What happened this week in the Digital Assets markets?

What happened this week in the Digital Assets markets?Week-over-Week Price Changes (as of Sunday, 1/10/21)

|

|

WoW

|

YTD

|

|

Bitcoin

|

+14%

|

+30%

|

|

Bloomberg Galaxy Crypto Index

|

+14%

|

+42%

|

|

S&P 500

|

+1.8%

|

+1.8%

|

|

Gold (XAU)

|

+3.5%

|

+3.5%

|

|

Oil (Brent)

|

+8.5%

|

+8.5%

|

Source: TradingView, CNBC, Bloomberg

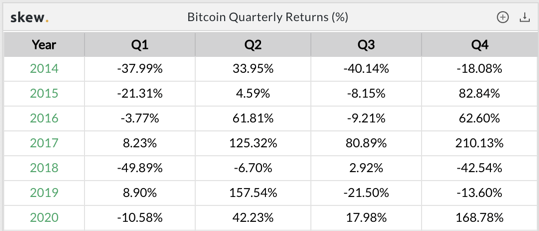

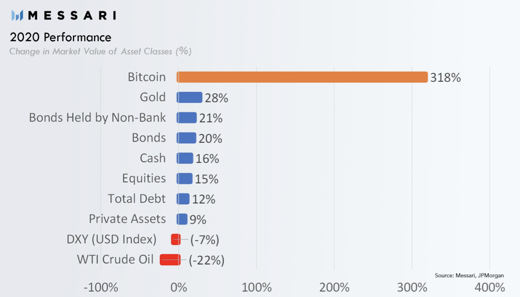

Bitcoin is 2020’s Best Performing Macro Asset (Not Asset Class)

Bitcoin had a monstrous 4Q, catapulting it once again to the top of the global macro stage, and it has yet to stop in the first full week of 2021. But there were also over 40 other digital assets that outperformed Bitcoin in 2020, most of which have nothing to do with money or cryptocurrency. Digital assets is an asset class. Bitcoin is simply the most visible and well known part of this asset class.

So What Caused the Rally since mid-December?

Our last “That’s Our Two Satoshis” of 2020 was published on December 21st. At that time, Bitcoin was just under $24,000; and Ethereum was just above $600. It’s been a wild ride since then, with Bitcoin hovering around $35,000, Ethereum around $1100, and numerous other digital assets gaining even more over this time period. Those dedicated to digital assets like ourselves didn’t have a relaxing holiday break.

So what has changed in the last three weeks? Honestly, nothing. The factors driving the value proposition and adoption of both Bitcoin and other digital assets have not changed; the announcements of those who are finally recognizing these factors and entering the market have simply accelerated. This is reflexive, as it gives others more confidence, and the constant headlines garners even more attention.

The factors driving digital asset adoption are simple.

- Cash is dead

- Fixed income is dead

- Equities are frothy

- The US dollar is crumbling

All of the money that is coming out of these other asset classes has to go somewhere, and when “somewhere” includes an asset class that is both tiny and accelerating, prices can change quickly and violently. The small size of digital assets relative to the new money pouring in certainly contributes to the outsized returns, but this is not the only factor causing rapid price increases. Another factor is that a large part of the digital assets investable universe simply cannot be valued, and by definition, if it has no value, it can’t be overvalued. Some assets of course can be valued, and we spent most of 2020 discussing how this asset class is maturing to the point where traditional cash flow and yield analysis drives price movements of certain pass-thru equity-like tokens and asset-backed tokens. But many of the largest and most crowded “high upside, low probability of success” tokens simply cannot be valued, including Bitcoin, Ethereum and most of the largest tokens by market cap. Similarly, most SPACs, and even certain popular stocks like Tesla (TSLA), fall into this same “infinite upside” fallacy, simply because there are no fundamentals supporting the valuation. Some of these investments clearly have more merit than others, but they share a similarity that they can never actually be overvalued. While most investments have theoretical ceilings, governed by cash flows, asset value, or yields…. in a world of low rates, tons of stimulus, and a declining dollar, it’s possible that investors may actually be better off in investments that have no ceiling.

That’s not to say that we should brush off this rally like many digital asset naysayers. An insane amount of progress has happened since the last bull run in 2017, both in terms of project breadth and token economics structure. But there is no rhyme or reason for why the market decided to finally care about all of these factors in the past 3 weeks.

But Now That Everyone Has Access to Bitcoin...

… the investing landscape and opportunity is going to change. Bitcoin is now a global macro asset, graduating from the ranks and comparisons of other “non-money” digital assets to the front-page of CNBC, and every Deutsche Bank and JP Morgan macro strategy report. Bitcoin’s correlation to other digital assets has decreased substantially since March 2020, as the drivers of Bitcoin are no longer the same as the drivers of cash-flow producing companies with tokens. Further, the skills needed to invest in Bitcoin (macro/trading) and even Ethereum (tech) are vastly different than those needed to invest consistently in pass-thru tokens and asset-backed tokens (research/modeling).

With the rise in Bitcoin infrastructure (via Fidelity, Coinbase, CME, Grayscale, Square, Paypal), the rise in passive Bitcoin funds, and the rise in “Bitcoin tracking stocks'' (i.e MSTR, GLXY, Hut8 and soon Coinbase’s IPO), just about anyone who wants direct Bitcoin exposure now has a myriad of options to choose from to get that exposure. Further, the launch of public large cap trusts like the Bitwise 10 and Grayscale large cap index has led to overpriced trusts with huge premiums to net asset value, making it even more important to dig deeper into other areas of digital assets in order to uncover real value. It’s likely that any actively managed hedge funds or passive indexes built around high allocations to Bitcoin have a very short shelf-life. Investors now have the knowledge and means to buy Bitcoin and Ethereum themselves, and will not rely on high fee active managers to give them this exposure. Very soon, investors will seek out digital asset hedge fund strategies that specifically do NOT own Bitcoin, as investors will look for differentiated returns generated from high growth real companies and products that have implemented a digital asset into their capital structure.

NO, We Don’t Care About XRP, XLM, ADA or other Top 10 Tokens

When digital assets rally, and retail euphoria kicks in, the phone calls and texts start pouring in. That means a lot of “What do you think about XYZ?” questions, typically focused on the more well known, but often completely useless and worthless tokens from the 2017 vintage.

Of particular note is the recent SEC versus XRP-Ripple event, which has caused a 45% decline in the token price over the past 30 days as most major exchanges have delisted it. Somehow, the XRP token is still the third largest token by market cap, despite the fact that I don’t know a single professional fund manager (other than passive index vehicles) that own XRP for any reason other than beta. But the SEC news is not what makes XRP uninteresting. As our friend Mike Creedon said,

“People seem to misunderstand the global scope of the SEC. In fact, they don't make the world's securities laws. They will hunt people down all over the planet who rip off Americans. Big distinction. Our regulators aren't telling Dubai, Singapore, London what to do. XRP-Ripple could see a deathknell here but I don't know why they couldn't move elsewhere, pay the fine - which will be gargantuan - and soldier on. Steve Cohen of Point 72 once paid nearly $2 billion for a legal infraction. Last month, he bought the New York Mets. And he didn't even have to leave the country. We'll see more of this in crypto and traditional finance in the years ahead. It's what's called "regulatory arbitrage". And it won't go away.”

He’s exactly right. Ripple didn’t fall 45% because the SEC is tired of Ripple continuously selling tokens to American retail investors. Ripple fell 45% because the token has no value proposition other than being liquid and available to trade on exchanges. The XRP token was being sold for years in a perpetual 2017-like fundraising ICO, but never created any value. Everyone who did any research whatsoever knew this, and very few institutional investors owned it. It simply has strong name-brand recognition, and retail investors gobbled it up, not too different than when Hertz filed for bankruptcy and retail investors bought the stock even though it is almost certainly worthless. The only interesting news related to Ripple is that because their token has no value, and because they kept selling it, the SEC basically shut down their ability to do so, and as a result, all of these exchanges de-listed it. It doesn't change the value proposition (there never was one), it just changes the ability for traders to trade it. Ironically, the XRP token may actually become more valuable now. Since trading can no longer be the driving force of demand, Ripple will be forced to actually come up with a use case and a value proposition for its XRP token. The flexibility of token structures means we probably haven’t heard the last of XRP.

Perhaps more interesting are the implications for U.S. companies and investors going forward. While we applaud regulation, it’s not a great look for the U.S. to be on the small list of banned countries that include Cuba, Iran and North Korea. It will be difficult to become a digital assets powerhouse when we’re alienating all of the talent working in this space.

What’s Driving Token Prices?

With Bitcoin posting its fourth consecutive week of double digit gains in confluence with a broad stock market rally and increased talks of a larger stimulus package around the corner, there is a heightened awareness around the digital asset market. Of the Top 100 assets by market capitalization: 84 finished the week positive, 57 finished up double digits, 30 finished up 25%+, and 11 finished up more than 50%. These kinds of moves are bound to breed intrigue, but on a week like this it’s hard to give more than a generic blanket statement about the potential of this space. There were a few updates, roadmaps, and partnerships; however, by and large the market traded together throughout the week and nothing stood out as a driver. As such, this week we abstain from individual movers and look forward to idiosyncratic movements returning in the following weeks.

What We’re Reading this Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

Alex Woodward- Analyst

To learn more or talk to us about investing in digital assets and cryptocurrency