Source: TradingView, CNBC, Bloomberg, Messari

Tech Up / Crypto /Flat

Meta beat earnings

Amazon beat earnings

Microsoft beat earnings

Google beat earnings

Apple beat earnings

The “Magnificent 7” added a combined $3 trillion

market cap in 2024. Meta alone added $200 billion in market cap in a single day following its 4Q earnings and dividend announcement - the biggest one-day gain for any public company in history!

There were, of course, plenty of other less positive events last week, too. Regional bank stocks are suffering again, pushing KRE down 10%, many large companies are announcing layoffs even as the overall economy adds jobs, and the Fed struck a hawkish tone as Powell pushed back on expectations for a March rate cut. Powell reiterated that the Fed needs "greater confidence" that we are on the path to 2% inflation and hedged hawkish commentary with "we are not looking for better data but continuation of the better data."

But it’s pretty hard to fade the market in a meaningful way when the largest tech companies in the world continue to blow the doors off of expectations.

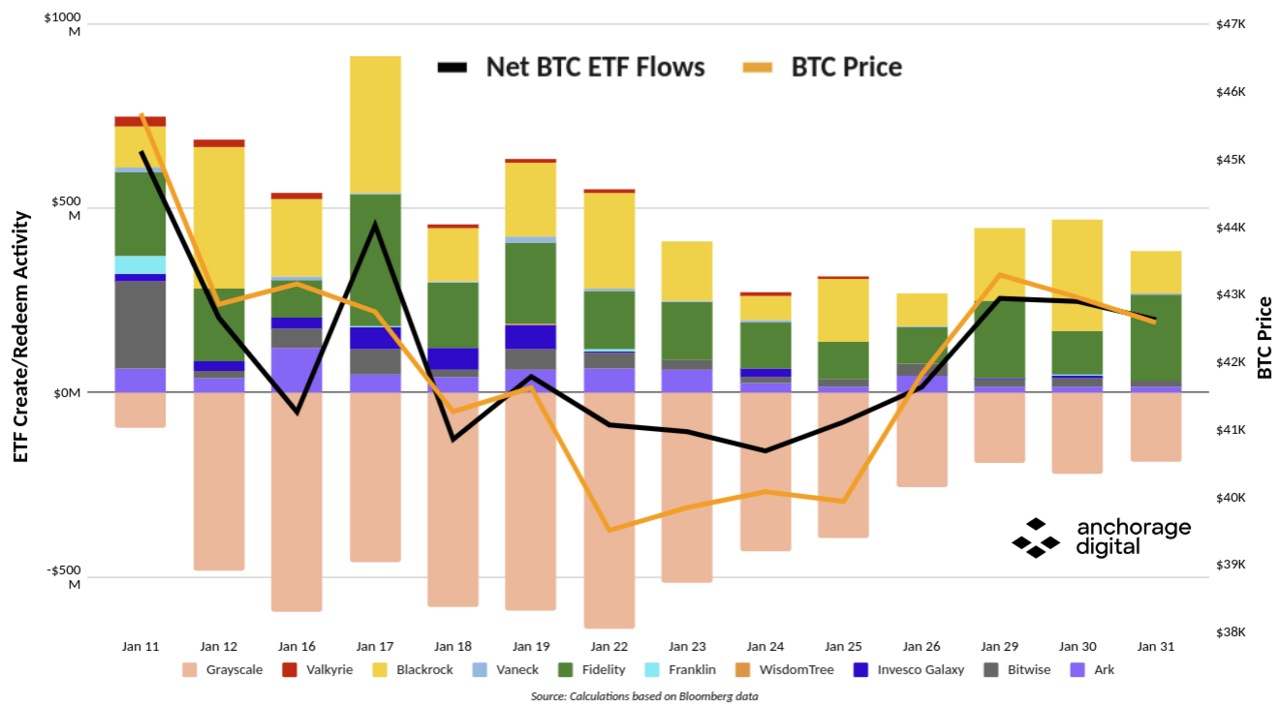

That said, digital assets continue to disregard both tech and the overall economy, which is a good thing even if it means lagging recent strength. The new Bitcoin spot ETFs continue to warrant most of the market’s attention, as trading volumes have been nothing short of spectacular.

As our friends at Anchorage pointed out, Bitcoin's price has been very correlated to the net ETF flows. While the outflows from Grayscale have continued, they're trending lower and have been overcome by the new ETFs' inflows.

- Last week +$701M net (Grayscale = $600M outflow, new ETFs = $1,301M inflow)

- Prior week -$417M net (Grayscale = $2,234M outflow, new ETFs = $1,817M inflow)

Source: Anchorage

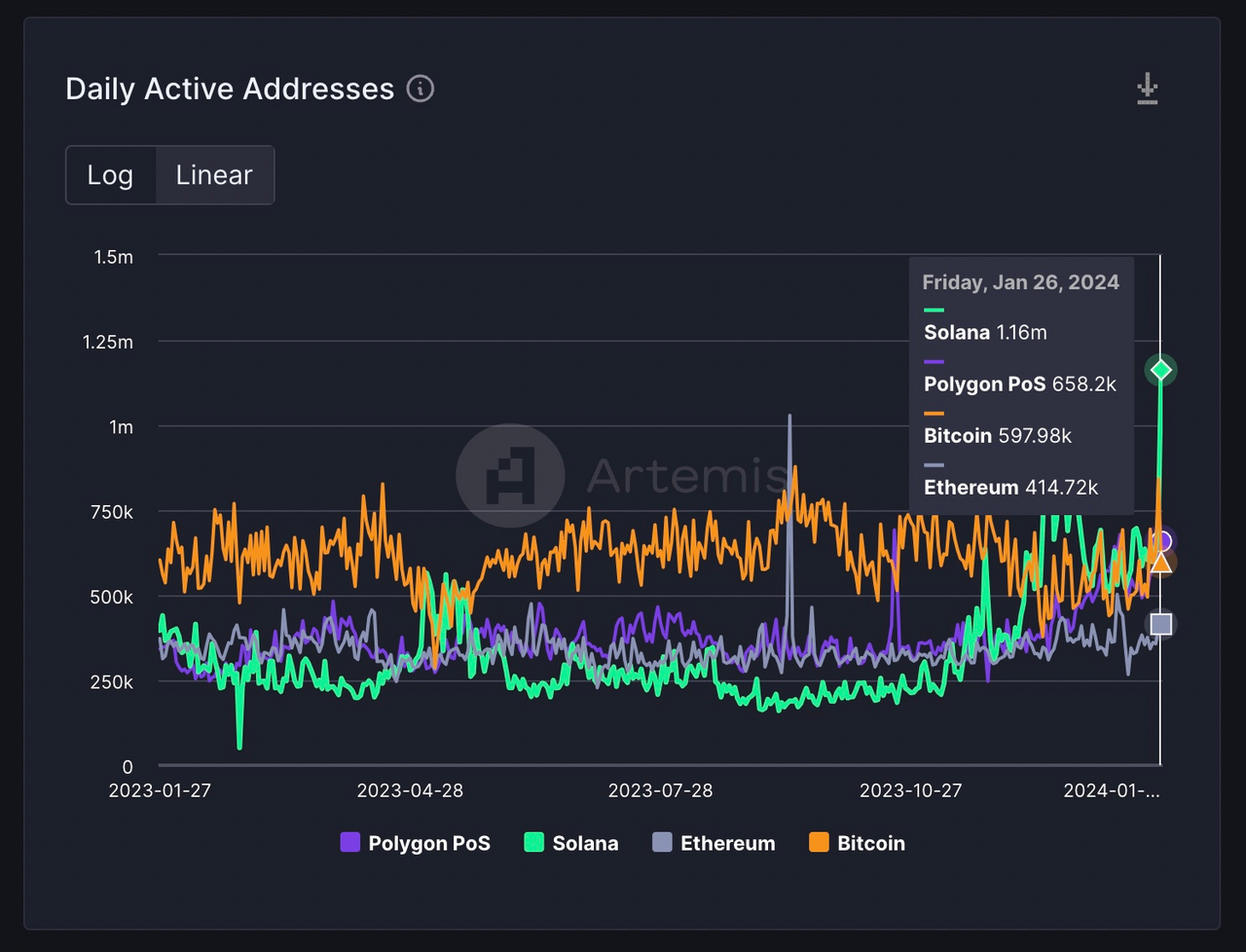

But just as the rest of the equity market isn’t really keying off the Magnificent 7, the digital assets market isn’t keying off Bitcoin. Gaming remains strong, with IMX +7% and RON +30% WoW. Oracles are trading well, with LINK and PYTH +20% each. And the Solana ecosystem is once again getting a boost from airdrops.

Another Airdrop Raises Questions About Capital Markets Efficacy

“Airdrops are quite possibly the easiest way to learn about the mechanisms driving the crypto ecosystem and earn rewards for participating, thereby increasing your wealth. For anyone even remotely intellectually curious about digital assets and blockchain, we recommend figuring out how to participate in airdrops. Numerous other airdrops will happen in the coming months, and all you need to do is participate in the protocol to reap the benefits.”

Right on cue, the next installment of Solana airdrops hit the market last week with the launch of the Jupiter (JUP) token. Jupiter is Solana’s leading decentralized exchange aggregator, and this was one of the largest airdrops ever. The elevated blockchain activity that occurred post-airdrop represented an important stress test for the Solana blockchain. Although some individual nodes were overloaded, there was no widespread blockchain halt, showcasing quite an improvement over the many outages Solana suffered in the early days of the protocol. In short,

Solana passed an important test.

The JUP token itself traded $1.4 billion in volumes on its first day, and the token immediately jumped into the Top 100 by market cap. However, as usual, market makers and retail investors mispriced the airdrop on the break, and the price has gone straight down since the initial hours of trading. And of course, when the price goes down, there is controversy. Some token holders complained about how the token launch pool was used by the team to sell tokens to the public – in essence,

turning an airdrop into an ICO.

Controversy aside, Solana has established itself as a real emergent in blockchain. Beyond its technical strengths, Solana's ecosystem has drawn in thousands of new wallets due to various airdrops over the past months from projects like Jito Network (JTO), Pyth Network (PYTH), and now Jupiter (JUP).

Source: Artemis

But are airdrops actually a healthy way to create or distribute value? Quite frankly, with proper disclosures, an ICO may have been better, as people generally value something based on what they pay for it.

Let’s start with the word value. We’ve been fighting this battle for years, but value does not necessarily only mean the present value of discounted cash flows. There are three forms of value:

- Financial value - similar to present value math for bonds and equities, an asset's financial value is driven by an entity's cash flows and the promise of distribution of these cash flows.

- Utility value - The ability to spend or use this asset. For example, airline miles, Starbucks points, gas tokens, token collateral, etc.

- Social value - From meme stocks to Nike shoes to the incredible enthusiasm and staying power of blockchain communities, there is value in “being a part of something cool”. The feeling of common affection for something is a durable source of motivation—far more so than communities of critics who typically dissipate before long because it’s not that fun spending your time hating something.

The new JUP token has immediate utility. You can already use it as collateral to trade leveraged perp futures on Drift. You can also borrow against it in lending protocols like Solend and MarginFi. There is probably also social value for JUP, as it was dropped to a community of early adopters who share in their early belief of the protocol (at least those who weren’t just callously farming for tokens). But the JUP token has no financial value, at least in its current form.

Utility and social value were enough to turn something that didn’t exist on Tuesday into a token now worth over $700 million in market cap. Marex Digital asked the right question in a blog to subscribers:

“Did Jupiter “create” money or simply redistribute existing value? Are airdrops more like helicopter money or an equity distribution?”

It’s a good question. It appears we’re still operating under the “social consensus” zeitgeist, where the value captured is secondary to proxy value. Jupiter is one of the best protocols and should, therefore, command tremendous proxy value. For now, utility value and social value may be enough.

That said, when a token goes straight down, you can’t call this a screaming success. There is a good reason why IPOs generally go up. And there is a good reason for why BNB, ETH, and BTC are 3 of the most successful protocols today. When you price an asset low, and let early investors participate in the financial upside of your success, it tends to have long-lasting positive effects. Your users become power users and evangelists. But when something prices high and goes straight down, you alienate those who were true believers. And it’s hard to come back from that.

It remains to be seen if the JUP token recovers, especially when the next Solana airdrop comes to market and airdrop mercenaries shift gears from JUP to the next one. As impressive as the Solana blockchain has been recently, the capital market's antics of the supporting ecosystem leave a lot to be desired. From heavy VC concentration to FTX’s stranglehold, to low float/high FDV launches, to the endless mispriced airdrops… Solana project developers continue to look a gift horse in the mouth with poorly constructed token launches and bad capital markets advice.