Source: TradingView, CNBC, Bloomberg, Messari

New Issues

A bad mix of macro data was published at the end of last week, as GDP came in light and the PCE index jumped. This stagflationary trend caused yields to jump and equities to fall. However, equities were able to erase losses to close the week driven by strong earnings, specifically from Microsoft and Google. The market is now pricing in just one interest rate cut this year compared to the eight predicted in January.

Digital assets didn’t bounce back and finished the week lower again, logging its 4th straight week of declines. Without earnings or any real crypto-specific data points, there is little to latch on to, though Republic First Bank (a small regional Philadelphia bank) was seized by regulators on Friday for issues similar to SVB. While this is significantly smaller than SVB and the regional bank failures of March 2023, it could potentially lead to a bid for Bitcoin. Both Microsoft and Google specifically cited their cloud demand was fueled by growth in AI, which led to a bid for AI tokens like RNDR, NEAR, and TAO, but even that bid was short-lived and quickly sold as crypto failed to keep up with equities.

Overall, the slow bleed is lower, with light volumes, muted interest, and a lack of catalysts, which has the crypto community again divided. Either this is the calm before the storm, and

wildly higher prices are not far behind using history as a guide. Or, this year’s strong performance is

fool’s gold, and prices will fall precipitously due to a lack of interest.

I’m in the former camp, but not because of history, charts or cycles. To me, it’s just looking more and more like a healthy market with more demand drivers than supply drivers, and any pullbacks are due to temporary buying strikes more so than heavy selling pressure.

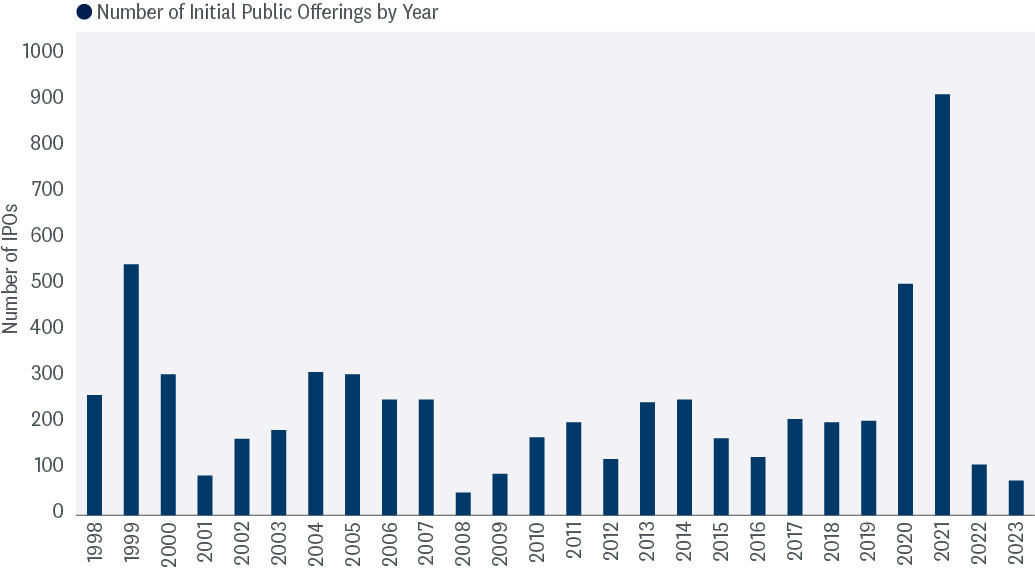

One area of particular interest is new issue supply. Recall that new issue volumes in the debt and equity markets typically track debt and equity prices. In other words, investment bankers typically bring more deals to stronger markets, while weaker markets tend to see less deal flow.

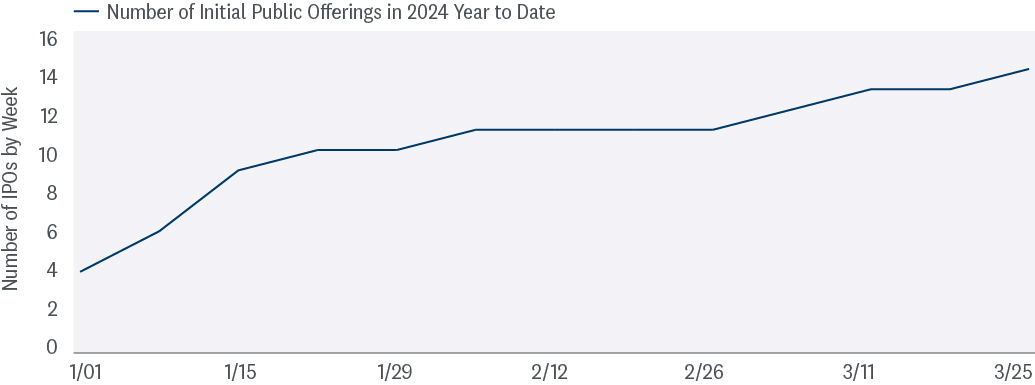

The recent increase in IPO activity YTD and generally positive price performance provide a favorable reading for this risk barometer. The number of IPOs continues to rise in early 2024.

Similarly, new issues are heating up in digital assets and can be seen as a major indicator of market strength. Through 4 months, we’ve already seen a massive increase in the supply of tokens. An estimated

$8.6 billion in additional liquid supply of tokens has been injected into the market YTD. And this is likely only the beginning, as many other projects have hinted at token generation events such as:

- Eigenlayer

- Kamino

- Friend Tech

- Drift

- Magic Eden

- LayerZero

- ZkSync

- Scroll

- Blast

- Zora

- Grass

This issuance is a double-edged sword. As mentioned above, it is a sign of strength in the market, and the supply can easily be absorbed by both inflows and cash on balance sheets should the market show even moderate levels of new interest.

On the other hand, there are a few short-term pitfalls. For starters, many crypto VCs are already feeling the heat for not distributing capital back to their LPs. They are likely selling tokens as soon as possible to lock in gains, return capital to LPs, and turn the fundraising spigots on for their next vintage. Second, the average float (circulating market cap divided by fully diluted capital) of these new tokens is only 14%, indicating a lot of future dilution – roughly $70 billion of locked tokens will come to market over the coming years from just this year’s new issues alone.

And finally, the process of bringing tokens to market continues to be massively flawed. The ICO market of 2017 was MUCH MUCH MUCH better, where tokens were being sold at fair prices based on actual demand, and new investors could feel early and engaged with projects and their future success. Today, with airdrops, direct listings, and pressure from a handful of VCs with too much control and influence over market makers and exchanges, these exchanges are being bullied into listing tokens at artificially high prices. Fair or not, exchanges are the de facto investment banks in this space, and if they don’t start pricing tokens to go up instead of down, it will turn off a lot of their customers. There’s a reason why debt and equity capital market bankers focus on the after-market performance of their new deals. If investors make money, they keep returning for more deals, and future stock and bond issuers will come to them if they have investors lined up.

Arca has analyzed hundreds of newly listed tokens, and the results aren’t overwhelmingly positive.

Source: Coingecko and Arca internal calculations

Perhaps crypto folks should take a look at decades of history and league tables before pricing yet another terrible deal destined to go straight down.

The Fight Against the SEC

Speaking of ICOs, or the lack thereof, the SEC’s heavy influence over digital assets continues. Still, we’re seeing more companies and enterprises fighting back instead of lying down. While Blackrock’s entrance into the digital assets space via the Bitcoin ETF was credited as the spark for the late-2023 / early-2024 rally, an equally and perhaps less discussed positive catalyst was the number of blows to the SEC delivered by crypto-native companies:

- U.S. District Judge Analisa Torres said last year that Ripple Labs did not violate federal securities law by selling its XRP token on public exchanges.

- Grayscale won a court order against the SEC last year, in which the SEC was deemed “arbitrary and capricious,” which many believe was why the BTC ETFs were finally approved.

- While the SEC got a big win versus Coinbase, the Coinbase Wallet triumph over the SEC allegations was a ‘giant win’ for DeFi, which led to Uniswap feeling more comfortable turning on a fee switch, and Uniswap’s lawyers are ready to fight against the SEC themselves.

Last week, Consensys joined the fight, no doubt influenced by the pioneers before them who have already entered the ring. In a

complaint filed last week in the District Court for the Northern District of Texas, Consensys is challenging the SEC in its approach to regulating ETH as a security. The lawsuit revealed that Consensys had received a

Wells notice from the SEC on April 10, indicating that the agency is preparing to bring charges against the company over its MetaMask wallet, which, as the regulator alleges, has acted as an unlicensed broker for facilitating securities transactions via the Swaps and Staking products.

Consensys founder Joe Lubin took to his

blog to explain that Consensys is suing the SEC to defend the Ethereum ecosystem. Consensys is an important part of the Ethereum ecosystem, so any legal developments here may impact the broader crypto industry and hopefully clarify (finally) whether or not ETH is a security (Hint: It’s not). Per Lubin:

“We took this step for two very basic reasons: (1) the SEC should not be allowed to arbitrarily expand its jurisdiction to include regulating the future of the internet; and (2) the SEC’s reckless approach is bringing chaos to developers, market participants, institutions, and nations who are building or already managing critical systems running on Ethereum, the world’s largest platform for decentralized applications.”

So here we go again. Another crypto heavyweight is going after the SEC. Meanwhile, the SEC’s internal camp continues to speak out against its own actions. Long-time crypto-friendly SEC Commissioner Hester Peirce has written countless statements highlighting the agency’s hypocrisy, with her most recent one regarding a cease-and-desist order against ShapeShift being my personal favorite.

And why not throw in a little abuse of power for good measure as well.

While none of these events will end soon, nor will they be completely definitive, there is one thing for sure. The war is gaining speed, not slowing down.

I remember a time when I didn’t even know the SEC Commissioner’s name. Like a good ref or umpire, it’s probably not great for anyone when they become the story.