What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

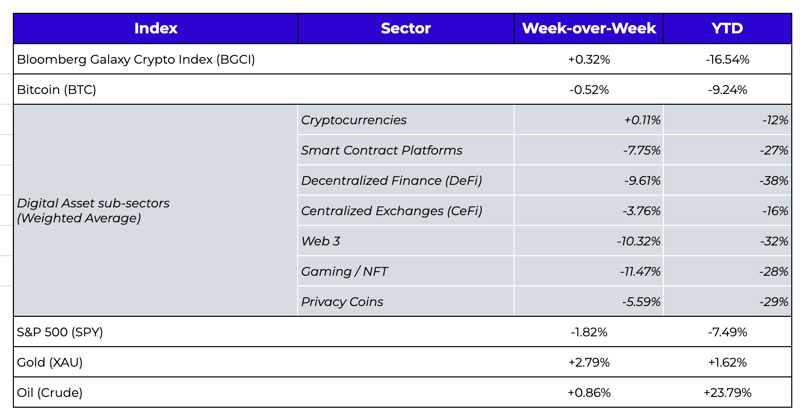

Week-over-Week Price Changes (as of Sunday, 2/13/21)

Source: TradingView, CNBC, Bloomberg, Messari

War, Rates, Bitcoin and Digital Assets

Last week was pretty awful for the broader digital assets market, as just about every ounce of strength was immediately sold into, with low liquidity aiding further to broad-based double-digit losses. The exception was Bitcoin, which showed both absolute and relative strength. We’ve been on record many times stating that Bitcoin has none of the characteristics of a defensive asset (no yield, no cash flows, no intrinsic value), and have suggested that it would make much more sense if cash-flow producing tokens with low customer turnover (like Ethereum, DEXs, and gaming) acted as the defensive “healthcare and utilities” sectors of digital assets. Nonetheless, it is not that surprising to see Bitcoin shine (relatively) amidst the geopolitical and macro backdrop. Bitcoin is now -9% YTD, which actually makes it one of the better assets to own this year other than anything related to energy, financials, gold, and a select few tech behemoths. The reality is that so many of today’s top digital asset projects are less than four years old, so we have no historical context for how Layer 1 protocols, gaming, DeFi, and Web 3 tokens should behave with a possible war looming and a 40-year high in inflation. Long-term, these factors are great reasons to own digital assets, as they shield investors from the monolithic actions of central banks and governments, but short-term, it’s a bit of a guessing game.

That said, for Bitcoin, we do have some clues. While Bitcoin rarely reacts in the same fashion twice, it has occasionally traded as a risk-off asset during periods of high geopolitical tension. For example, during the Iran missile attack in January 2020, Bitcoin traded up in line with gold and Treasuries. Should that happen again on the heels of a potential Russian invasion of Ukraine, it could once again flip Bitcoin’s narrative upside down from today’s “it’s just a 24/7 levered VIX” to tomorrow’s “global safe-haven asset.”

For now, though, despite discouraging losses piling up for digital asset investors, we should at least be encouraged by the differentiation in price action. Arca has been an active and vocal leader in educating the masses about uniqueness of different digital assets, but it’s nice to see others starting to reiterate the same message. Recently, Fidelity Digital Assets wrote a research report separating Bitcoin from other digital assets; while this was very Bitcoin-centric, potentially because Fidelity still only offers Bitcoin services, it does advance the education process. We were encouraged further by Delphi Digital’s 2022 outlook, in which they joined Arca on its crusade to highlight the maturation of this asset class. They stated:

“Bitcoin and digital assets appear to be trading more like macro assets, in large part because the biggest tailwinds that propelled them to new highs over the last 18 months have strong crossovers with those driving traditional risk assets like equities. That said, investors should brace for a world where the sectors within crypto—BTC, ETH, DeFi, NFTs, L1/L2—start behaving more independently as correlations between different crypto sectors start to weaken. Fundamentals were almost a running joke in the early days of the crypto market. Now, we’ve reached a point where protocols generate significant value in wholly unique ways. Investors will begin to recognize this, the same way they recognized that stocks in different sectors will exhibit unique return patterns, and will be benchmarked accordingly (e.g. how a SaaS company’s revenue and cash flow are entirely different from a global retailer’s). In the coming years, crypto investing will be no different.

Broadly, there’s a growing divergence between ‘macro crypto’ and ‘web3 crypto.’ Macro crypto (think BTC) will continue to be impacted by key macro factors, whereas the impact on the broader crypto market will depend more on the type of asset or protocol and whether or not such events directly impact its value proposition. In other words, the success of these dapps and protocols will be determined more by adoption and usage activity rather than the same macro factors impacting BTC.

Part of this divergence narrative will be driven by ‘smart money’ that recognizes the potential for crypto’s outsized returns. The days of classifying everything as either Bitcoin or “something trying to be Bitcoin” are long gone. Investors will realize that, unlike traditional equity, most crypto assets are designed to be productive assets, and the use cases (or utility) of these assets varies by application or protocol. Sure, you can take a buy-and-hold approach, but in order to participate in many of these networks (or at minimum avoid dilution), you need to do something with the native asset that contributes to its success (such as staking or providing liquidity, for example). One of the big unlocks in crypto is greater capital efficiency, and smart investors will come to realize this.

That’s not to say macro factors won’t impact the broader crypto market. After all, we know rapid liquidity growth can be a strong tide that lifts all boats. Specific sectors and their underlying assets will stand to benefit from strong fundamentals, creating a ripe environment for active management if you know how to spot trends early.”

For now, the market awaits every Bitcoin and Nasdaq move for guidance, but it’s clear we’re headed towards a more mature market structure soon.

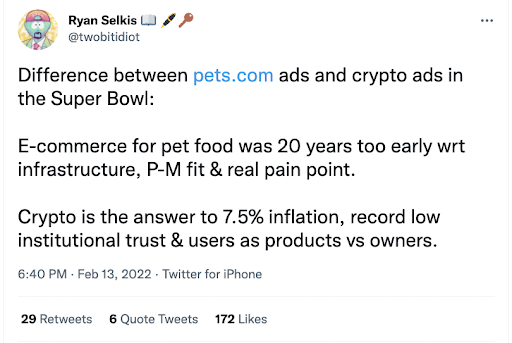

The Digital Asset Super Bowl Ads Were Brilliant

The boom in digital assets is often compared to the dot-com era. While this is typically used as a negative data point and can be dismissed easily given the actual user growth and traction of the products, it can also be viewed as a positive. Many of today’s most influential companies were built during the dot-com bubble, even if many individual projects were too early. More importantly, every company in the world is now a dot-com company, to the point where “dot-com” became a redundant misnomer and was eventually dropped.

Two of the largest digital asset companies, Coinbase and FTX, paid the outlandish costs required to secure a Super Bowl ad spot last night. FTX’s commercial basically said, “if you’re a naysayer about digital assets, you’re going to end up on the wrong side of history.” Coinbase’s bouncing QR code commercial suggested, “if you don’t understand where we’re headed with technology, you’re not our target customer.” The FTX commercial led to polarizing opinions from Larry David fans on his involvement, with some loving that he is now “one of us”, while others couldn’t believe he’d take a paycheck for something as “dumb as crypto.” Yet almost no one is debating the point of the commercial, which is that those who still deny the digital asset revolution are almost sure to continue to be flat out wrong, just like they have been thus far. Coinbase’s commercial was so popular it crashed their site as viewers rushed to scan the QR code. Moreover, for an industry that is characterized solely by speculation and trading, it’s noteworthy that 2 of the 3 largest companies in this space chose to spend millions of dollars to make broader points about the industry and the technology rather than try to capitalize on “get rich quick” retail customers.

Ultimately, I think we’ll look back on these ads fondly.

Bitfinex / LEO Case Study in Event-Driven Investing and Blockchain Forensics

The U.S. Department of Justice has seized 94,000 BTC, worth approximately $3.6B, that was stolen in a 2016 hack of Hong Kong-based digital assets exchange, Bitfinex. This is the largest financial seizure in the history of the DOJ. There’s a lot to digest here.

First, what a trade this was for holders of Bitfinex’s LEO token; it is now up 500% since being issued at $1.00 in 2019 and has gained over 55% in the last 30 days. The LEO token is not your typical “cryptocurrency”. In short, the LEO token was issued to plug a hole in Bitfinex’s balance sheet, which is why it had such favorable terms for investors. It was issued by a centralized company, it was issued under distressed conditions, it has an onerous amortization schedule based on cash flows of the business, it is completely transparent with regard to these buybacks, and most importantly, there was a clause in the white paper that said Bitfinex would have to buyback or tender for LEO tokens if the 2016 Bitfinex stolen BTC was ever recovered. Basically, it is the furthest thing from a “decentralized web3 application,” but that’s exactly what made this token such a beautiful, distressed, and special situations investment.

Second, speaking on the arrests made by the DOJ, the Deputy Attorney General, Lisa O. Monaco, said, “Today’s arrests, and the department’s largest financial seizure ever, show that cryptocurrency is not a safe haven for criminals.…Thanks to the meticulous work of law enforcement, the department once again showed how it can and will follow the money, no matter what form it takes.” What a statement this is! The second-largest seizure of cryptocurrency by the DOJ was back in November 2020 when the Department took over BTC, totaling more than $1 billion at the time. These seizures highlight the DOJ’s increasing capabilities when it comes to tracking illicit transactions through blockchain analytics, which undoubtedly dispels fears about the increasing use of cryptocurrencies on public blockchains making financial crimes harder for law enforcement to catch.

Let’s reiterate how important this is: while the media and members of the US government continue to perpetuate a narrative that Bitcoin is for criminals, those who are actually in law enforcement are stating the opposite. Matt Levine at Bloomberg summarized this succinctly:

“There is a strange debate about crypto and money laundering. Crypto skeptics will often say “Bitcoin is mostly useful for money laundering”; crypto proponents will occasionally say “what of it, money laundering is fine, freedom, man,” but mostly they will instead say “no, Bitcoin is useless for money laundering because it creates a permanent public record of all transactions and why would you want to launder money that way.”

You might think that a federal criminal indictment for $4.5 billion of Bitcoin money laundering would be vindication of the “Bitcoin is for money launderers” side, but I want to tell you: No it is not! What allegedly happened here is that hackers stole $4.5 billion of Bitcoin from a crypto exchange (and stealing from exchanges absolutely is a major function of crypto), and then they had a horrible time laundering it. They managed to extract only a relatively small portion of the money for actual spending, and each time they got money out the feds were able to trace it from the hack all the way to legitimate accounts with their names on it. The laundering efforts were small-scale, and they are also how they got caught.

If you rob a bank and steal a sack of money and the bills are sequentially numbered and a dye pack explodes in the sack and you drive directly to another bank and hand them the dye-stained sack and say “I’d like to make a deposit please” you will totally get arrested, and you will probably get charged with money laundering, but in no meaningful sense did you launder the money. It still has the dye on it! That is what happened here.”

One-by-one, the popular excuses used by many investors, governments, and individuals for why they refuse to allocate to digital assets just keep melting away:

- Digital assets are used by criminals: Nope, it’s a terrible asset for criminal behavior.

- There’s no intrinsic value and digital assets can’t be valued: Nope, today’s “Graham and Dodd” of digital assets are working hard to show off all of the different ways we can value different types of digital assets.

- Digital assets are too volatile: Nope, the recent 2- and 3-sigma moves in equities and rates would make even 2019 Bitmex users blush. Volatility is part of investing; it was just suppressed for 12 years by the Fed in certain asset classes.

Ultimately, each of these historical barriers to entry is being brought down. And once they are fully removed from the narrative, the sky's the limit with respect to the inflows of capital we expect to see.

What We’re Reading This Week