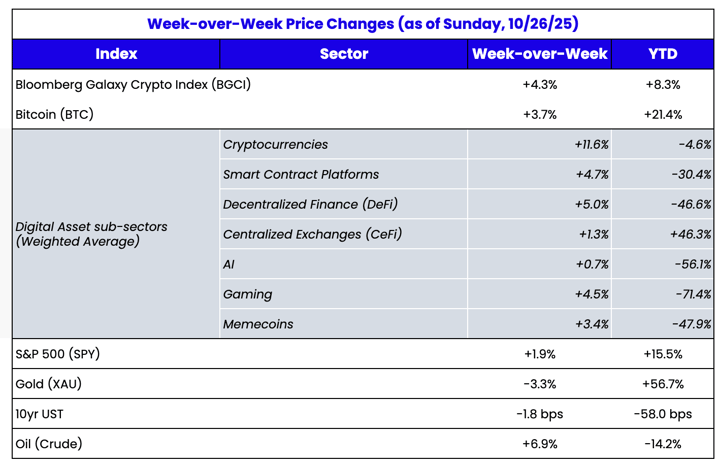

Source: TradingView, CNBC, Bloomberg, Messari

The Positive Headlines Continue

Digital asset investing is at an inflection point.

The young cypherpunks who started the Bitcoin movement are no longer young, now that 15 years have passed since Bitcoin’s genesis block. The old-school ICO builders and investors from 2017 have had almost 10 years to reflect on their successes and failures, and many have moved on to new industries, been wiped out by high leverage, or are now so successful that they talk to Washington and Wall Street more than they write code. Investors who once poured into crypto funds, often with little to no knowledge of what they were investing in, are now simply buying ETFs. What was once an optimistic, youthful industry has been replaced by a very pessimistic group of older traders and Twitter influencers, many of whom now make more money on social media than they do in crypto. The combination of PTSD from 2022, horrible token launches, predatory tokenomics, and a flash crash earlier this month has soured the minds and crushed the hopes of many of crypto’s original cheerleaders.

It’s perhaps no surprise that nearly all of these people were bearish last week, at what we believe are likely to be the lows.

But I didn’t say crypto was dead, I just said it was at an inflection point. The new wave of crypto investors who aren’t burned out or burned are as optimistic as ever. These new investors come from both sides of the spectrum – from more sophisticated TradFi funds and banks, to the retail Robinhood crowd. This new wave of investors is way bigger than anything this industry has seen before, and they buy dips, just like they do in the equity market. They don’t immediately turn bearish the second prices go down, and they don’t live on crypto Twitter reading about things that haven’t been relevant in years written by one-trick ponies from 2017’s glory days. In some cases, they are still being steered into the worst assets by “exchanges” brokers who cater to VCs and founders rather than secondary buyers, who fail to properly educate on the differences between a memecoin and a cash-flow-producing company with a token. However, they are largely still optimistic about the industry’s growth.

As we wrote two weeks ago, most of these new investors weren’t harmed at all by the levered washout from two weeks ago. Instead of trying to play detective to figure out which market maker or market-neutral fund may have blown up, they simply saw lower prices and stress-tested DeFi infrastructure.

The majority of signals that used to work 5 years ago to understand momentum and price action no longer work; they have become contraindicators. I don’t think anybody in crypto truly understands the flows anymore, as we are all just small pieces of a larger TradFi puzzle now.

And that is not a bad thing at all. It’s a sign of this industry's maturation.

Any first-year analyst could have looked at last week’s news flow and, objectively, realized that all of the data points were absurdly positive. For example:

- JP Morgan called for the end of QT, and the market priced in 100% certainty of 2 more rate cuts by year-end after the softer CPI print.

- The crypto market structure bill is moving forward. As Galaxy Digital wrote this week, “We wrote in July that the House’s passage of CLARITY raised the odds of crypto market structure being signed into law before the 2026 midterm elections from 25% to 35%. Our general skepticism then was born from a fear that the complexity of the issues and a lack of sufficient Congressional floor time presented significant headwinds. However, we are now raising our assessment of the likelihood that a bill hits the President’s desk for signature before the summer recess next year to 60%. Our more optimistic view is largely driven by the meetings held in Washington this week.”

- Hyperliquid (HYPE), one of the profitable companies in crypto and one of the best-performing tokens this year, was finally listed on Robinhood this week, proving that good assets with good tokenomics will finally be listed somewhere, even if not on Coinbase.

- President Trump scheduled a meeting with Chinese President Xi, with Treasury Secretary Bessent saying that China and the U.S. have reached a framework.

- All of the macro fears are slowly eroding, from regional bank lending issues to the repo markets thawing.

- Corporate earnings have been fantastic thus far in the 3rd quarter

- JP Morgan, Charles Schwab, Fidelity and a host of other top banks and brokerages put out headlines last week about various ways in which they are adopting crypto, or launching trading/lending.

- Global stock markets continue to bounce back, reaching all-time highs yet again.

You wouldn’t need more than 2 weeks in a finance or economics class to realize that last week was bullish.

And yet, so many in the crypto world were looking for the worst possible outcomes just because it had taken a few days to work out the issues from the flash crash 2 weeks ago. A summary of my chats and conversations over the last few days looked like this:

"Yes, everything is bullish, but price isn't reflecting that, therefore it is bearish"

That’s the tail wagging the dog. When setups are obviously bullish, they usually are. There’s no need to overthink this.

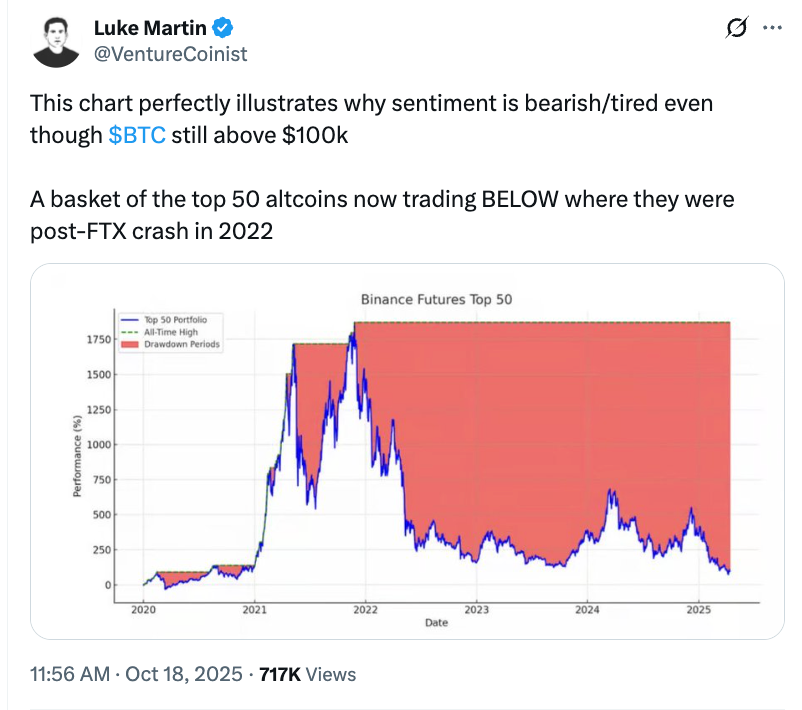

Now, I’m not entirely sure what will make certain areas of the crypto market rally at this point. And I’ve always been on record that not all of crypto will, or should, rally anyway. Most of these assets should go to $0. Even in a highly correlated market driven by market makers, dispersion can still happen between the “haves” and the “have-nots”. And when that does happen, it angers those holding the “have nots”, but it encourages institutional investors and stickier money to do the research on what causes a token to be in the “haves” camp. We’ve been pointing out for months how this “bull market” in crypto hasn’t been a bull market at all. It’s healthy that the worst of the worst assets are no longer blindly going up for no reason, while some of the better projects with good tokenomics have outperformed.

That’s a good chart. Most of the “top 50 altcoins” are terrible assets. As my colleague Topher Macpherson pointed out, have you ever looked at which assets appear on the Binance Top 50? Consider us not shocked that COA, KGEN, RVV, SLERF, RECALL, BAS, ZBT, YEI, XPIN, TOWNS, RIVER, LAB, BANK, YB, and EVAA aren't driving incredible returns. Token investing isn’t dead – but free 1000% returns with no due diligence are most certainly dead.

While we may lose some of crypto’s OGs in the process, they are being replaced by investors who will help take this asset class to the next level. And if this upcoming week has the upside legs that we anticipate, it could wipe out yet another group of pessimistic bears, while further differentiating between the “haves” and the “have-nots”.