Source: TradingView, CNBC, Bloomberg, Messari

The Backdrop For A Significant Rally

I’ve

pounded the drum for almost 6 years about digital assets being completely uncorrelated to other major risk asset classes, and that any significant positive or negative correlations are always short-term and subject to change on a dime. And I still adhere to this. So maybe I’m the wrong messenger for this. But I’m even surprised by how much crypto lags behind the broad reversal rally. Perhaps it's best to explain this via charts.

Many “consensus” views were shaken in the past few weeks. The pain trades included short JPY, long big tech, and long “Trump wins” trades. All of these were crushed a few weeks ago, but all have bounced back completely.

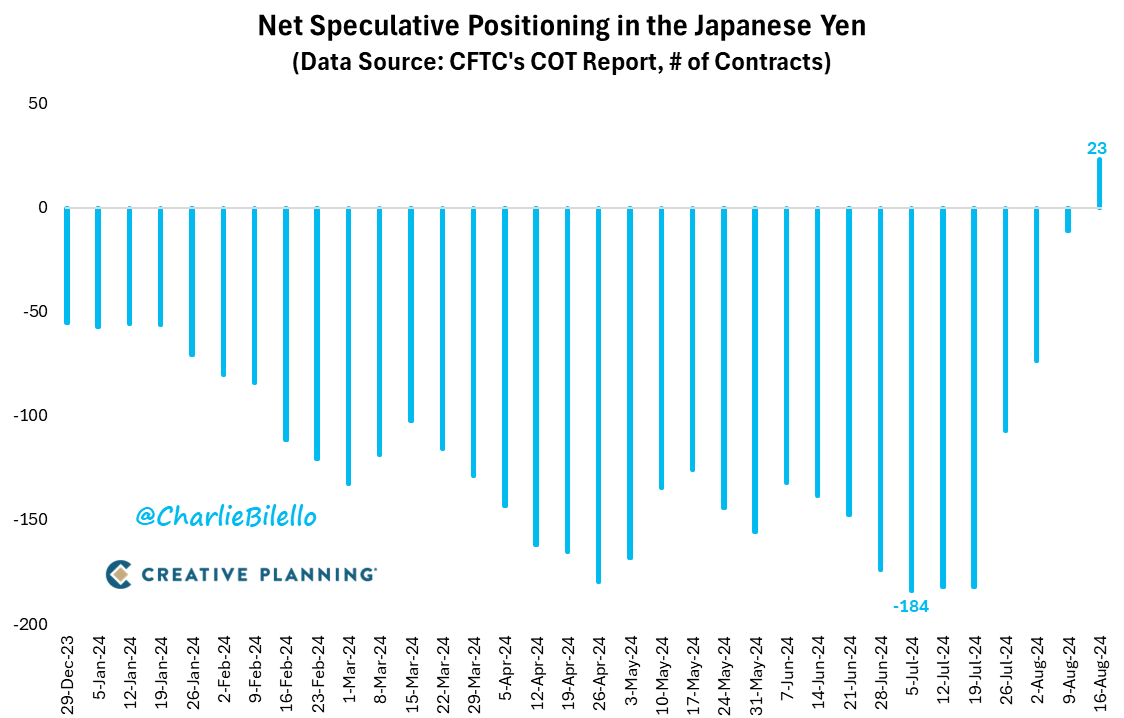

The short yen trade has completely unwound, with speculators moving from a record net short position in the Japanese Yen a month ago to a net long position today, signifying that most of the yen-carry trade is over.

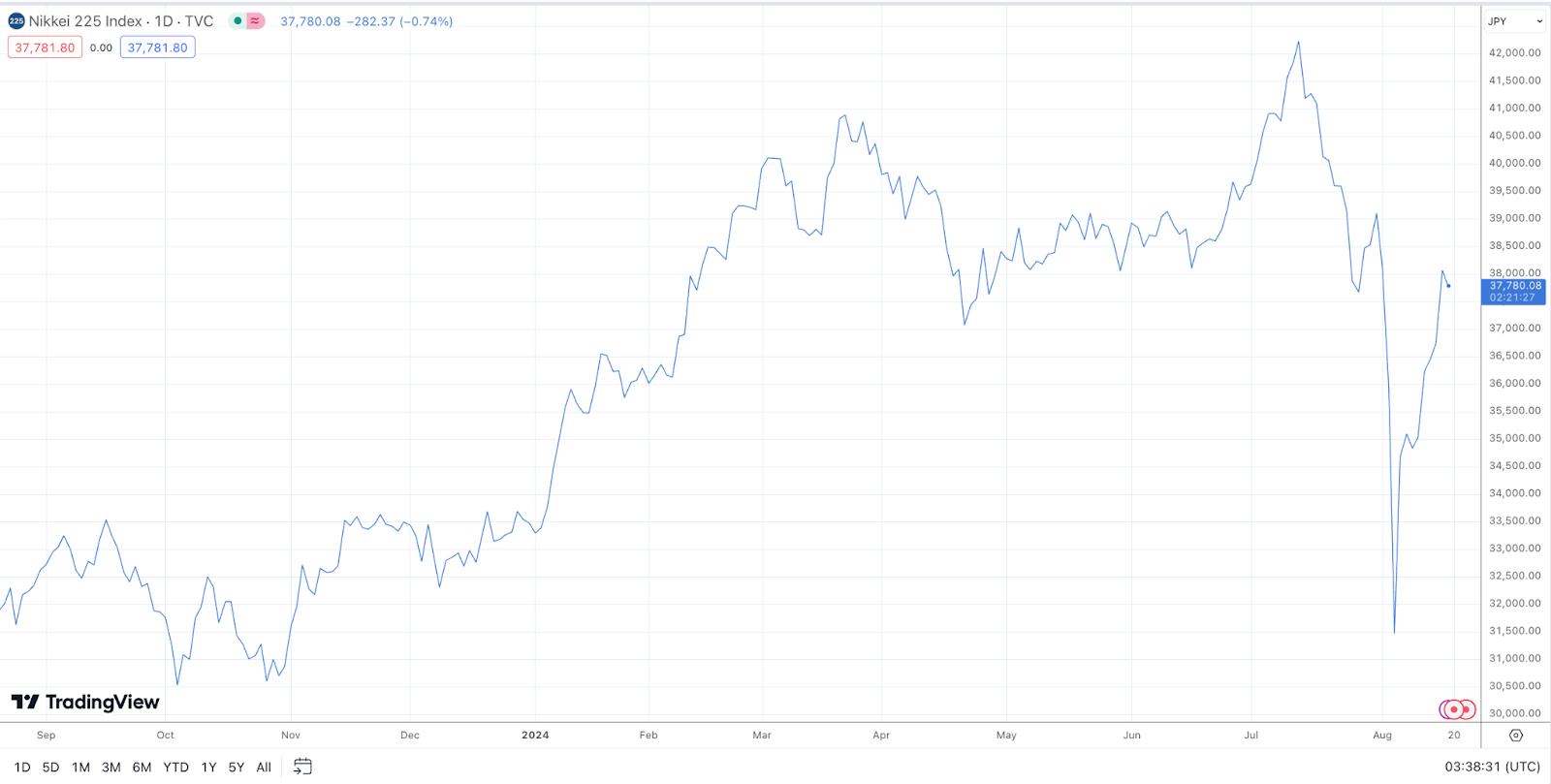

Yet, even without the carry trade, the Nikkei 225 index has bounced all the way back from the August 5th meltdown.

Source: TradingView

The VIX had traded above 65 prior to this month only twice – during the 2020 Pandemic and the 2008 Financial Crisis. I think we can all agree that August 5th was nothing close to those events, so it’s natural that the VIX has snapped back. But the 62% drop in the VIX over the last 9 trading days is the biggest volatility crash in history. No one has seen anything like this before because it’s never happened.

Source: SharePlanner

…. and speculators are betting on continued declines for the VIX from here.

Source: Bloomberg

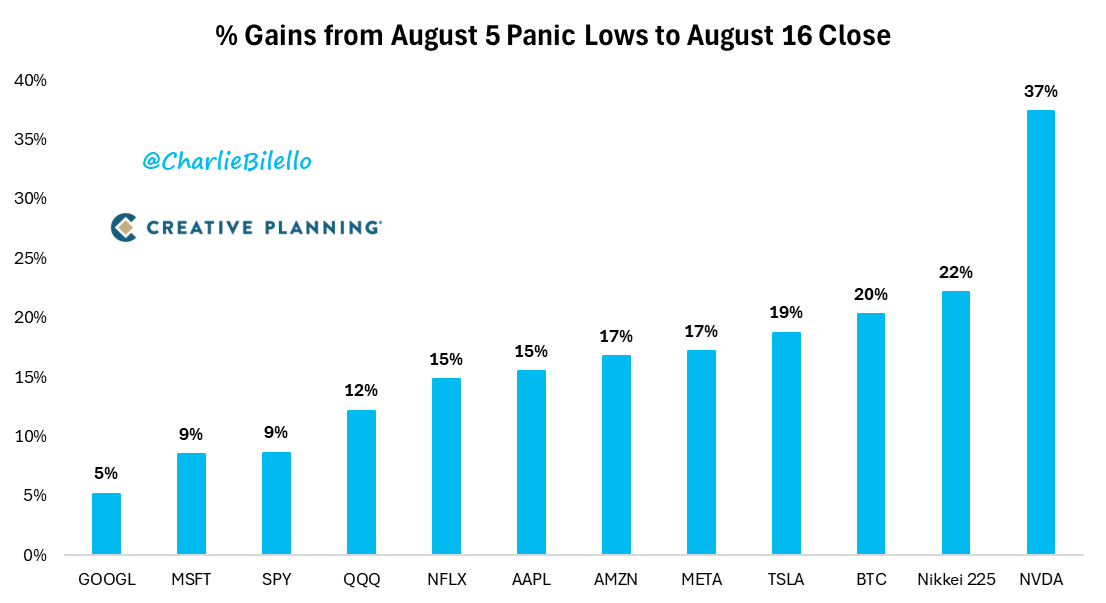

Meanwhile, U.S. equities have also roared back from the August 5th lows, led by the Magnificent 7 tech stocks.

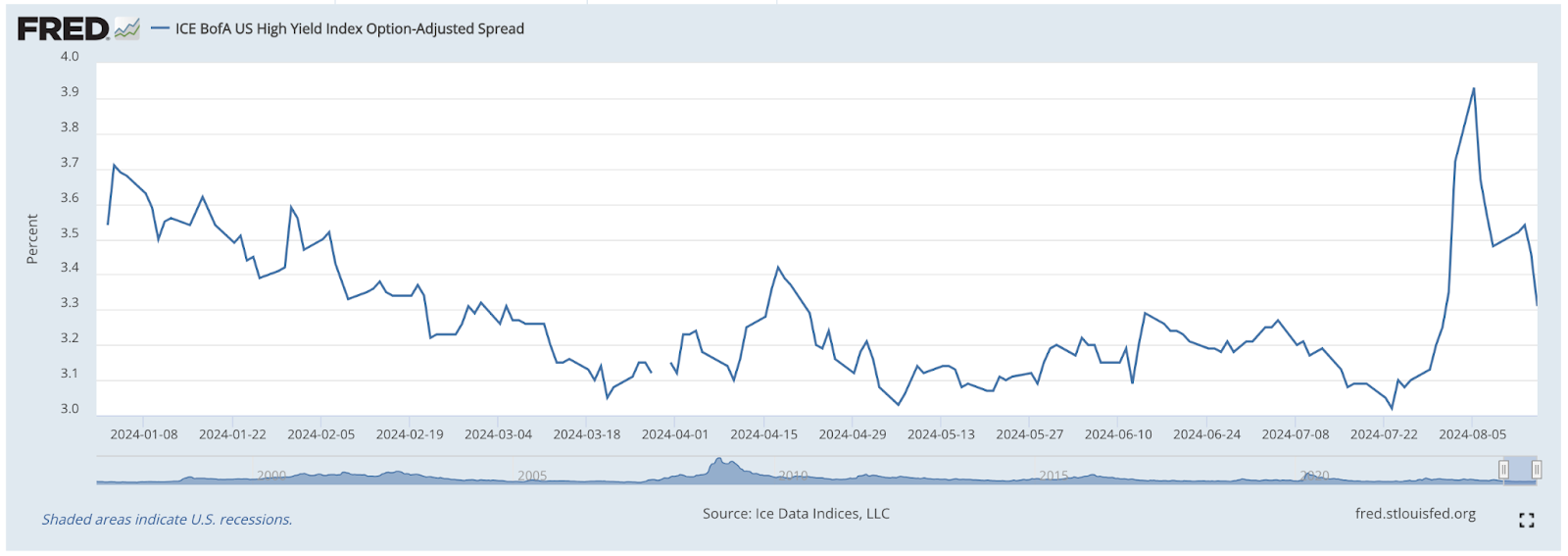

Even credit spreads, which are admittedly a bit of a laggard, have begun to erase the August 5th fear trade. There is simply no fear in the market exactly two weeks after we had max fear.

Credit spreads would probably be even tighter if not for the 10-year U.S. Treasury Yield declining 50 basis points, which keeps absolute corporate yields (US Treasury yields + credit spreads) at the recent lows.

Source: TradingView

All of these factors, combined with the upcoming U.S. Presidential election, suggest that the fear trade is gone, and risk assets are going to continue their ascent higher. Normally, this would mean that digital assets would be soaring higher as well since, at minimum, crypto tends to be the “fastest horse” in an “everything rally,” but also because this asset class has been so unnaturally beaten up recently due to short-term technical supply pressures that have now completely abated.

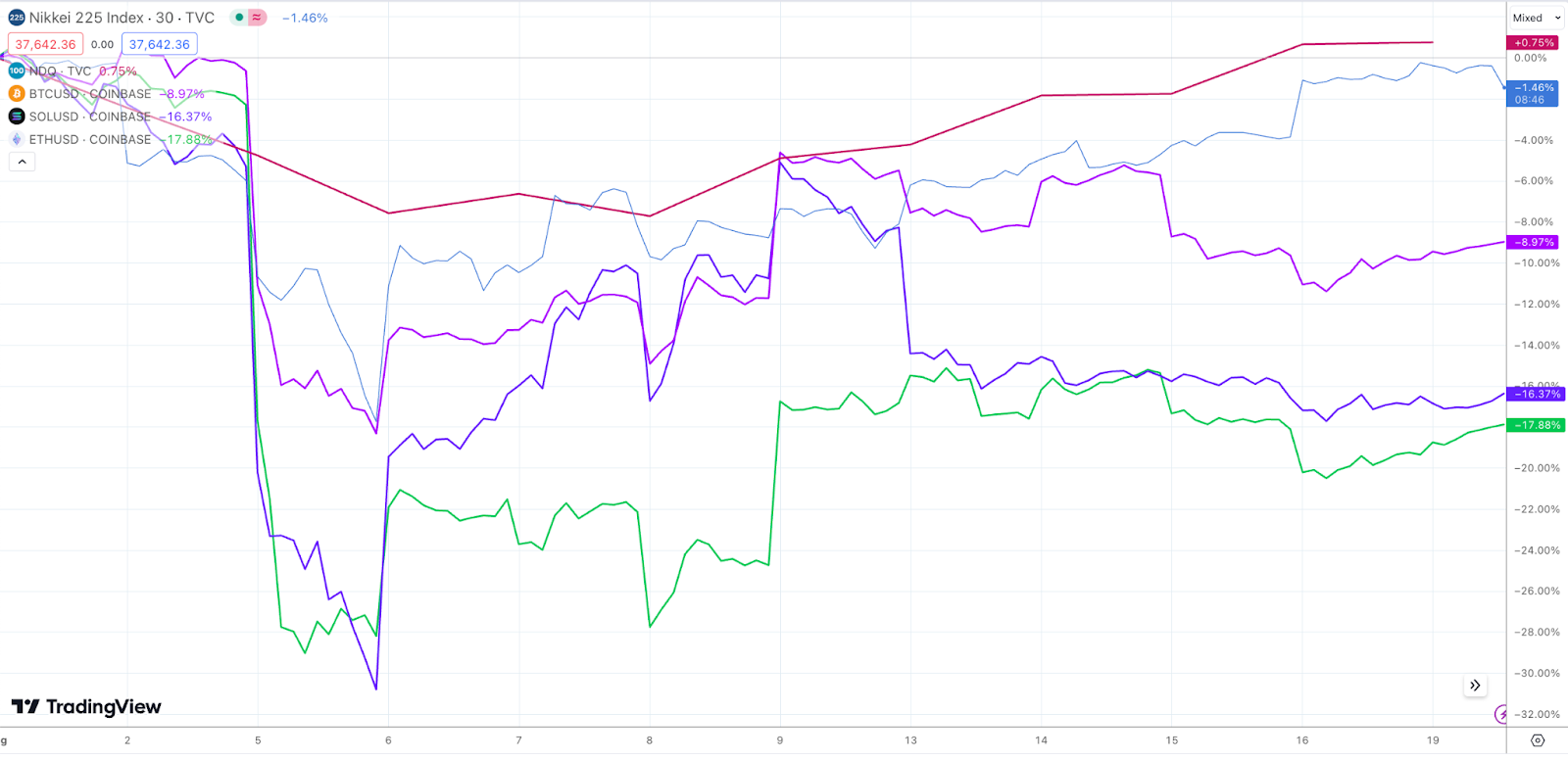

But crypto is just stuck at lower levels, with BTC (-9%), SOL (-17%) and ETH (-17%) down month-to-date despite the fact that the US and Japanese equity markets have fully re-traced.

Source: TradingView

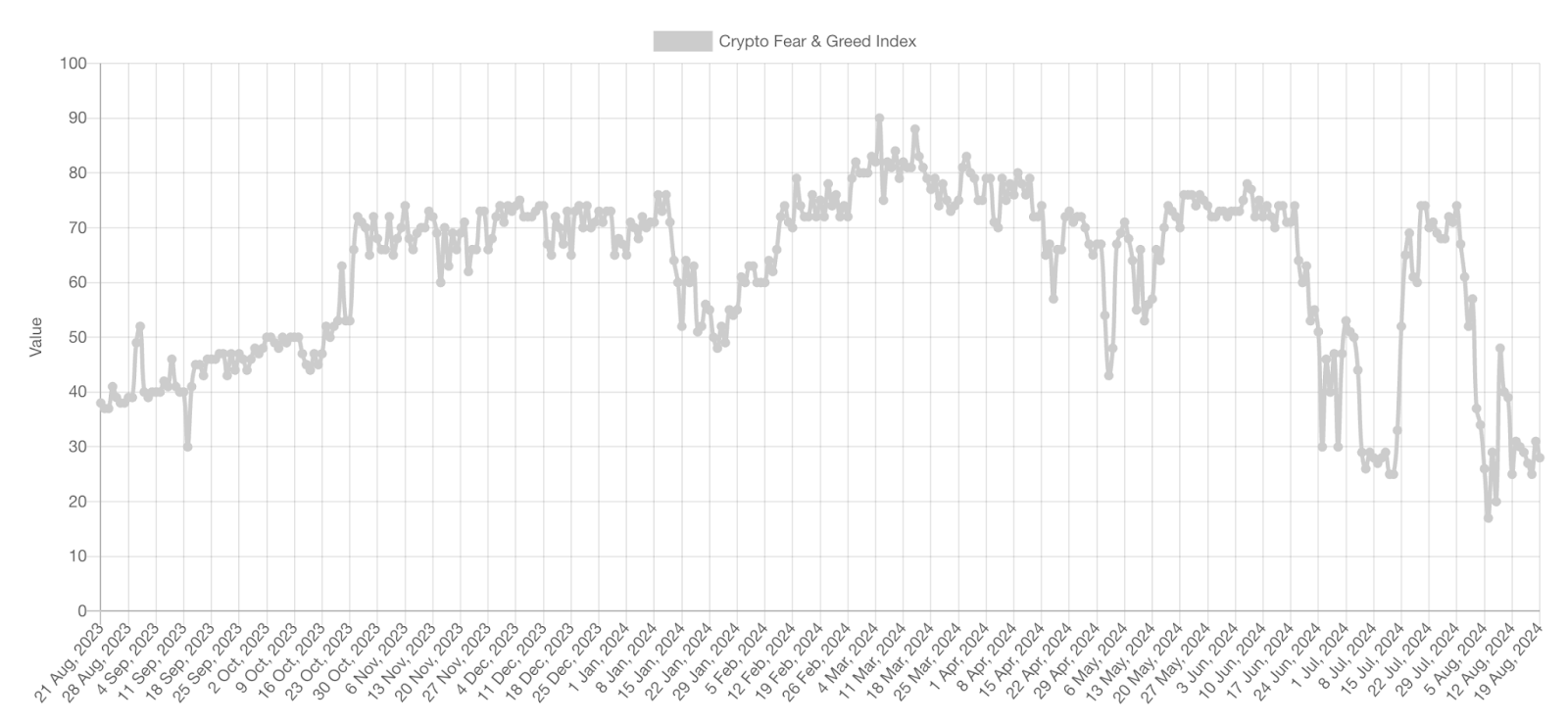

The VIX literally tells you there is nothing to fear right now, yet the Crypto Fear and Greed Index tells you to jump out of a window.

And Bitcoin is now having the worst post-halving performance on record even with the new BTC ETF demand.

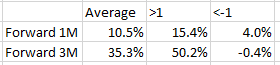

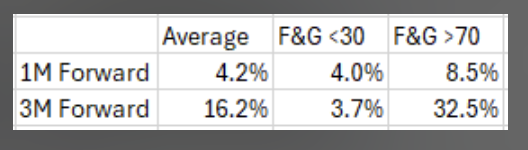

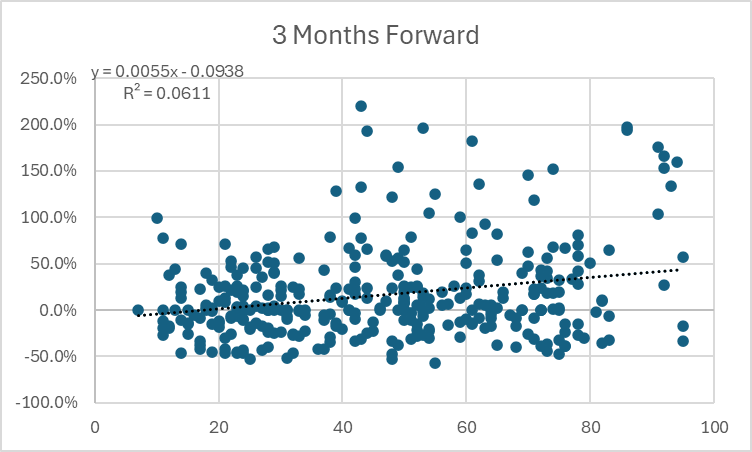

Common market sentiment and positioning measures, like the Fear and Greed index and open interest, have fallen to their lowest levels of the year. Funding rates are also sharply negative, indicating that shorts outweigh longs. Perhaps this is a bottom signal? Maybe, but our historical studies show that using these indicators have not been great contrarian buy signals. Forward 1- and 3-month returns are significantly higher than average when F&G is above 70 and well below average over the 3-month timeframe when F&G is below 30 as it is now. So maybe there is less of a chance of going lower when sentiment hits rock bottom, but we can’t necessarily assume the market will go higher.

Source: Arca Internal Calculations

Similarly, when Open Interest of futures contracts is 1 standard deviation above average over the last 100 days, returns are significantly higher than when OI is very low. So wiping out massive leverage over the last two weeks won’t be enough to send prices higher, either.

Source: Arca Internal Calculations

The crypto markets have very few speculative bets right now, and horrible sentiment, even as other markets are high-fiving on their way back to all-time highs. The positive news is being completely ignored, like the Ethereum ETF inflows (and lack of Grayscale outflows) and the fact that Morgan Stanley and its $5.7 trillion in client assets (the biggest of the wirehouses) are now

set to allow advisors to offer spot Bitcoin ETFs to some clients. Not to mention, crypto projects like Polymarket and Helium show real product market fit.

Quite frankly, either crypto is actually finally dead this time, or we're setting up for one of the biggest “rip your face off rallies” in history, just as everyone throws in the towel.