What happened this week in the Crypto markets?

What happened this week in the Crypto markets?Corporate Bond and Equity Supply versus the Bitcoin Halving

Despite Friday’s equity selloff, the S&P 500 finished April with a whopping 12% gain; its best monthly performance since 1991. Not to be outdone, Bitcoin (BTC) raced to the finish line in the last week of April with a 12% week-over-week gain and finished the month up 34%. Bitcoin and several other digital assets have now completely retraced the March 12 lows, rising over 100% since “Black Thursday”. Record monetary and fiscal stimulus is creating the perfect macro backdrop for this inflation protected, non-sovereign digital asset class. Further, the recent high positive correlation between BTC and the S&P 500, which we feel was more of a blip based on liquidity pressures than a trend, is now starting to subside, while the Chinese Yuan is once again falling versus the dollar, which has historically had a much higher negative correlation to Bitcoin. Within this context, you might even argue that Bitcoin’s strong performance is actually underwhelming given its historical high beta to other risk assets. Could April’s move simply be a precursor for what is to come?

Bitcoin Halving Starting with Supply and Demand

To explore this further, let’s start with simple supply and demand. The highly anticipated “Bitcoin halving” is now upon us, with an estimated date of May 12th, and there is record interest in this upcoming “event”.

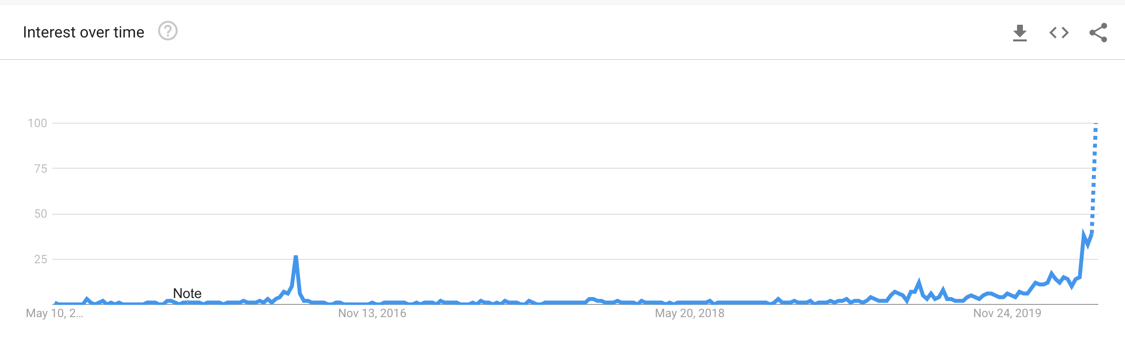

Google Trends Search Term “Bitcoin Halving”

Source: Google Trends -- A value of 100 is the peak popularity for the term.

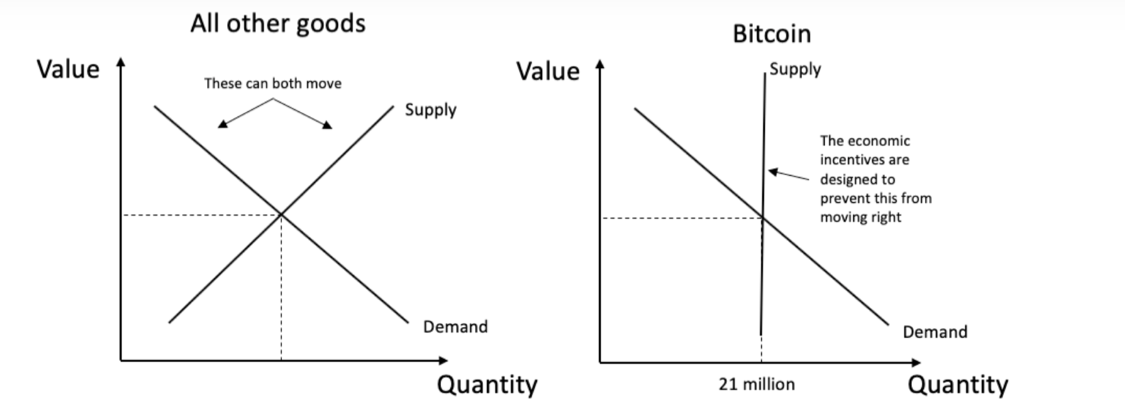

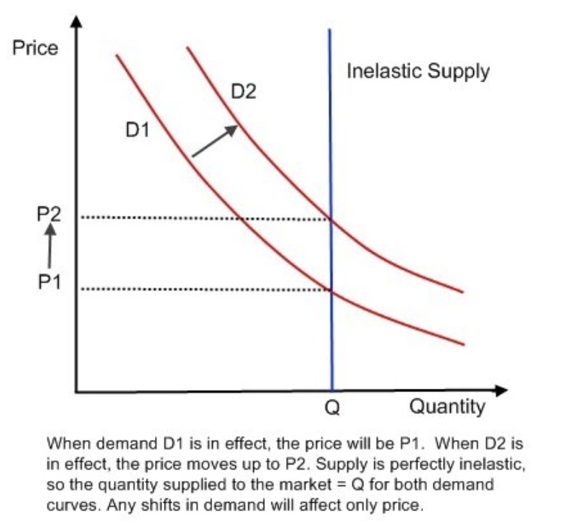

But in our opinion, the halving is not an event at all. In fact, the supply of Bitcoin is fixed at 21 million coins, and this fixed supply is well known. As a result, the supply curve is vertical -- it is perfectly inelastic as supply does not change based on price or demand.

This means that price can only change due to a shift in the demand curve, not a move along the demand curve.

So rather than debate microeconomics, let’s focus on the demand curve. Generically, the following attributes cause a shift in the demand curve:

- Income

- Trends and tastes

- Prices of related goods

- Expectations

- Size and composition of the population

All of these are certainly in play as it pertains to the future growth in Bitcoin adoption, and subsequently price. But none of these are specific to the halving itself. That said, there is still reason to believe that the price of Bitcoin will move higher as a result of the halving, for one simple reason: The amount of newly issued Bitcoin is miniscule relative to the amount of investment dollars.

For context, let’s look at the corporate bond and equity markets. Before this year, corporate bond monthly new issuance would typically average $100 - $120 billion in new deals per month. In March 2020, corporate bond issuance reached $260 billion, and in April 2020, issuance reached $285 billion (including a record $22 billion from Boeing alone, which saw $50 billion in orders). According to Cantor Fitzgerald, there is over $300 billion already slated for May as well. Similarly, US Equity IPOs, while much smaller, average roughly $3-4 billion in new issues per month. And while these deals may be on hold right now, there is still plenty of demand from investors for both debt and equity new issues.

Newly mined Bitcoin meanwhile is approximately 1800 BTC per day, which will fall to ~900 BTC per day following the mid-May halving. At today’s prices, that equates to roughly $240 million per month of new Bitcoin, or 12x less than new equity offerings and 500-1000x less than corporate bond offerings.

You can throw your economics charts aside… there just ain’t enough Bitcoin to satisfy new investor demand.

Breaking News: Financial Advisors Don’t Recommend an Asset They Can’t Profit From

Without a Bitcoin ETF, financial advisors really have no way to profit from advising their clients to buy Bitcoin. So it probably comes as no surprise that very few are pitching digital assets to their clients. While there are certainly some advisors out there that have their clients’ best interests at heart, financial products are typically sold, not bought. And to sell, you need proper incentives.

Quite frankly, the digital assets space needs more salespeople, and unfortunately this space is too young and lacks sufficient revenues to employ top salespeople. While a few firms are now large enough to run aggressive sales and marketing programs (i.e. Grayscale, Galaxy, Bitwise), the majority of interest is coming from reverse inquiry. This is the definition of the tail wagging the dog. Meanwhile, asset managers continue to flock to this space because they believe in the return potential. In the traditional alternative investment world, most funds won’t even launch unless they get to $150-200 million in AUM so they can support their business with management fees. Those entering the crypto space, however, are making a bet based on a belief that performance fees will be more than enough to pay for their business risk. That’s oddly refreshing, even if greedy.

In a world where everything is changing, isn’t it time to rethink how and why you buy financial products? Do you want the product that is large enough to afford the best salespeople, or the product that exists and survives on its actual performance merit?

It’s kind of funny that one of the biggest knocks on crypto is that digital assets haven’t found a use case yet, which would imply that investors are simply gambling on an unknown future. At the same time, almost every equity investor has now completely written off 2020 earnings (and 2019 earnings) and is pointing to how cheap stocks look versus expected 2021 and 2022 forward earnings ratios. Hmm.

We have talked at length recently about how antifragile digital assets are, falling and bouncing back with no intervention. Meanwhile, the debt, equity and commodity markets continue to be propped up by government stimulus and hope. If you need a refresher, our friends at Messari did an excellent job detailing and explaining all of the different stimulus actions taken by the Fed and the Treasury in the past few months (not including all of the stimulus from the ECB and Japan and everywhere else in the world). This took me 20 minutes to read because the list is so long including lowered rates, repo, QE4, QE unlimited, lowered reserve requirements, FX swap lines and a whole host of new acronyms (TALF, PPPLF, MSNLF, MSELF, PMCCF, SMCCF, MLF, CPFF, MMLF, PDCF) that collectively stand for “money anywhere and everywhere”.

The takeaway is not that the Fed and Treasury overstepped -- if anything this is the first time in 10 years where this was actually necessary. But if your entire investment thesis for owning stocks and bonds requires this much intervention just to survive, shouldn't every debt and equity investor at least be willing to listen to alternative thought processes?

If 2020 has taught us anything thus far, it’s that we should be approaching challenges with an open mind.

Notable Movers and Shakers

Whereas last week saw significant bifurcation amongst the asset class (BTC.D unchanged), this week was much different: Bitcoin lurched ahead early in the week and never gave up ground (+15%, BTC.D +3%). As such, only one project stood out to us as a notable mover:

- Theta (THETA) has been gaining momentum since “Black Thursday”, presumably due to its March 10th announcement regarding its 2.0 main net upgrade. On Saturday, Theta partnered with World Poker Tour to provide 24/7 live poker video content on Theta.tv - a timely announcement as quarantine continues to impact the status quo of social interactions. The token continued to gain traction this week, finishing up 29%.

What We’re Reading this Week

At an online event last week, the head of Ernst & Young’s blockchain division discussed how public blockchains, not private blockchains, could be the best long-term solution for enterprises. Most enterprise blockchain solutions to date have focused on building out internal private blockchains, which mask the data and transactions of these large companies. However, open blockchain networks offer the benefit of shared access across various enterprises, eliminating the data silo effect present in today’s networks. To date, EY has specifically focused its blockchain development efforts on the Ethereum network, building out its Baseline Protocol in conjunction with Microsoft and ConsenSys for enterprises.

Last week, Nasdaq announced it had partnered with R3 to offer a digital assets platform on the Corda blockchain. The partnership is an integration of the Corda blockchain technology into Nasdaq’s current Financial Framework technology, which covers the matching engine, surveillance, data discovery and reporting services. The new digital asset marketplace will allow capital markets participants to manage issuance, trading and settlement of digital assets and symbolizes Wall Street’s evolution towards digitized blockchain solutions.

Famed venture capital firm Andreessen Horowitz last week announced it had closed $515m for a second crypto-focused fund. The firm also laid out its broad investment thesis for crypto highlighting payments, store of value, decentralized finance and Web 3 as its areas of focus. This thesis differs from its first crypto fund’s focus which was on stablecoins, financial inclusion and the tokenization of real-world assets. Despite the new focus, the fund still highlights that we are in the early stages of crypto and there is still much to be done on the infrastructure side before full adoption can be reached.

Messaging app Telegram, which has been locked in battle with the SEC for the past 8 months, announced last week that it is delaying the launch of its blockchain network and returning investors’ capital. The decision comes after a US court ruled that Telegram cannot launch its blockchain network or distribute its tokens until the case with the SEC is resolved. The official new launch date of the TON network is slated for April 2021 and as a result is offering investors a 72% refund on their initial investment ($1.2b of the $1.7b raised in 2018). However, investors also now have the opportunity to receive 110% back via a new loan agreement in April 2021 when the network launches. Once the most hotly anticipated blockchain projects, Telegram is now scrambling to push its project forward while appeasing both the SEC and its VC investors.

A blockchain voting application, Voatz, was used at the GOP convention in Utah to decide on the primary’s nominees. Backed by Overstock’s Medici Ventures, Voatz previously suffered a handful of security flaws but the Utah virtual state convention is its most significant trial to date, during which it processed 93% of the registered vote delegates. The use of Voatz for the convection was particularly useful in a time when in-person events cannot be held and shows promise for use in future elections while the coronavirus pandemic hangs over the world.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency