Source: TradingView, CNBC, Bloomberg, Messari

A Breakout

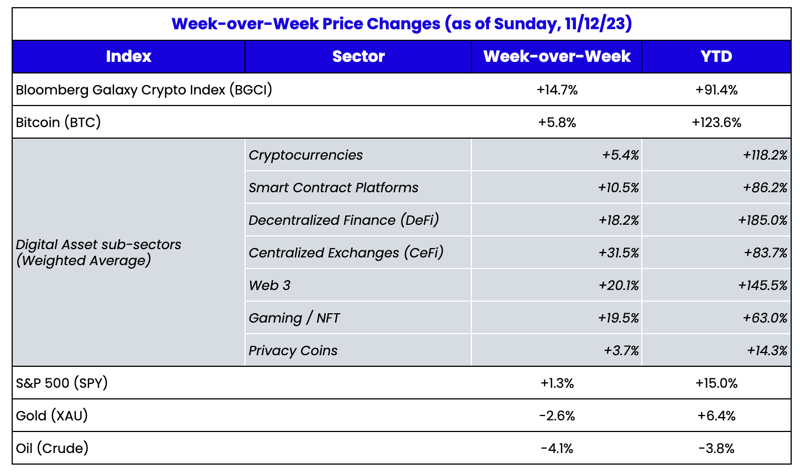

For most of this year, we’ve struggled to find anything worthy of writing about besides Bitcoin. Seemingly all newsworthy events have directly impacted Bitcoin including the regional banking crisis, Blackrock’s ETF application, and spiraling global government debt and interest expense. BTC is up +118% YTD, and up until this week, was one of the best performing digital assets. But that has changed quickly. Unlike the end of October, where strength was led by Bitcoin, Bitcoin lagged the broader market this past week. It didn’t hurt that equities continue to rise, and

Blackrock filed for an ETH ETF. But last week was not really about ETH either:

- Layer-1 protocols were led by AVAX (+38%) and SOL (+37%)

- Layer-2 protocols were led by MATIC (+19%)

- DeFi was led by DYDX (+25%),

- Gaming was led by ILV (+40%)

In total, over 100 tokens in our coverage universe gained 10% or more in the week.

A few months ago we wrote that only a handful of sectors/tokens were actually moving higher, but those that were generally had legitimate reasons for their ascents. This past week, that’s been less true. Price seems to be leading activity versus fundamentals leading price – the tail is wagging the dog. Once the price starts to move, however, we begin to see transaction volumes increase, DeFi activity increase, developer activity increase, VC funding increase, and constant announcements. The reflexivity that caused so many problems in 2022 is now working in the market’s favor.

Meanwhile, we continue to see

steady inflows into Bitcoin and record Bitcoin trading volumes and open interest at the

CME, suggesting the institutional bid ahead of an ETF remains strong.

This type of price action has historically been an inflection point. Either greed and leverage grow too fast and the market ultimately resets, or shorts/cash continue to get left behind as both retail and institutional interest pours back in. For the moment, it appears to be the latter.

A Bittersweet Outcome to Aragon’s Governance Debacle

High level, Aragon is a 2017 project that hasn’t captured much success, and any success they did capture did not translate into token value accretion. Because Aragon issued a token to fund the project, we believe Aragon has a fiduciary duty to deliver some value back to token holders. In May, we wrote an open letter to Aragon token holders outlining our desire to work with the Aragon team to help find a solution to return ANT to book value. Since then, a back-and-forth discussion occurred taking a significant amount of time and undergoing various forms including a buyback proposal from a co-founder, our buyback proposal, and a potential sale of the project. Though conversations started a little contentious, it ultimately became a constructive and healthy debate on how a project like Aragon could continue without dragging token holders down. Ultimately, the Aragon Association has settled on the following restructuring plan.

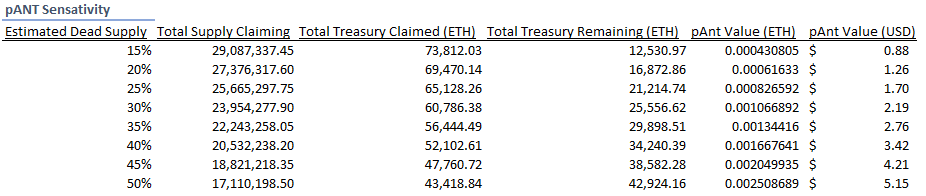

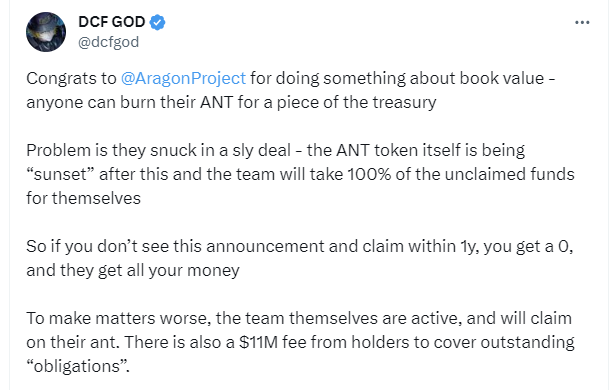

To summarize the plan, their treasury will allow ANT holders to redeem their ANT for ETH and dissolve the Aragon Association. However, if you examine the restructuring plan, any outstanding treasury not claimed within one year will go to the private entity of Aragon. Given how old the ANT token is, it is likely that tens of millions of dollars will not flow back to token holders since many might have lost their private keys or not know that they need to claim their ANT.

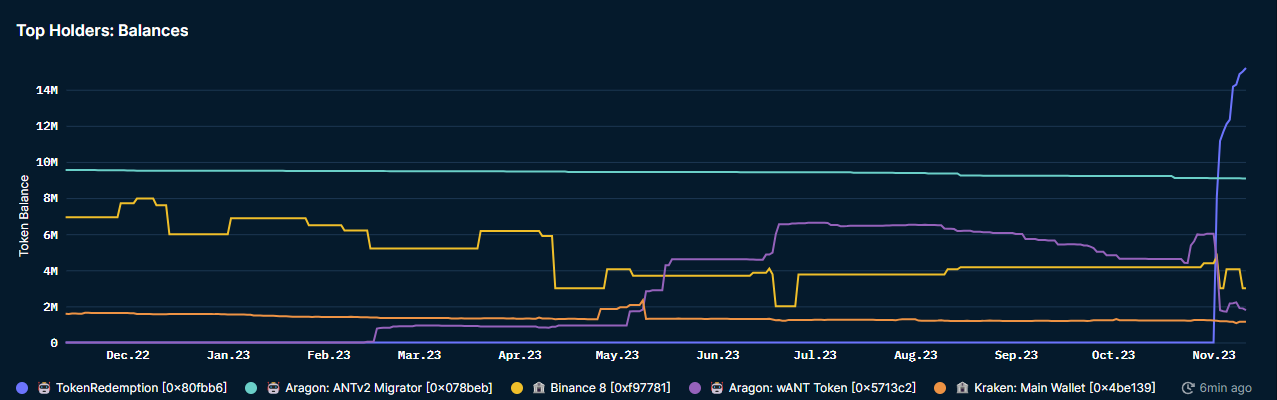

The issue is not that $11 million of treasury assets are being withheld for outstanding obligations, but rather that the go-forward private entity of Aragon will receive all of the outstanding treasury that is not claimed after one year. Given how old the ANT token is, this is likely to be multiple tens of millions of dollars that will not flow back to token holders. For instance, the largest ANT holder outside of the migration contract is the ANT v1 to v2 migration contract with 9.089 million ANT, or roughly 27% of the total supply that has a claim on the treasury. Because this holder didn’t migrate their tokens over the past 3 years, it is likely that these tokens are “lost”, and will redeem at a lower rate than ANT already migrated.

This is not to say that v1 ANT holders shouldn’t have a claim on the treasury, but rather to highlight just how many tokens are likely lost if 27% of the supply with a claim did not transfer over to the ANT v2 token, despite the migration being open since 2020. Because of this, we believe that 25%-35% of the supply will not be redeemed via the restructuring tender, and the go-forward private Aragon company will walk away with the $11M held back for obligations PLUS between $43.5M and $61.4M from the unclaimed treasury funds in a year. On top of that, Aragon raised its ICO in ETH and still maintains a significant portion of its treasury in ETH, meaning that its co-founders and employees continue to benefit from rising ETH prices rather than the project’s success. In addition to this potential upside, Aragon employees received an accelerated vesting schedule over the years, which employees can claim against the redemption. If employees receive equity in whatever new company is formed, and this new company dissolves within a year after the redemption, the team is in for quite a payday.

The amount of value that may ultimately be retained by the team and not distributed to token holders is staggering. Because of this, it makes more sense to consider a second redemption with unclaimed funds after a year, similar to pROOK.

We are pleased to see this year-long governance process end and appreciate that Aragon took responsible action by returning funds to ANT token holders. However, as you can tell, this deal is unfair to token holders.

This is precisely why token holders are pushing for a second redemption and even secured a $300K claw back to pay for a recent community snapshot vote that passed to claw back the $300K transferred to the DAO as legal funds to pursue this avenue. Given that ANT is trading at approximately 1% over the redemption price, the market is giving some validity to the possibility of this lawsuit succeeding. This will be interesting to see play out, but as of now, ANT is akin to a free legal call option with a one-year expiry.

The community only has two choices:

- Take a less-than-fair deal

- Fight

Some token holders are choosing option 2. Aragon took a lot of money from people and now gives them back a lot less. From the community's perspective, it's just simple math -- investors gave Aragon 275,000 ETH in exchange for ANT in 2020, and ANT has fallen 75% in value versus ETH, and now Aragon is giving them back only a fraction of that ETH. I suppose that would be fine if that were truly all of the assets Aragon had left to give them -- but it's not. The Aragon team received a lot of money over the years in salaries (funded by token holders), and the team was gifted ANT tokens (which is now getting ETH back via this liquidation at the expense of paying token holders), and on top of that, the team is getting all of the upside from any ANT that is not redeemed.

The community might accept this deal if the process were open and transparent through governance. But the fact remains that there are a lot of open questions that have not and likely will not be answered.

Arca was one of the leaders of this year-long "governance" process. And while we were not involved with structuring the final terms, we repeatedly offered our guidance to Aragon, in constructive and friendly ways. Our advice, in essence, can be summed up as, "Don't get too cute -- because if you try to get too cute, it will cause more headaches than whatever value you try to squeeze." There was an easy path - give token holders more than they valued ANT- and a challenging path - squeeze every penny out of the community.

It seems Aragon chose the hard path.