When All Digital Assets Trade The Same

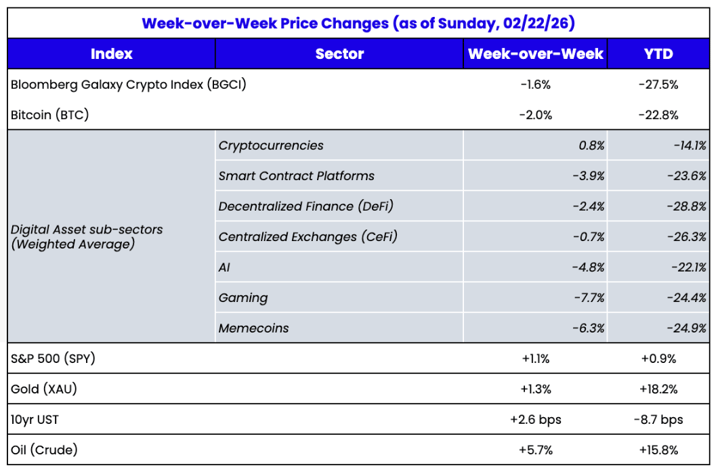

Digital assets largely moved lower again last week, and worse, they fell by roughly the same magnitude across all sectors and themes; L1s, DeFi, infra, gaming — it didn’t matter. Dispersion was minimal. When correlations spike, and everything trades in lockstep, that’s usually not from organic spot selling. That type of price action comes from market makers moving assets up/down together to manage overall risk, structured products unwinding, or derivatives positioning driving the tape. It tells you the marginal seller isn’t a fundamental holder exiting a specific thesis, but rather an overall balance-sheet repositioning.

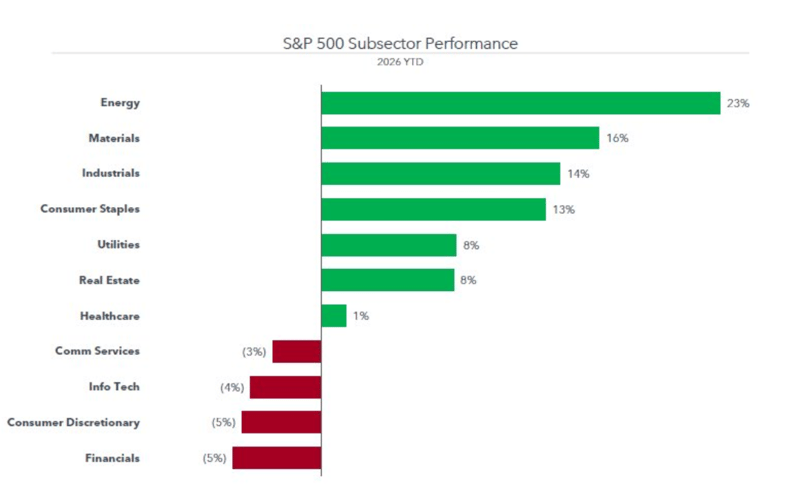

This continues to be the biggest detriment to token investing. Contrary to popular belief, investors often don’t shy away from volatility. Volatility is fine if the reasons for the volatility make sense, and the upside volatility warrants the downside volatility. But investors are used to dispersion, where there is typically some area of an asset class that is worth investing in, even if the asset class as a whole is lower. Take equities, for example. This has been a very volatile year, with massive dispersion by sector as software and other consumer cyclical sectors have been hit hard, and money has rotated into energy and consumer staples.

Source: Twitter / X

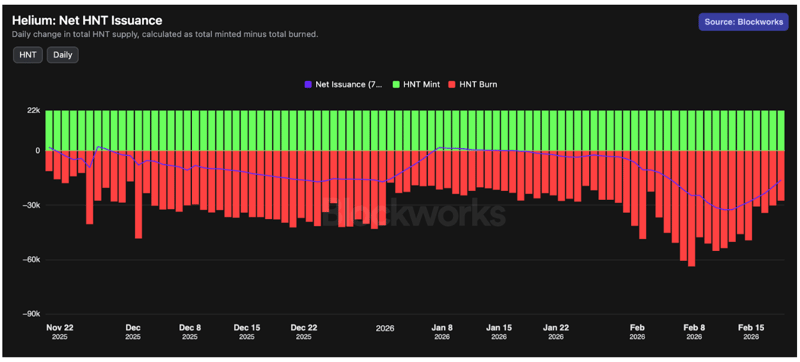

There were only a few bright spots in token prices last week. Helium (HNT) rose roughly +60% last week despite no official updates from the project. Token burns are still outpacing issuance, and structurally, that matters. When supply is shrinking, and price rises on limited news, it’s usually a signal that someone is either:

Source: Blockworks

The other notable outperformer was Aerodrome (AERO), which was essentially unchanged week over week. Uniswap announced that it is expanding its fee switch beyond V3 pools to every pool type. On the surface, this sounds positive for UNI holders via increased fee capture, but there’s a second-order effect. If Uniswap takes more from LP yields, it reduces the net return for liquidity providers. In a competitive landscape, it makes it harder to retain liquidity, especially when Aerodrome expands further into the EVM ecosystem.

Further, Base is moving toward operating as its own chain. On its own, that isn’t hugely meaningful. But if Base is formalizing its independence, the logical next step is a token generation event. When that date gets announced, activity on Base could spike as it often does around incentive cycles. And when activity spikes on Base, Aerodrome benefits.

Lastly, in a completely different example, Figure Technology Solutions (FIGR) priced a 4.23M secondary share offering of its Series A Blockchain Common Stock, not as a “tokenized” wrapper sitting on top of DTCC rails, but as a public equity natively issued on Provenance Blockchain, trading on an on-chain ATS, settling in self-custody wallets.

Even though FIGR stock continues to decline ahead of earnings (with a whopping 50% short interest), the broader point is that, as token investors, we need better tokens. And tokenized stocks could potentially help usher in a new era of return dispersion. As tokenized equities begin to trade on-chain, with real cash flow rights and real legal clarity, that creates a whole new category of token investing. When you introduce instruments with explicit claims on earnings, dividends, or equity, price discovery may improve, and capital may allocate more rationally. This could cause returns to separate based on fundamentals instead of liquidity conditions.

Ironically, tokenized stocks may end up being healthier for the crypto market structure than many native tokens.

Revisiting the “Crypto Hills I Will Die On”

A year ago (March 2025), I wrote 12 Crypto Hills I Will Die On. At the time, many of these points were debatable and often disputed by the larger crypto community. The uncomfortable reality is that most of those “hills” are becoming more true, and that’s bad for price action generically, but good for the long-term health of blockchain. Looking back, I wouldn’t adjust or change anything I wrote.

To be clear, most of these opinions weren’t from a year ago. I’d been writing and speaking about these topics for years, and only summarized them a year ago, focusing on themes I’ve written about for years:

What’s happening now?

All of that is structurally healthy. It just doesn’t create the type of indiscriminate beta that defined prior cycles. In other words, the market is growing up.

Unfortunately, growing up is rarely euphoric.

If you believed, as I have for years, that crypto needed:

Then this environment is progress. It’s just not exciting progress. And it certainly isn’t making for a great short-term investment environment.

ETH Denver

Katie Talati, Arca’s Head of Research and Advisory, just returned from ETH Denver. Among her many notes:

None of that is surprising. When the main conference energy drops but institutional side events are packed, it tells you where the center of gravity is shifting.

The early ETH Denver years were full of hacker energy. Now it’s allocator energy.

The themes reflect that shift:

The venture comment is particularly telling.

Despite lower public token prices, private valuations haven’t meaningfully compressed. That gap rarely persists forever. Either:

History suggests the latter eventually happens.

ETH Denver didn’t feel euphoric. It felt transitional.

Less “what can we build?”

More “how do we operate within the structure that now exists?”

That matches the broader market sentiment.