The Market Puke and the Search for New “Safe Havens”

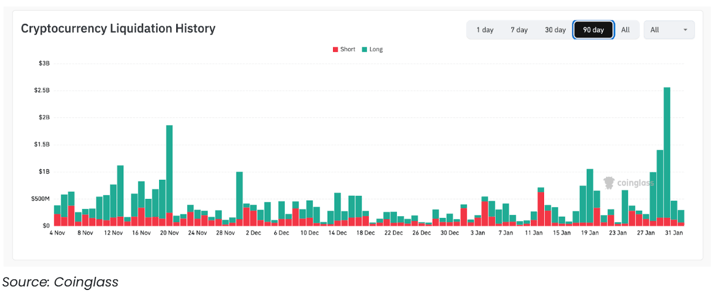

Total liquidations of crypto assets exceeded $5 billion over the last 4 days, marking the largest wave of liquidations since October 10th. For context, $1.2 billion in liquidations occurred during the Covid crash of March 2020, and $1.6 billion in liquidations happened during the FTX crash in November 2022. This weekend, on a random and seemingly quiet Saturday (from a news standpoint), $2.5 billion was liquidated, suggesting this was not a normal sell-off.

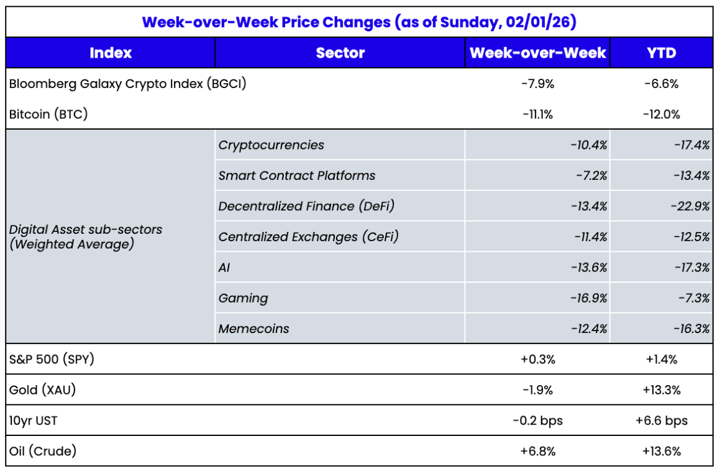

The week-over-week charts for most digital assets look pretty ugly. I say most because, once again, it is foolish to lump all assets together just because they are wrapped by a digital token. When folks in this industry talk about “crypto” price action, they tend to generalize based on how BTC, ETH, XRP and SOL perform, as these have been proclaimed as the “benchmarks” of digital assets due to their size (collectively, these four assets make up ~80% of the overall token market cap), and because market makers tend to move every other asset up or down in line with these four assets. This past week, these four assets were down -11%, -19%, -12%, and -14%, respectively.

Now, let’s say, for example, that Nvidia, Google, Microsoft, and Apple stocks were all down big in a given week (the 4 largest stocks in the U.S.), but there were a few big stocks in defensive sectors that made large gains. Would the story just be about those 4 assets, or would financial advisors, brokers, and the media try to focus attention on the assets that bucked the trend?

Hyperliquid (HYPE) gained +42% last week

Canton Coin (CC) gained +23% last week

Pump.fun (PUMP) gained +1% last week

(Past performance is not indicative of future results. The Arca Funds hold positions in HYPE, CC, and PUMP.)

What is unique about these 3 assets?

All 3 of these companies earn real revenue, have tokens aligned with the growth of their businesses, and have diversified earnings streams that are independent (or at least less dependent) on BTC, ETH, SOL, and XRP.

Source: X/Twitter

How many stories did you hear about these 3 assets this week? My guess is zero.

In fact, as I’m writing this, I received a call from the Wall Street Journal asking me to opine on the following:

(1) How bad do you think this crypto selloff could get? How much further could prices fall and why?

(2) Could the price declines force crypto treasury firms like Strategy and BitMine to sell their holdings?

(3) Any other implications of this selloff on the market?

Of course, I answered that this is a ridiculous question. I said it is dangerous and misleading to use the term "crypto" to refer to all blockchain-based tokens. Asking "how low can crypto go?” is equivalent to asking "how low can ETFs go?" That question, of course, makes no sense because the ETF is just a wrapper, and what is inside the wrapper matters more than the wrapper itself. In the same vein, not all "crypto" tokens can be lumped together—there are different sectors and different asset types that behave differently. Stablecoins are part of crypto, and they aren't moving lower at all because many are backed by U.S. Treasuries. Hyperliquid (HYPE) is part of crypto, but its token is actually higher because it is a DeFi-based Perp DEX that is generating a lot of revenue from liquidations and trading fees.

I doubt my quotes will be included in their story.

Perhaps a better way to frame this is by discussing “defensive sectors.” In the U.S. corporate bond and equity markets, it has been pretty well defined over the years that consumer staples, utilities, healthcare, defense, and a handful of other sectors are “defensive.” Similarly, investment-grade bonds are more defensive than high-yield bonds, which are more defensive than distressed bonds.

Did these assets and sectors become defensive because their prices performed better than cyclical assets during bear markets? Or did certain assets become defensive because of the market leaders that guided investors towards these sectors during bad times?

The former is more likely, but the latter matters too. These assets/sectors were classified as defensive due to their fundamental characteristics, which lead to stable demand and higher earnings/cash flows, and thus better relative price performance (lower declines, sometimes outperformance, or positive returns) during bear markets, recessions, and economic downturns. Analysts, strategists, and the media recommend rotating to defensives (or IG bonds) when recession/bear signals appear, and inflows follow as investors seek safety.

This seems to be a pretty important part of the corporate investing world, and quite frankly, common sense. Rotation into defensive areas is an important part of investing.

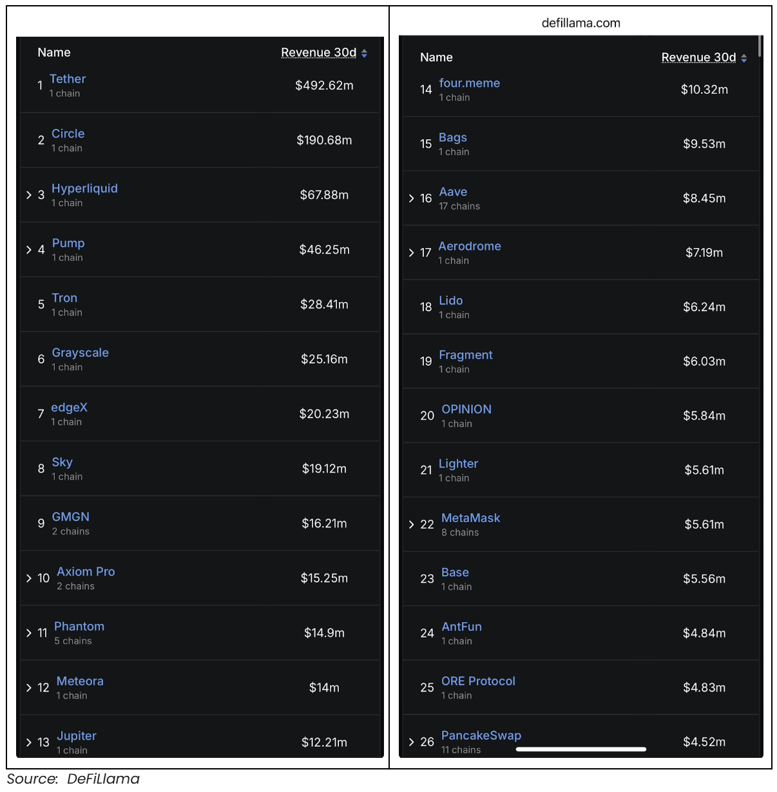

Well, here you go crypto industry. HYPE, PUMP, CC, and a host of other DEXs and lend/borrow platforms seem to kill it fundamentally during market routs. Below are the last 30-day revenues from top crypto companies and platforms. Notice a trend?

- Stablecoin issuers (i.e., Tether, Circle)

- DEXs (i.e., Hyperliquid, Jupiter, Aerodrome, Lighter, PancakeSwap)

- Lend/borrow platforms (i.e., Sky, Aave)

- Wallets (i.e., MetaMask, Phantom)

- Launchpads (i.e., Pump)

In my opinion, these are the more defensive sectors in digital assets.

Some of the founders of these companies are trying to highlight this. Aave announced that it liquidated over $140 million of collateral across multiple networks without any issues, in a fully automated fashion, demonstrating (yet again) that DeFi works and it is the market leader in protocol resiliency. Maple Finance similarly announced the success it is having in this market downturn. But it’s not enough to hear it from the horse’s mouth. We need the platforms that talk to investors to shout this from the rooftops, too.

The numbers are obvious and transparent. These businesses seem to print money. But for some reason, the industry leaders (exchanges, brokers, research firms, asset management firms, media) don’t seem to want to separate the wheat from the chaff. Worse, these same industry leaders want to try to convince you that "big" equals "defensive", as if hiding out in the biggest assets should keep you safe, even though the biggest assets are the LEAST defensive businesses in all of crypto. They either make no money (BTC), have massively reflexive downside usage (SOL, ETH), or are a flat-out joke (XRP, which is the exact opposite of HYPE—they dump billions of dollars of tokens on their users every quarter, and use the proceeds to buy back their stock). There is simply nothing defensive about a made-up currency with no cash flows, or a few L1s with cyclical usage.

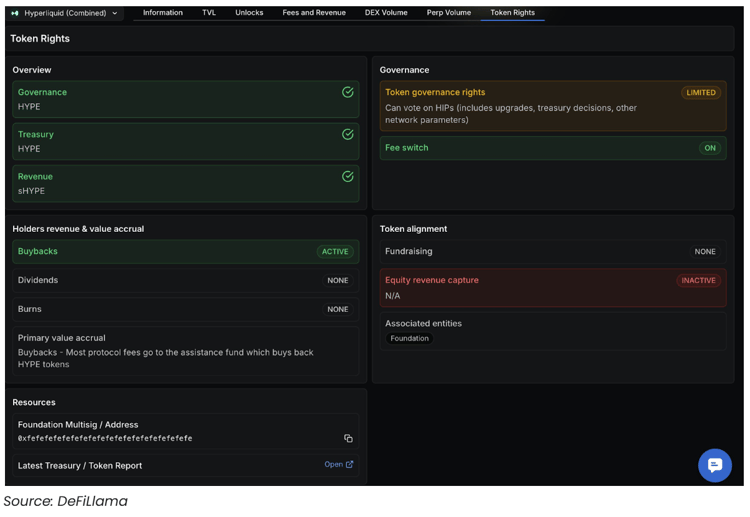

Fortunately, we’re starting to see some progress on the education and differentiation front. DeFiLlama wants you to know what a token actually does before investing. What a brilliant concept!

Does the token control governance?

Does it have any claim on the treasury?

Does it receive protocol revenue via buybacks or dividends?

DeFiLlama recently launched “Token Rights.” Token Rights gives you a clear, standardized view of what a token entitles holders to: revenue, treasury, governance, or none of the above.

This is fantastic. Every crypto broker and data source provider should integrate this ASAP. This industry simply cannot grow without proper education.

Not all tokens are created equally!

So let's stop pitching them as one giant macro trade, and instead start celebrating their nuances. And in a tough market environment like today, long live defensive tokens!