once seemingly outlandish projections made by Bernstein analysts a year ago estimating

stablecoins to reach $2.8 trillion dollars by 2028 might prove too conservative, with a potential growth flywheel between platforms of TradFi, Fintech and DeFi issuers.

The Future of Ethereum is Coinbase; the Future of Crypto is Solana

Written by Joey Reinberg, Trade Operations Associate

The future of Ethereum appears increasingly tied to Coinbase, while Solana is rapidly emerging as the frontrunner in the broader smart contract platform (layer one) landscape. Once the undisputed leader in smart contract platforms, Ethereum is currently struggling with low market sentiment and underperformance in price.

![]() Source: TradingView

Source: TradingView

In contrast, Solana has experienced positive sentiment all year and is consistently outperforming most other Layer-1 blockchains in terms of price. A significant factor in Solana's success is its integrated approach to providing developers with a low-cost environment to launch apps on a singular chain. This has led to the proliferation of DePin projects with "utility tokens" that not only have value accrual mechanisms but also align well with the current regulatory structure in the United States. For instance, Helium is a prime example of a decentralized network that leverages utility tokens to incentivize users to build and maintain wireless infrastructure. This model of tokenomics is particularly appealing in the current regulatory environment, as it avoids many of the pitfalls associated with tokens that might be classified as securities. Additionally, these DePin tokens provide more long-term utility because they are used by network participants rather than just governing a decentralized protocol, like many current DeFi tokens.

Ethereum’s scaling strategy, while essential for growing an L1 that can’t handle sufficient usage and has high fees, is becoming a double-edged sword. The fragmentation of liquidity and applications is parasitic to Ethereum. Instead of strengthening Ethereum, this approach dilutes and fragments the Ethereum ecosystem across hundreds of chains without a unifying interoperability standard.

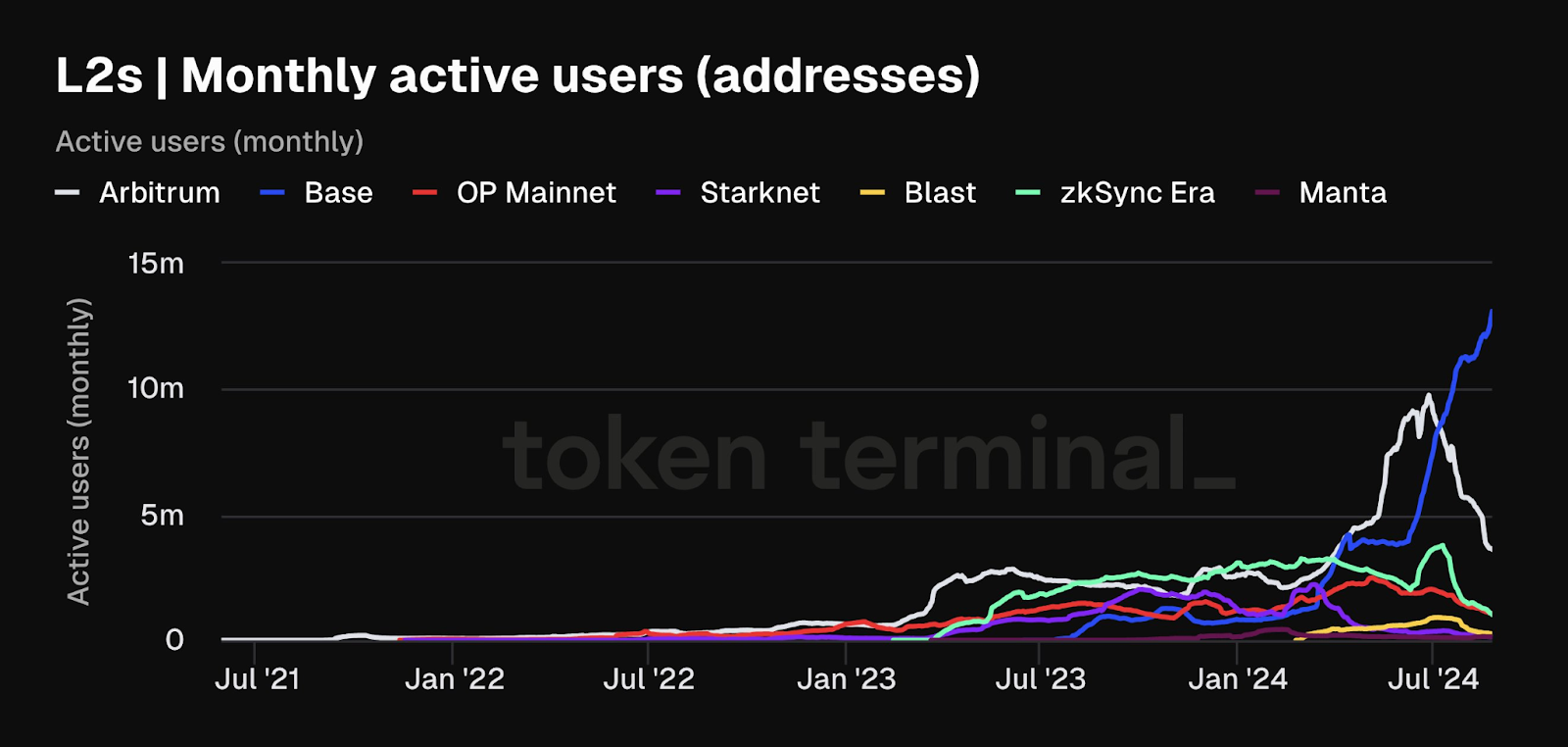

Coinbase released Base earlier this year, and while Base is not currently leading the Layer-2 race in terms of TVL, it is leading the Layer-2 race regarding users and builders.

Source: TokenTerminal

Almost all L2s are essentially the same product. What differentiates them is the community and integrations the protocol provides to builders. Base makes it easier for developers to build apps by offering seamless integration with Coinbase’s products, users, and tools. With access to 110 million verified users and over $100 billion in assets, developers can leverage Coinbase’s extensive ecosystem to gain a significant advantage over building on other Layer-2s. Features like gasless transactions, easy-to-use APIs for account abstraction, smart-wallet (passkey) integration, and simple asset bridges are designed to foster thriving applications rather than promoting its own Layer-2 governance token.

Source: TokenTerminal

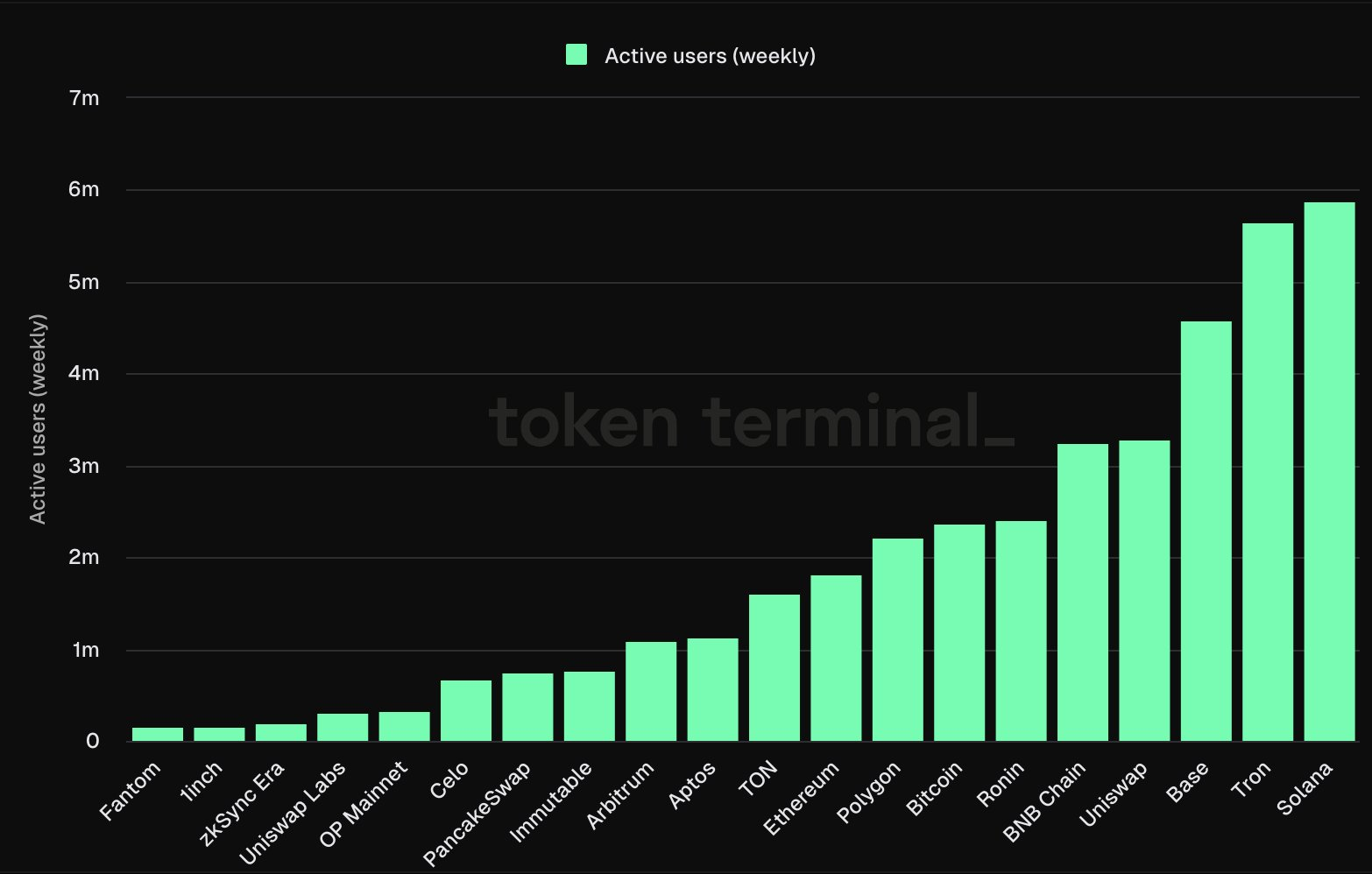

On the other hand, Solana has adopted a more holistic and integrated approach to blockchain development. This integrated approach allows for a seamless and efficient ecosystem that supports a wide range of applications all on the Layer-1 itself. Unlike Ethereum’s fragmented Layer-2 ecosystem, Solana’s cohesive environment is better suited to the needs of developers and users alike. At the end of the day, all that really matters is how many people (or AI agents soon) are using a blockchain, and Solana and Base continue to dominate in terms of active users.

Crypto Should Be Non-Partisan

Written by Wes Hansen, Managing Director, Trading Operations

To anyone who spends every day in the digital assets space, it might feel like the November U.S. presidential election has completely taken over the mindshare of this industry. You cannot even log into crypto Twitter without being inundated by the (often) inane thoughts of everyone who believes they have something meaningful to contribute. But what might be different this time is that people outside digital assets also sense this push. That’s because corporations in the digital assets industry account for about half of all corporate contributions to political action committees (PACs) this election year.

Entities in the crypto industry are spending more money than any other industry when viewed solely by the political contributions of corporations (there are some wealthy individual donors who put everyone to shame in the amount of money they throw at elections to buy their way into power and influence).

While it’s fantastic for digital assets to continue to drive towards being viewed more positively, it is concerning in terms of the orchestration and results of this push. It’s very clear that the current presidential administration couldn’t care less about digital assets, and many feel this is due to the Elizabeth Warren agenda. Whatever her game plan is, it’s been a horrific 4 years for crypto. Warren, with the SEC by her side, has been on the warpath for far too long. This industry needs more oversight and better regulation, but the “regulation by enforcement” approach has hurt innovation in America. We have always led, but we’re now falling behind. The Democratic Party is now suddenly known as the party that does not want to move forward, does not support progress, and does not want to see American exceptionalism continue. This is not just a result of the party’s approach to digital assets but to all types of innovation, whether technological or not.

Hopefully, the Democratic Party can right the ship. There are many in crypto who do not want to take sides, but just want digital assets to thrive. Crypto should not be a partisan issue. Digital assets should transcend parties because this is about moving forward as people and building a better future. If you believe digital assets can help improve the world, then you should not be rooting for one side over the other; you should be rooting for crypto to bring both sides together for a common goal.