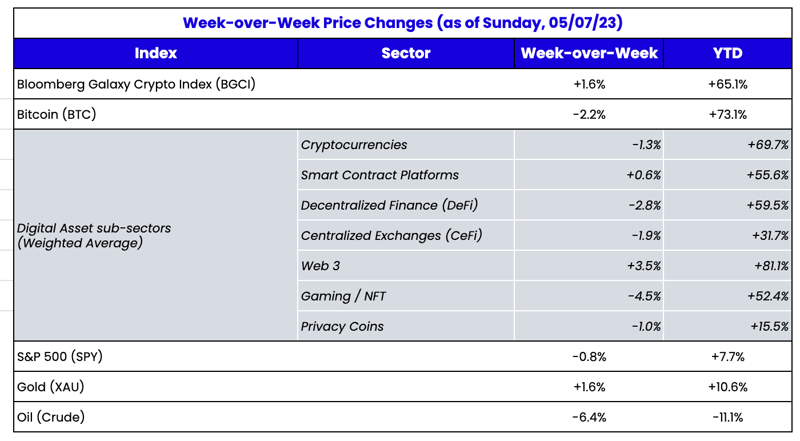

Source: TradingView, CNBC, Bloomberg, Messari

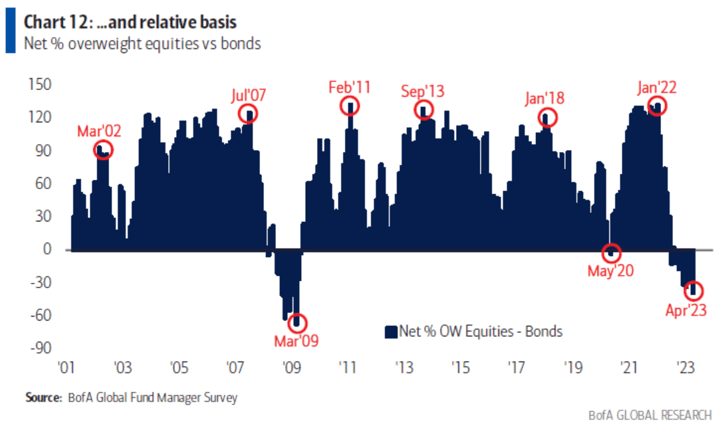

The Hypocrisy of Bank Equity OwnersThe 26th Annual Milken Institute Global Conference took place last week. While I did not attend, the consensus view on the macroeconomic landscape was profoundly negative based on written accords and anecdotal conversations with attendees. This view is also being expressed via investor positioning.

Source: Bank of America Research

And yet equities and digital assets continue to chug along, as the biggest fears about recession have yet to materialize. Digital assets were largely range-bound last week, with choppy trading sessions ultimately going nowhere. It seems the major digital assets are still buoyed by failing banks, but no longer moving higher on every failure.

While the economic data was plentiful last week, it took a backseat to banks yet again as First Republic Bank (FRC) became the second-largest bank failure in history (FRC entered FDIC receivership, was assumed by JP Morgan, and equity holders were wiped out). Bank stocks hit another YTD low, with the Regional Banking ETF (KRE) falling another 16% last week. At one point, it was down roughly 25% before rallying back. Jamie Dimon said we are nearing the end of bank failures, but I do not believe that is true. Deposits are still leaving banks in favor of higher-yielding money markets, and there are still roughly $600B+ of unrealized losses at banks versus now less than $100B in FDIC Insurance.

Unless Mr. Dimon personally spoke to millions of depositors and found out they’re happy earning below-market rates for increased risk, it seems implausible that we are anywhere near the end of this. As depositors flee, unrealized losses become realized losses, and the cost of funding skyrockets. Perhaps the fear of imminent failure has subsided a bit, but long-term failure is even more ominous. As Bloomberg’s Matt Levine put it, “This week the stock market noticed, not that the regional banks are failing, but that they are unprofitable, so their stocks went down.” Meaning bank stocks originally tanked in 2023 because many were failing suddenly and surprisingly. But now, they are simply unprofitable businesses even if they manage to limp along and avoid death.

Peeling back the onion a bit, bank equity is a complete fantasy. Over $100B worth of bank equity of now failed institutions has gone to $0 this year, and many hundreds of billions more have declined from still-solvent banks. As a result, the value of a bank stock is now:

Do you believe the CEO when he says “everything is fine” during a bank run plus temporary profits earned on phantom money that isn’t actually there when you need it?

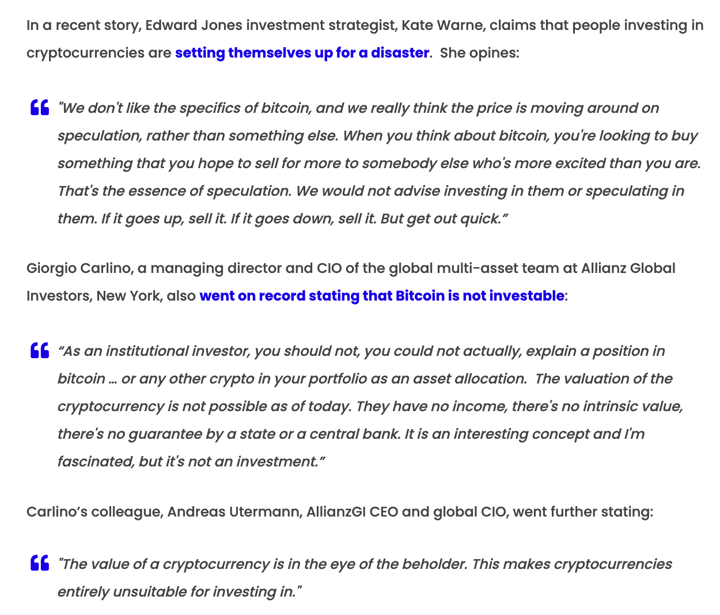

Bank stocks have zero intrinsic value. Their value is derived purely from a game of confidence. And that confidence has eroded. In July 2019, I wrote a response to numerous claims stating that bitcoin had no intrinsic value. Ironically, you can now replace “bitcoin” and “cryptocurrency” with “regional bank stocks” in every hypocritical, nonsensical quote from this article:

Financial stocks make up roughly 12% of the S&P 500; while financial stocks consist of more than just regional banks, the point is still clear—just about every investor owns some regional bank stocks (intentionally or via passive diversification). Every one of these investors should, as a hedge, if nothing else, own some Bitcoin.

In most industries if this sort of dynamic happened where there was a big hit to the stocks which didn't reflect a change in underlying fundamentals, there wouldn't be much impact on the business. It would keep doing its thing, and eventually the stock would simply reprice.

But banks are a very different sort of business. They are a confidence business more than anything. And big stock price declines are a problem for confidence.

At some point these declines *will be enough* to start to worry uninsured depositors who are paying attention.

And when that happens the fundamentals will deteriorate, which will further reinforce the equity market action. Shorts will get paid for being the very folks inducing the bank run.

That sounds a lot like an instrument with no intrinsic value. Perhaps those in glass houses who keep trying to undermine digital assets should avoid throwing rocks.

Where Are the Investment Bankers? Version 2.0

- The lack of regulatory clarity is keeping would-be (and should-be) issuers away from the market

- There are no investment bankers pitching token solutions

Here is what astute investment bankers would be doing right now: After a rocky Chapter 11 process, Voyager will liquidate its assets and return digital assets to long-suffering customers. This liquidation likely means an end to the $56M market cap of the VGX token. But VGX won’t ever really go away—there is no mechanism for a token to disappear. The debt and equity of Voyager will be swapped into new re-org equity through the bankruptcy process, but the token will live forever—even if it has no underlying company or reason to exist. VGX token holders will be looking for a new use case, a new narrative, or a new home for the orphaned token. Which introduces the question an investment banker should be asking: “Is it worth more than $56 million to some company to take over this token?” Essentially, the VGX token represents a customer and employee list because VGX tokens were given away to Voyageur customers and employees. Assuming 6,537 VGX holders (based on blockchain records) and a $100M tender offer for the tokens, this assumes roughly $15,300 per customer. Is acquiring 6,537 active crypto traders worth $15k/person to some entity? An investment banker should be thinking through an acquisition list and looking to help execute a merger/tender:

- Who has the liquidity to tender for this token?

- Who has a use case that aligns with the interests of VGX holders (crypto-native users, likely interested in yield-producing products)?

- Who has an existing customer base that doesn’t already overlap with VGX holders?

- Who is lagging the competitors and looking to grow their user base quickly?

A few targets emerge:

Centralized Companies

Fidelity just opened its crypto trading platform. They certainly have the capital to do this and a desire to find new customers.

Robinhood has had terrible publicity for the past 2 years and this could generate good publicity. They’re probably looking to re-grow their customer base, too—especially crypto-native customers.

Paypal & Venmo likely have the capital to do this and are looking for new customers to purchase crypto on their platforms.

Shopify / Amazon could buy VGX holders’ tokens in exchange for customers creating accounts and buying some products using crypto.

eToro is active in the crypto space but also offers traditional securities, which might be attractive to the VGX token holders that were burned by crypto.

Nexo has been quiet in the market recently and likely needs more customers. The spin could be, “We’ll buy your VGX tokens at a premium to market price in exchange for you depositing your fiat/USDC at Nexo and purchasing BTC or ETH, which you can then lend for interest or borrow against.”

Crypto-Native Projects, Decentralized Exchanges, Liquidity Protocols, and LSDs

Centrifuge, GoldFinch could attract VGX token holders who would be familiar with the offering and may be more comfortable with RWAs backing up their holdings. Both of these companies are looking for a lot more liquidity, too.

dYdX, GMX, Synthetix, etc. could capitalize on perp/derivative DEXs’ accelerated growth in retail popularity. Additionally, the foundations may be liquid enough to pull off an offer like this. The question is if they think VGX holders are already pretty active on their platforms—in which case it would be of no real benefit.

Lido could adopt a similar idea to the perp/derivative DEXs with the same risk.

Wallets

Frontier would definitely be interested in growing their user base; they’ve had good publicity recently and are making progress, and VGX holders may be interested in redeeming their tokens at a premium in exchange for creating a wallet and buying bitcoin.

One day, M&A ideas won’t come from a weekly crypto market recap but from investment bankers who recognize the value in tokens on a company’s cap table and the customer lists attached to them.