What Happened This Week in the Digital Assets Markets?

What Happened This Week in the Digital Assets Markets?

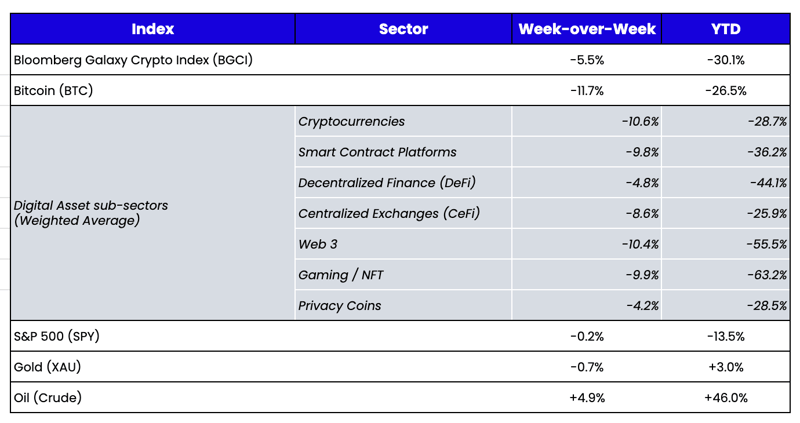

Week-over-Week Price Changes (as of Sunday, 5/08/22)

Source: TradingView, CNBC, Bloomberg, Messari

No Relief in Sight

The sole reason the world is in the mess it is in today is because Fed Chairman Bernanke, a student of the Great Depression, decided that throwing money at the 2008 mortgage crisis and whatever consequences came with it was a worthwhile trade-off to avert a global depression. Current Fed Chairman Powell accelerated this "throw money at all problems" solution, culminating in the record response to Covid in 2020. Yet today, market sentiment has never been lower; market participants are trading as if a depression is imminent, essentially saying that the Fed bought us 13 years of prosperity, but the end game will still be the same—economic depression. It’s the ultimate “kick the can down the road” strategy.

While pretending to fight inflation is the target of the Fed’s current monetary policy, it’s anyone’s guess whether or not real economic contraction and a market crash will ultimately cause the Fed to bring back the “Fed put” and ease up on its rate stance. The Fed and other central banks worldwide are playing a giant game of chicken. They know rate hikes don’t actually fight supply-side inflation, and rates markets have already priced in 2 years of rate hikes anyway. So the only real inflation risk is that consumers fear inflation so much that they make it worse by front-loading purchases (if you think prices will go higher, you buy more now, driving prices higher faster). As a result, the Fed's primary tactic is to jawbone about how they are "tackling inflation" just long enough to keep consumers at bay until natural deflationary forces lower inflation organically (which is already happening). Long-term deflationary forces include technology, an aging population, and crushing debt loads. Short-term variables include economic contraction, negative wealth effect, and the easing of shipping and supply chain issues).

As expected, the Fed announced a 50bps rate hike to 0.75-1.0% last week (the first 50bps hike since 2000) and a balance sheet reduction plan. The Fed seemed to be trying to calm markets last week, removing a future 75 bps rise from the equation and indicating that inflation may have peaked (we’ll see if that’s true this week with the CPI number). But the knee-jerk response higher in equities and digital assets was immediately met by massive selling into the week’s end. U.S. equities have thus started May with a fifth week in a row of losses for the major averages, and digital assets have declined for six straight weeks—a new record. 2022 has seen the worst total return start for the U.S. 10Y Treasury (or proxies) since 1788!

It’s bad out there. But we still have record employment, strong consumer and company balance sheets, and none of the financial stresses from 2008. This is just a buyer strike of ultimate proportions, and it remains to be seen what (if anything) will bring buyers back.

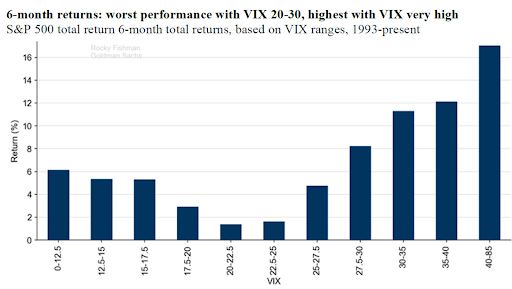

The biggest bull case is simply that the bear case is so strong that it is almost certainly wrong. CNBC, in fact, has a perfect track record of incorrectly stoking fear. The 6-month returns after the VIX spikes to 35+ are 10%+; 12-month returns after the VIX spikes to 35+ are 20%. So again, most of the time, investors are wrong when they get this negative.

The only thing we know for sure right now is that no one is afraid to sell or short digital assets. It’s working, so keep doing it. But the amount of firepower to buy is at the highest level ever relative to the number of assets available. The Stablecoin Supply Ratio (the orange line on the graph) shows the market cap of Bitcoin relative to the amount of stablecoins outstanding, and it is currently at all-time lows. So if the market ever decides to buy digital assets again, the window to jump through is quite small.

Source: Glassnode

We Need New Blockchain Scaling Solutions

By Nick Hotz, Research Associate

Bored Apes and Spam Bots Brought Ethereum and Solana to Their Knees

One of the biggest long-term questions in the blockchain space is if and how we can eventually scale chains to accommodate millions and billions of users at prices they can afford. Before 2020, demand was low enough that Ethereum could handle virtually everything. However, 2020's DeFi summer and 2021's NFT mania drove a demand that became more than Ethereum could accommodate alone. As a result, other Layer 1s and sidechains emerged, taking over much of the burden. Even so, Ethereum remains highly congested with fees well above the other chains.

Ethereum's low scalability was on full display last weekend as the Bored Ape Yacht Club project launched its "Otherdeed" land plot NFTs for its upcoming metaverse, Otherside. In a frenzy to mint Otherdeeds, users sent transaction fees on Ethereum into the stratosphere up to a maximum of roughly $20,000 in fees for a single transaction. Even outside of this spike, users consistently paid 1-2 ETH ($3-6 thousand) to get in on the mint. The staggering fees priced out all but the biggest Ethereum whales, effectively taking the chain down and rendering Ethereum and its Layer 2 rollups unusable for hours. On a chain already notorious for exorbitant fees, excess demand for its blockspace can destroy the value of this public good for all but the wealthiest—an untenable outcome for those who want to onboard the world to blockchain systems.

Among the biggest winners of the 2021 blockchain scaling wars was Solana, a blockchain that boasts it can support 50,000 transactions per second to Ethereum's 15-ish. While this claim is dubious, the fact remains that Solana is incredibly fast and inexpensive to use. Moreover, Solana aims to run so fast that it can support all applications—DeFi, DAOs, NFTs, and everything in between—all on one chain. However, the downside of its low fees is that it is wide open to economic attacks.

Solana last week showed us the Otherside (pun intended) of the current blockchain scaling problems, going down for seven hours due to bot traffic. The culprit was "Candy Machine," an NFT minting tool, which bots spammed to the tune of 4 million transactions per second, knocking validators out of consensus and forcing the chain to halt. Solana validators were forced to debate blocking Candy Machine contracts to restore order, though they ultimately decided against it due to concerns about censorship. Still, in the interest of the chain's uptime, Metaplex (closely linked with Candy Machine) noted that it would implement a "botting penalty" to stem excessive traffic.

Unfortunately, due to its low fees, Solana is prone to bot spam in a way that Ethereum's high fees immunize it. And when bots aren't dealt with properly, it brings the network to a complete stop, meaning even wealthy users cannot use the network for long periods.

The Path Forward for Blockchain Scaling

While 2021's wave of scaling blockchains put a bandage on blockspace supply issues, they haven't yet offered a fundamental solution. We need to go back to the drawing board to understand how blockchains can actually scale. If we strip them down to their basic functions, blockchains are just computers with one extra function. Computers perform two essential tasks: making data available in the hard drive and executing or modifying data with RAM. Blockchains complete both functions while also reaching a consensus across the network about whether the executed data is valid.

Most blockchains currently house all three components in one place, on one chain. These are what we call "monolithic chains." Solana, Fantom, Terra, and Binance Smart Chain are quintessential examples that follow a strictly monolithic scaling roadmap, attempting to execute as quickly and cheaply as possible on the base layer.

Other blockchains break out some of these core functions to varying extents to separate chains. On the spectrum from mostly monolithic to mostly modular, roughly, we have Ethereum, Avalanche, Polkadot, Cosmos, and Celestia. All have roadmaps that will make them more modular over time, breaking out the roles of data storage, execution, and consensus across chains.

As a monolithic chain, Ethereum is poorly positioned to onboard the world. However, its roadmap will make it modular over time, offloading its execution capabilities to Layer 2 rollups and making data available on shards— parallel chains that will solely exist as a place to dump data. Coming to consensus about the validity of transactions will be the only responsibility of the Ethereum mainchain.

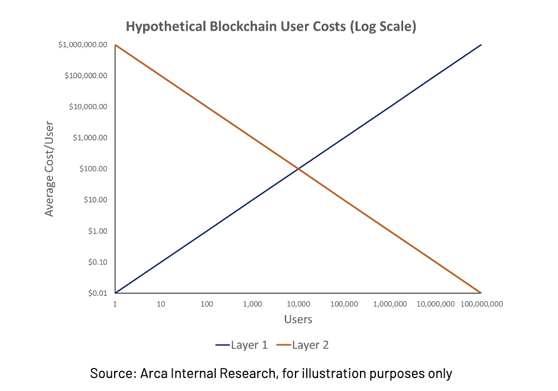

This modular world is far superior to the one we currently inhabit. For example, transactions on Layer 2s can be batched by the thousands or even millions back to the mainchain by providing a mathematical proof of their validity, ensuring security at a fraction of the cost. Further, due to the high fixed costs, but incredibly low variable costs of creating proofs, Layer 2s will actually see lower average cost per user as more people use the network, whereas monolithic chains become more expensive.

Much of the cost of transactions currently comes from storing data on-chain, which takes even more of the blockchain's precious blockspace. Making data instead available on a separate blockchain will dramatically reduce the cost of transactions and how quickly the chain grows, ensuring the chain can stay decentralized.

This modular world solves the problems we see today with monolithic chains. In the case of Ethereum, we see something as trivial as an NFT mint rendering the chain a plutarchy for hours at a time. However, a modular world will be able to execute data much faster and more economically than achievable today. In the case of Solana, we see the sacrifice of economic security to achieve scale, but with the drawback of much more downtime. Modular blockchains won't need to sacrifice economic security. Instead, they can be validated at a lower cost than Ethereum today while accruing sufficient rollup fees to be immune to economic attacks.

With 2021 in the rearview, we see which scaling ideas from that period worked and which glossed over existing problems. Despite this downturn in demand for digital assets, we can still see such problems emerge for monolithic chains, which shows the critical need for new scaling ideas. Those chains that fail to learn the lessons of 2021 will be left to the technological dustbin to be knocked down by apes and bots. However, blockchains that successfully execute on a modular roadmap will possess the speed, decentralization, and security necessary to pave the way for millions and billions of users to adopt these systems.