What happened this week in the Crypto markets?

Source: TradingView, CNBC, Bloomberg, Messari

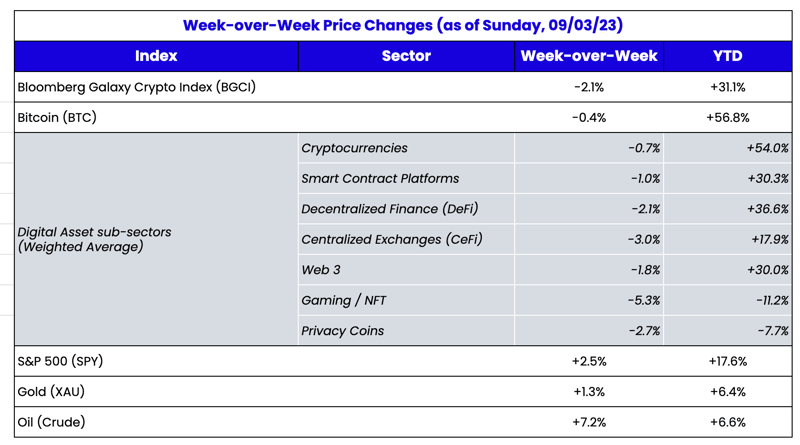

A Noisy, Unchanged Week For Digital Assets

Jobs data, GDP, and consumer confidence all came in well below expectations, and since bad news is once again good news for stocks, equities pushed higher. Fixed income markets were mostly quiet, with yields pretty much unchanged week-over-week. The U.S. Dollar was largely unchanged and the VIX came crashing back down to YTD lows.

Normally this would be a good setup for digital assets broadly, and coupled with any idiosyncratic tailwind, a much needed rally could have been sparked. But alas, without new capital entering the market, there are just too few buyers to generate any significant upside price action, especially in the face of relentless selling from VCs and a handful of bankruptcy liquidations from the FTX and Celsius estates.

Overall, prices of large-cap digital assets were largely unchanged, while small caps continued their decline. However, the weekly graph of Bitcoin (BTC) below suggests that there was an idiosyncratic crypto news event that, at least momentarily, jolted markets higher. This news came from a U.S. Court of Appeals ruling in favor of Grayscale in their lawsuit against the SEC, which challenged the agency’s denial of an application to convert Grayscale Bitcoin Trust (GBTC) into an ETF.

GBTC is currently the largest Bitcoin fund with ~$16.3 billion in assets under management and owns over 3% of all Bitcoin outstanding supply. Obviously, once an ETF is approved, Grayscale will face severe competition from Blackrock, Fidelity, and others, and Grayscale’s hefty 2% management fee on the current trust will be cut at least in half, if not much more. So the bet Grayscale is making is that their huge lead on the competition in terms of AUM, combined with positive press from this lawsuit, will help them grow assets to offset the fee pressures.

Since an ETF is inevitable, eventually, Grayscale really has no choice but to feign interest in an ETF, but the victory itself is pretty hollow. From a market perspective, the immediate rise in BTC price following the news made little sense. The Grayscale news is irrelevant for prices. The market was already pricing in a 100% chance of a Bitcoin ETF being approved at some point in the future, and Grayscale’s victory didn’t improve those odds above 100%, nor does it speed up the timing. It was a moral victory perhaps, as another take-down of Gensler’s SEC provided plenty of Twitter fodder, and the Judge calling the SEC’s decisions “

arbitrary and capricious” made for a good laugh, but it was a pretty empty catalyst nevertheless. Following the news, Bloomberg analysts increased the probability that a spot Bitcoin exchange traded fund (ETF) will be approved in the US before the end of 2023 from 65% up to 75%, with a 95% chance of one being approved by the end of 2024. A non-factor in the price of Bitcoin. We need an actual ETF to increase fund flows as no one has an incentive to front-run the news.

- Spot and futures ETFs are different

- Surveillance sharing agreements and market sizing do not support a spot ETF

However, this does not mean the SEC will speed up their approval. As Bloomberg reports, the next major time frame to watch will be the middle of October, but realistically, we believe that January, at the earliest, will be the actual time frame for approval since that’s when Ark’s application hits its final deadline.

Unfortunately for the market, there is no ETF-related news that will do anything for markets other than an actual approval because only the actual inflows caused by a Blackrock ETF and subsequent aggressive marketing can create new “buy interest”.

Can’t get enough of the SEC? Here comes the Treasury and IRS!

Per Galaxy Digital:

“For background, in August 2021, when Congress was weighing President Biden’s Infrastructure Bill, later named the “Infrastructure Investment & Jobs Act,” language was included that broadened the IRS’ tax reporting rules to include a wide swath of entities in the digital assets ecosystem. At that time, we wrote that this language was ‘bad and needs to change,’ arguing that the language was highly problematic because it could require IRS reporting from several types of previously un-covered entities, including several that functionally will be unable to comply. Under the proposed rules, digital asset entities that qualify as brokers would need to 1) perform KYC on their users and 2) furnish individual users and the IRS with transaction information (including gross proceeds) for digital asset sales/conversions on Form 1099-DA.”

The issue here is not paying taxes, of course. Most investors would (and do) pay their taxes to the best of their ability. The issue is that no DeFi applications are set up to issue 1099 statements and properly report on users’ behalf. Specifically, any “facilitative service” that is “in a position to know” its customers’ information and profit-and-losses would qualify as a broker and would need to perform tax reporting. That’s an impossible task for a decentralized protocol. The proposal appears to treat all sorts of people as "brokers" even though they

have no way to comply. The IRS is accepting public comments until October 30, and if adopted, the rules go into effect for the 2025 tax year (for taxes filed in 2026).