What happened this week in the digital assets markets?

What happened this week in the digital assets markets?Week-over-Week Price Changes (as of Sunday, 6/28/20)

|

|

WoW

|

YTD

|

|

Bitcoin

|

-2.5%

|

+26%

|

|

Bloomberg Galaxy Crypto Index

|

-3.0%

|

+29%

|

|

S&P 500

|

-2.8%

|

-7%

|

|

Gold (XAU)

|

+1.5%

|

+14%

|

|

Oil (Brent)

|

-2.0%

|

-39%

|

Source: TradingView, CNBC, Bloomberg

Risk on, Risk off. Covid-19 is gone, Covid-19 is back. V-shaped recovery, global depression. The narrative du jour continues to push all asset prices in the same direction, and last week the narrative was negative. Correlation is rising again between Bitcoin and equities, and while this is likely a non-factor long-term, it is driving price action today.

Where Digital Assets Fit in a World With Unstoppable Equity and Debt Gains

Needless to say, these are strange times. The founder of a sports blog is outtrading and publicly mocking investment legends. Global credit and equity markets are rising amid a global pandemic, social unrest, record unemployment and the fastest recession in history. And the Fed is buying everything that isn’t nailed down, including the bonds of companies with the best balance sheets and easiest access to capital. This of course leads to common chants of “Don’t Fight the Fed” and “Modern Monetary Theory is theft” and “Capitalism is dead”.

All of this may be true, and it may not matter. Torsten Slok, Chief Economist at Deutsche Bank, laid it out perfectly, as he stated all of the problems that don’t matter, until they do:

“Modern Monetary Theory assumes that the Fed can purchase all Treasuries with no consequences. But the risk-free asset is used to price all private sector assets such as the S&P 500, IG, and HY credit. Put differently, the result of the Fed buying all Treasuries – and now also IG and fallen angels – is that the Fed ends up controlling all asset prices. As a result, pricing in stock markets and bond markets no longer reflect the true default risks of individual assets. And if prices of government bonds, credit, and equity are no longer a correct reflection of the true default risk in these asset classes, then it ultimately increases the likelihood that investors, including foreigners, no longer want to buy any public or private sector asset in the country doing MMT. Looking at it from the finance textbook, MMT assumes that undermining the assumptions about what a risk-free asset is will have no consequences for the currency and demand for private sector assets. As we know from history, countries that have monetized their debt have not only seen consequences for government bond interest rates but also for demand for private sector equity and credit, including from foreigners. In short, if you assume that investors don’t care about whether the price of Treasuries, credit, and S&P 500 is a true reflection of the underlying default risks, then MMT works. Or rephrasing the old IMF saying about countries growing government debt levels: MMT works until it doesn’t.”

Naturally, even the most bullish investors remain somewhat cautious with regard to when all of this unwinds. And there are some positive outcomes emerging from the chaos, starting with a few leading companies choosing society over shareholders by pulling back on Facebook ads. But until the music officially stops, maybe the Dave Portnoys of the world have it right… just buy debt, equity and real estate with both hands and no regard for valuation.

For those of us who actually care about valuation, however, perhaps we need to look elsewhere, like some of the creative financings that are popping up as a result of the pandemic. According to an SEC filing, United Airlines "expects to have approximately $17 billion of available liquidity at the end of the third quarter of 2020, which includes $5 billion of committed financing to be secured by the Company's loyalty program." Monetizing airline loyalty miles sounds eerily similar to what we’ve been saying for years about how companies can use digital assets as a new part of their capital structure. This is just the beginning. I truly believe that one day soon every company with loyal users like Starbucks, Facebook, Costco, Amazon and Disney will issue digital assets as part of their capital structures.

So it comes as no surprise that growth stocks are trouncing value stocks right now, as earnings no longer matter (and in many cases no longer exist). Yet it may surprise you that the opposite is true in digital assets, as almost all of the recent growth in the market (and investor gains) is coming from value tokens. The highest flyers year-to-date are from companies and projects where the tokens accrete real economic value, and these companies are also the ones attracting the most user and revenue growth.

The Four Types of Digital Assets

Yes, digital assets can be valued, at least some of them. In our opinion, there are now four types of digital assets, and the fourth one is the most interesting, albeit the least well known:

- Cryptocurrencies / Money -- These are decentralized tokens that aim to be a store of value, or a medium of exchange. By market capitalization, they dominate the digital assets world, and thus the mainstream media coverage and the popular vernacular. But there are actually very few cryptocurrencies, most of which are not investable or at all interesting. Bitcoin of course is the most dominant today, but the faster you look beyond cryptocurrencies, the faster you’ll learn what this asset class really offers.

- Decentralized protocols and platforms - Like cryptocurrencies, these are often talked about, but largely misunderstood because they are incredibly complicated. Ethereum is the only one that has real traction with regard to growth and users, while the rest are being built or playing catch up (examples include XTZ, ADA, EOS and ALGO). Whether or not the tokens associated with these blockchains accrue economic value remains to be seen, and therefore stir up the most debate and the most bifurcated reactions from investors. But these are almost impossible to value.

- Asset-backed tokens - These tokens barely exist yet, but are coming to market quickly. Tokens backed by equity, debt, legal contracts, and hard assets are coming, with major financial firms and individuals beginning to explore issuing these types of assets because they are cheaper, more efficient, or open up new forms of asset purchases. From Spencer Dinwiddie’s NBA salary backed token, to SocGen’s debt-backed tokens, to TokenSoft’s equity-backed tokens, you will soon be able to own traditional assets without a bank or brokerage account.

- Pass-through securities - Perhaps the least known, and most interesting part of the digital assets market, these are flexible token structures issued by real companies that can seemingly serve any purpose. In some ways, they are similar to SPACs (special purpose acquisition companies), or black boxes where you put your trust in the management team. On the one hand, this may give investors pause as they prefer a very straightforward definition of an investment (i.e. bonds are claims on assets, equities are claims on profits). On the other hand, this is the most dynamic investment structure ever created, as companies can pass through revenues, profits, user growth or rewards all in one investment vehicle. You get to back a good company and management team, but reap the rewards later as the token use case isn’t set in stone on day one. We’ve seen tokens issued by leading digital asset exchanges that are quasi-equity / quasi-utility tokens in that they amortize the tokens using a percentage of revenues, while also giving owners of the tokens discounts to use their product (examples include BNB, LEO, HT and HXRO). We’ve seen DeFi tokens that allow you to earn additional tokens for “staking” tokens on the network as a reward for providing network security, liquidity or participation in governance (examples include SNX, COMP, KNC). There are NFTs (non-fungible tokens) which give you digital rights to unique assets (examples include Topps issuing digital garbage pail kids cards and MLB offering digital collectibles). And we’re starting to see non-digital asset native companies begin to tinker with digital tokens that serve their communities (examples include Reddit and Atari tokens).

This last subset of the market is now by far the most interesting and valuable part of the digital asset investing universe and is largely ignored or unknown.

In the next few weeks, we are going to take a break from Bitcoin and the macro narrative and will try to shed some light on this growing and exciting part of the digital assets market.

Socios offers Chiliz (CHZ) Tokens For Fan Engagement and Entertainment

How often does a great product idea find immediate product-market fit and also come with immediate and liquid investment gains? That is the very nature of “Pass-through” tokens.

Fan Tokens can be purchased on the Socios app using the native Chiliz (CHZ) token, with Fan Token Offerings (FTOs) and Fan Polls conducted on the blockchain, making results verifiable. To date, Socios has held FTOs for soccer clubs Juventus (JUV), FC Barcelona (BAR), AS Roma (ASR), Atletico de Madrid (ATM) and Esports team OG (OG). There are many others in the pipeline as well including a partnership with the UFC.

After Fan Token Offerings have concluded, FTOs are immediately tradeable in the secondary market, with CHZ acting as the only available trading pair. As such, there are three separate investable opportunities:

- The illiquid but valuable private equity of the company which effectively underwrites the tokens (Socios)

- An all-encompassing, limited supply, valuable token that gives you the rights to purchase these tokens (CHZ)

- Individual tokens of the teams and leagues that you love (various FTOs)

There is an inherent demand for CHZ tokens that coincides with demand for fan tokens. Further, this is a pass-through token as CHZ has a deflationary supply mechanism, in which tokens are burned based on revenue from various channels:

- 20% of the net trading fees on the Chiliz exchange

- 10% of CHZ used to purchase tokens in FTOs

- 20% of net proceeds for NFT and collectible sales

Last week, Socios and Chiliz held an FTO for FC Barcelona’s token (BAR) which sold out in less than two hours with token proceeds of $1.3 million. The results are not surprising given FC Barca’s 450 million global fan base and FC Barca’s promotion of the sale to that fan base in the days leading up to the sale. Besides the impressive sale and secondary listing, the FTO received coverage from mainstream media like the Washington Post and AP News, further cementing our thesis that products like Socios/Chiliz are what will bring digital assets to the mainstream.

.png?width=512&name=unnamed%20(28).png)

The CHZ token is +68% YTD as Fan Tokens have exploded on the scene. The BAR token priced at $2.25, opened at $2.54, and quickly traded above $6, with $2M+ of exchange volume. Every other FTO has increased in value since being issued as well. Not bad for a new concept, with an early-stage growth opportunity that is immediately liquid.

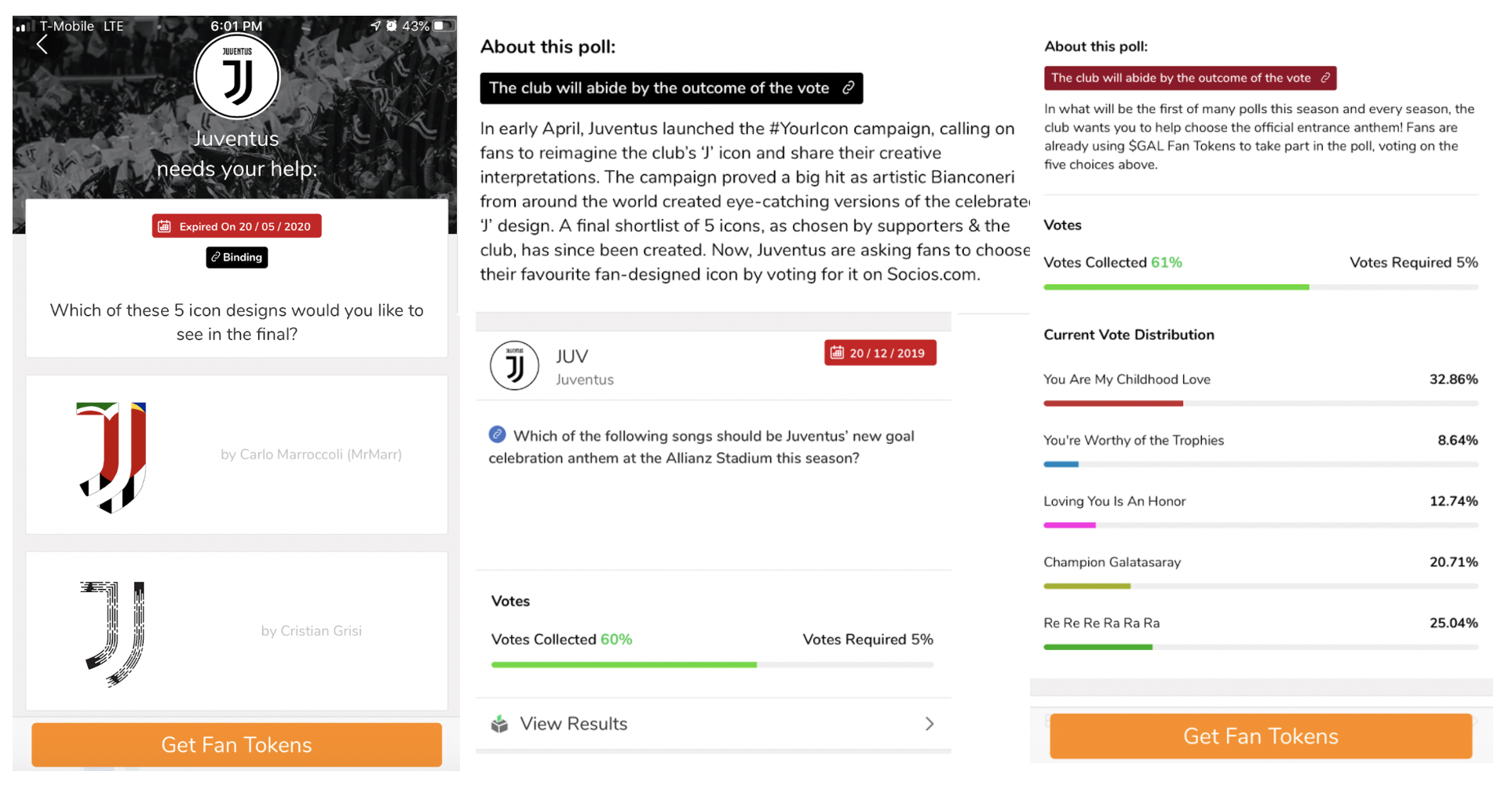

But Socios/Chiliz is not a one-trick pony. The sale last week was preceded by high engagement on fan polls, which are actually substantial decisions that fans get to participate in. For the first FC Barca poll, fans get to choose an inspirational message for inside the Barca dressing room. Recent polls for Juventus asked for feedback on the logo design for a special edition t-shirt and which song should play when the team scores a goal in the home stadium. Fan engagement is incredibly high -- sometimes 40%+ on these polls, proving real demand and product-market fit.

Source: Socios Mobile App

So what’s next for Socios and Chiliz? They have announced a partnership with UFC as their next frontier, but what if they come across the pond and issue tokens for NBA and NFL teams? With the in-game experience pretty much dead right now, one can imagine a mad dash to participate in polls for their favorite teams. When we do return to normal games and live audiences again, there’s the additional opportunity for special fan experiences based on the number of tokens each fan owns. There are endless possibilities for teams to engage with their fans in this way. And tokens don’t have to be limited to sports - the entire live events segment could tokenize its fanbase ...imagine if we had a Beyonce coin.

.png?width=512&name=unnamed%20(23).png)

Flexible, pass-through securities are likely the best way to utilize digital tokens within the capital structures of real companies and real revenue streams. Their investment value can be quantified and modeled, and their growth is real today, not perpetually “in the future” like cryptocurrencies and platforms/protocols.

While the media may want you to believe that Bitcoin, cryptocurrencies and decentralized networks are the only thing happening in digital assets, real investors in this asset class are focused on value creation.

Notable Movers and Shakers

The most notable event of the last two months has been the surge in the Decentralized Finance (DeFi) sector, which has posted impressive gains while simultaneously showing extraordinary growth in all available metrics. What stood out last week is that for the first time since May, we saw a bifurcation within the sector - some continue to surge, while others have notably not been able to keep the pace:

- The leaders: Celsius (CEL, 55%), Synthetix (SNX, +29%), Ren (REN, +28.5%), Bancor (BNT, +22%) Chainlink (LINK, +7%), Melon (MLN, +5%)

- The laggards: Compound (COMP, -19%), Aave (LEND, -17%), Kyber Network (KNC, -15%), Maker (MKR, -13.75%), Numeraire (NMR, -12.5%), Augur (REP, -8%).

What We’re Reading this Week

PayPal is exploring how to add support for cryptocurrency buying and selling to its platform of 325 million users. The move makes sense given Square’s Cash App foray into digital assets with Bitcoin trading and incremental purchasing features. Notably, PayPal withdrew from Facebook’s Libra project last year but is reportedly still interested in pursuing digital assets for its platform. Cryptocurrency support by the FinTech giant would be another boon for adoption, bringing more users and investors into the space.

Five years ago, the New York Department of Financial Services (NYDFS) created the BitLicense for entities seeking to transact in digital assets in New York state. The BitLicense has long been a point of contention for crypto startups as it places a large regulatory burden on small businesses and has stemmed business growth in the state. Last week, the NYDFS said it would consider easing some of these regulations including issuing conditional licenses to startups partnering with existing licensed businesses and finalized guidance on the listing of tokens for those holding a BitLicense. The move is a bid to lure more startups to the Big Apple and could indeed succeed as there have been calls to reform the BitLicense regulatory burden for years.

Last week, big four auditing firm KPMG released its KPMG Chain Fusion product that allows customers to collect data from blockchain-based and traditional financial systems for reporting purposes. Specifically, the product aims to help firms stay in compliance with financial reporting and security needs. Use cases include querying data from blockchain transactions to ensure they match up with the books and records that are maintained by entities - a process that would be helpful in audit scenarios. In a market that is incredibly fragmented and requiring many tools to run simple operations, Chain Fusion is a necessary advancement.

Bitcoin ATM operator LibertyX is rolling out Bitcoin purchasing options to 20,000 retail stores across the US including major chains such as CVS, 7-Eleven, and Rite-Aid. The service allows users to purchase Bitcoin using cash at the retail counters of these stores with the Bitcoin then being transferred to their digital wallet. LibertyX already has 5,000 Bitcoin ATMs nationwide and this new rollout further expands its reach and ability for individuals to purchase Bitcoin more easily.

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - Trader

Wes Hansen - Head of Trading & Operations

To learn more or talk to us about investing in digital assets and cryptocurrency