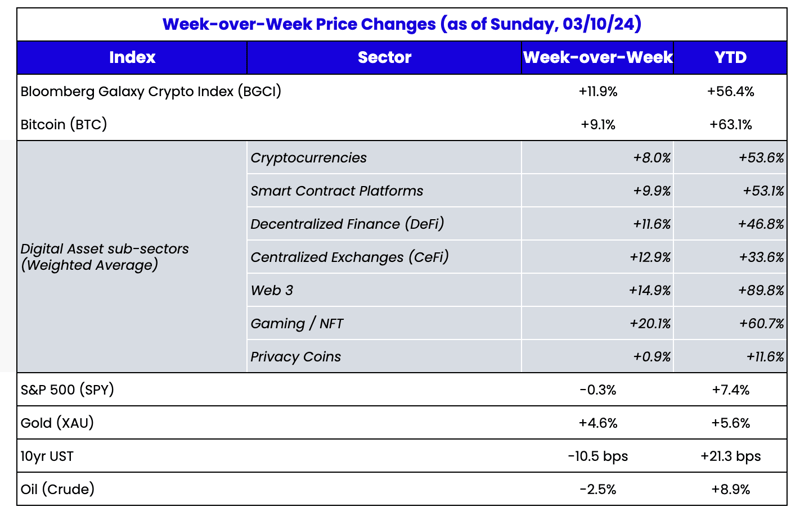

Source: TradingView, CNBC, Bloomberg, Messari

Source: TradingView, CNBC, Bloomberg, Messari

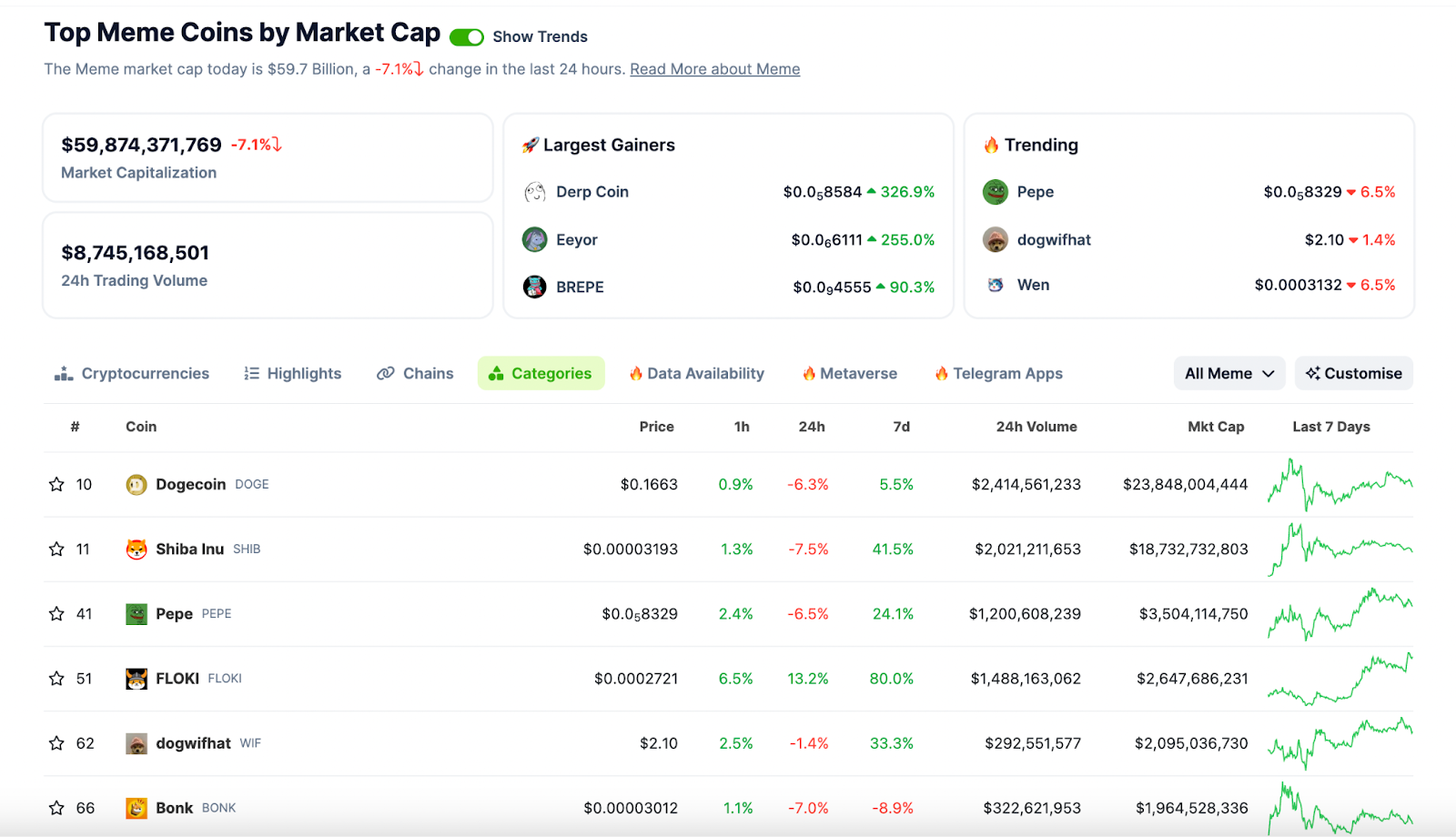

Memecoins are back, baby!

The digital assets market had another week of double-digit percent gains last week. After a slow start to the year, the market has gained pretty steadily since mid-February. There have been plenty of good reasons for optimism and continued strength. U.S. Treasury yields have begun retreating again amidst mixed economic data and undoubtedly dovish words from Fed Chairman Powell. Major global equity indices continue to hit all-time highs. The new Bitcoin ETFs continue to attract massive inflows, and trading volumes are higher than expected. New sectors within digital assets are emerging, with real usage and growth, particularly in gaming, AI, data availability and Bitcoin L2s. DeFi has received a bit of a “regulatory bump” following Uniswap’s decision to implement a fee switch. And dollar-backed stablecoins continue to grow, with Tether’s (USDT) market cap eclipsing $100 billion.

Yet one market area defies logic and scares some seasoned market participants who worry about euphoria. Memecoins are back! When we explain digital assets in layman's terms to new investors, including all the

different sectors and token types, we almost always ignore memecoins. It’s an area of the industry that is fun, sometimes profitable, and certainly unique, but it also invalidates some of the arguments about the valuation and value creation of digital assets. There’s no standard definition of memecoins, but essentially, they derive value purely from social and cultural excitement. As Galaxy Digital stated, “

Although some may have additional features, their primary offering is ownership of a coin that symbolizes a meme and fosters a sense of community”. But after this recent surge, the total market cap of memecoins is now almost $60 billion, with 6 different tokens in the Top 100 by market capitalization.

There are thousands of memecoins, because there is no barrier for entry to create and launch them, and it takes very little time and effort to develop a memecoin compared to more complex blockchain infrastructure and consumer applications. But very few have found traction. Memecoins can be found on every chain, and it is not uncommon for certain memecoins like DOGE, SHIB and WIF to be trending on crypto Twitter. And for good reason. The value in the memecoin comes from the social excitement itself. So yes, it’s concerning for memecoins to be at the heart and soul of this digital asset rally.

That said, the dare-I-say “more real” areas of digital assets are thriving as well, which seems entirely more healthy.

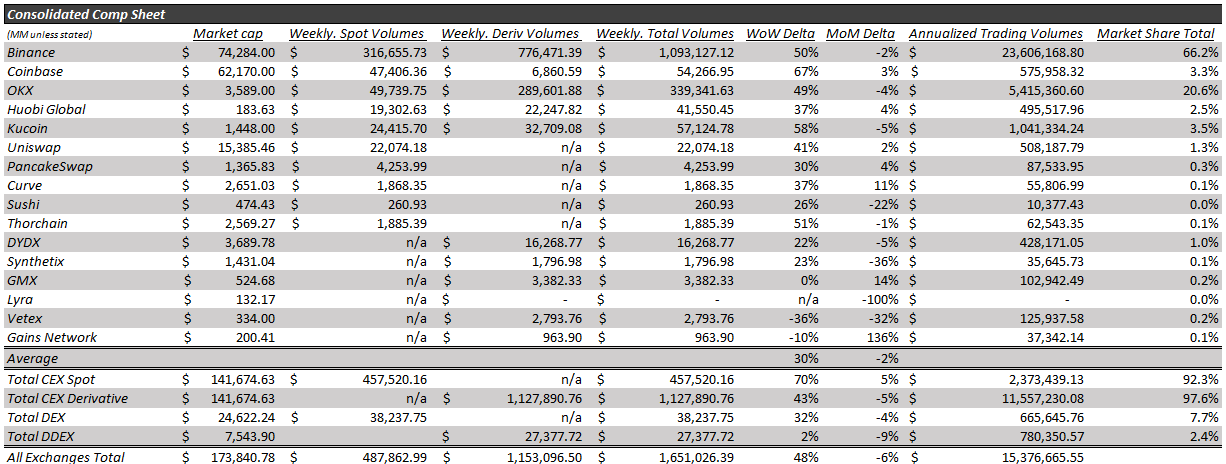

- While memecoin trading volume is exploding, so are total exchange volumes (inclusive but not limited to memecoins), which have continued to see significant growth with total volumes up 48% week-over-week.

- Centralized exchange volumes led the way with spot volumes up 70% WoW, and derivatives volumes up 43% WoW.

- Coinbase was the best performer, with total volumes up 67%, led by their derivatives business, with volumes up 83% WoW. COIN stock is naturally outperforming most tokens and is inching its way back to all-time-highs.

- Decentralized exchange volumes underperformed the broader exchange sector, but still saw volumes grow 32% WoW. Of the majors, Uniswap and Thorchain outperformed last week, with volumes up 41% and 51% respectively. Separately, there has also been a significant increase in on-chain trading volumes, which have surged, in part, due to a frenzy around meme coin trading. Volumes have more than doubled from $4.8 billion on March 2 to a peak of $11.5 billion on March 5. More than a third of this activity has actually been centered on Solana, which has increased its decentralized exchange (DEX) market share more than five-fold (from ~6% to ~30%) since the start of November 2023.

Source: Coingecko, Token Terminal, Dune, Artemis and Arca Internal Calculations

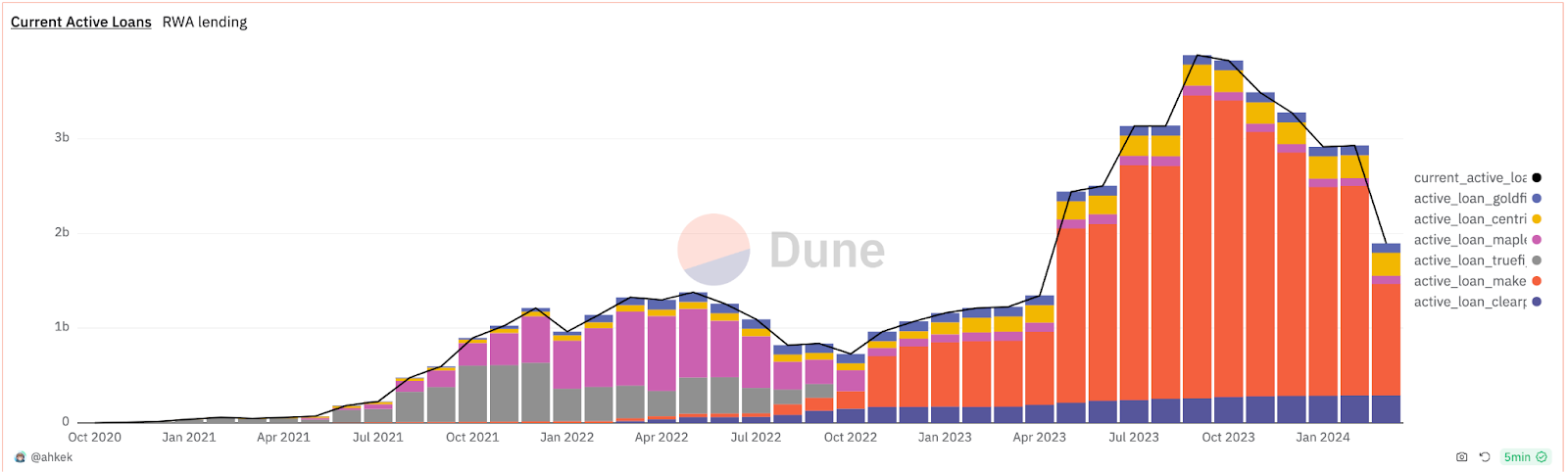

Perhaps most interesting, the rise in memecoins has taken a bite out of one of the more promising sectors, real-world assets (RWAs). And this is the problem with extrapolating narratives. Two months ago, real-world assets were all the rage. Now, RWA traction is declining because, with double-digit percent weekly gains and the excitement of winning the lottery via the next hot memecoins, there is simply a better use of capital than earning 4% sitting in U.S. Treasury bills via on-chain asset-backed tokens.

Source: Dune Analytics

So, where are we in the cycle?

We’ve spent a good part of the last 14 months discussing the parallels of this market to past market environments. On the one hand, it looks somewhat similar to the first 4 months of 2021, where every month has a new “sector du jour” (DeFi, Web 3, Gaming, then memecoins) on its way to a ferocious first half return and ultimate full-year triple-digit return. On the other hand, it looks closer to early 2020, when “altcoins” began to break away from Bitcoin after Bitcoin outperformed everything in 2019.

But perhaps comparing digital assets present to digital assets past is the wrong analogy. The Arca research team and CoinDesk made an astute observation this week.

After Bitcoin cleared its previous all-time high last week, a not-too-uncommon 10% selloff immediately followed. Some have mentioned that this looked similar to when the Nasdaq hit 5000 for the first time in March 2020, a bubble that took a decade before the Nasdaq retook the 5000 level a second time.

Source: Google Finance

But Coindesk pointed out that Bitcoin’s first rise to the $69,000 peak in 2021 was much more likely to be analogous to the March 2020 Nasdaq 5000. Both involved cheap money, big parties, and euphoria, whereas last week’s rise back to Bitcoin all-time highs felt more like “let's just get this out of the way and get back to work". Meaning, the 10-year Nasdaq bear market rebuild might have happened to digital assets in just 18 months from mid-2021 to the end of 2022.

And we all know what happened to the Nasdaq after it finally reclaimed the all-time highs again in 2017… a more than 3x rally over the next 7 years. Here’s hoping history repeats itself.