There are a myriad of issues preventing established investors from entering the digital assets space, like market illiquidity, price discovery issues, underlying valuations, and lack of infrastructure. But these same issues are seen in other asset classes as well. A proper narrative and realistic expectations can help investors better understand how to view this new asset class, and therefore help them gain exposure comfortably.

While digital assets are often compared to highly liquid markets like Oil and US equities, we believe digital assets make a lot more sense when viewed through the lens of more illiquid markets, namely High Yield bonds (HY) and Emerging market bonds (such as Bonds vs Bitcoin).

Below we outline the similar characteristics we see between the HY bond market and digital assets:

Similar Evolutions

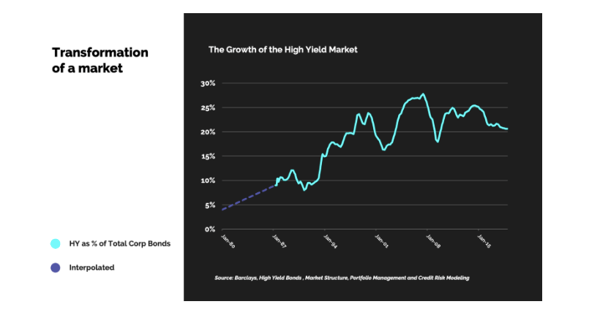

HY: High yield bonds were mostly irrelevant for decades and not widely used until a viable application was found. In fact, the derogatory “junk bond” moniker tells you all that you need to know about how people felt about this market in the early days. But in the 1980s, Michael Milken (via Drexel Burnham Lambert) famously figured out how to use this debt to finance leveraged buyouts. With this new use case, the HY bond market flourished with new companies financing themselves that previously had no access to cheap capital.

Digital Assets: The perception of digital assets is quite similar, where “junk” would be a euphemism for many investors’ true feelings. Digital assets still haven’t had their “Milken moment”, but large financial firms and a vast amount of intellectual capital are flocking to the blockchain space at a rapid pace. Viable applications for digital assets and blockchain technology are right around the corner, and companies and projects are finding sources of capital that were previously unavailable. Growth in this market will look very similar to that of HY, as more and more companies rush to this market to finance their visions.

High-Risk, High Reward Investments

HY: Junk Bonds were high-risk, high-reward investments that provided additional value beyond government and investment-grade debt. It took decades of data before investors were able to appropriately model where this asset class fit within their overall portfolio construction.

Digital Assets: Digital assets now occupy this role in an investor’s portfolio. To achieve higher returns, investors must accept higher levels of risk, but these risks can be quantified over time with longer track records and more data points.

Multi-Function OTC Desks

HY: OTC desks dominate the trading flows of HY & Emerging Market bonds, and these desks provide a valuable service in addition to just price and liquidity (underwriting, research, price discovery, etc).

Digital Assets: Similarly, many full-service digital assets firms now offer more than just OTC trading services like providing market color, research, and ancillary services. Further, these firms help investors eliminate much of the exchange/counterparty risk. These are workflows that traditional funds and investors are accustomed to.

Exchange Arbitrage

HY: Dealer price arbitrage exists in HY, where different dealers quote different prices, and price discovery is often challenging. Some "fast money" investors take advantage of these price discrepancies, but most investors and asset managers don't bother. Instead, they simply understand that real liquidity is different than what the dealers indicate on their runs, and that pricing service quotes are often inaccurate. While this may not be ideal, it is a reality, and investors have learned to work around these inefficiencies while striving towards removing them.

Digital Assets: In crypto, hundreds of exchanges exist, and often the prices across exchanges are wildly different, which leads investors to wonder about transparency, manipulation, and the ability to achieve best price. A large sub-set of crypto funds and market makers exist right now to take advantage of this arbitrage, but over time, these inefficiencies will be reduced. But even if it doesn't completely disappear, with the right expectations, investors can navigate around these issues.

Fake Volume

HY: HY dealers embellish their volume numbers all the time in order to attract more client flows. TRACE has provided some transparency, but it doesn’t distinguish between a $2m trade, a $5m trade, or a $100m trade, and dealers use this to their advantage by fabricating their volume. Further, TRACE has led to rampant manipulation in HY bond prices as dealers and even some funds have learned to “paint the tape”. These little blips don’t derail the entire $7 trillion high yield market efficacy, and investors have learned to trust certain dealers over others.

Digital Assets: It’s been widely reported that a high proportion of crypto volume is overstated, and is manipulated through wash trading. Investors are learning to avoid these exchanges, and over time, most transactions will occur on more legitimate exchanges.

Liquidity Gaps/ Thin Trading

HY: High-Yield bonds and Emerging Market bonds “gap” up (or down) all the time on no volume when market makers move their markets quickly to avoid getting taken short (long) at levels where they know they can’t replace the risk. This happens until a new equilibrium occurs. This is similar to how a casino sports book adjusts their betting lines until equal betting activity is achieved on both sides. Further, with distressed bonds, it is not uncommon to buy a distressed bond on the way down at 80 cents on the dollar, 60 cents on the dollar and 40 cents on the dollar… all in the same day. When news comes out, prices adjust forcing market participants to react to new prices in a way that may or may not be immediately transactable (i.e. it takes time to get to a market equilibrium where there are equal buyers/sellers on both sides).

Digital Assets: Bringing this back to digital assets, just because crypto exchanges allow anyone to see real-time prices does NOT mean that any trading is actually happening at these levels. This is an extremely immature market that is lulling people into a false sense of liquidity by showing constantly available prices that appear to be transactable, but in reality are not. Prices of many digital assets can fall or rise dramatically on little to no volume. Recently, a new equilibrium for Bitcoin didn’t occur until prices moved up 25% in a single day. Even though Bitcoin has a $150 billion market cap, and you’d expect reasonable liquidity for something so large that trades on so many exchanges, the reality is, liquidity is only there until you need it. And short-sellers have learned painful lessons numerous times on misperceived liquidity. The overall size of the crypto market ($250 billion) is dwarfed by the size of the High Yield bond market ($7 trillion), yet these same market dances happen all the time without anyone batting an eye in HY even though it affects much greater wealth. However, these moves are not normally reported by the press since the headline number is simply smaller (a 5% move doesn’t generate click-bait in the same way as a 25% move does).

Hung Deals and Mismatched Prices

HY: In 2007 and 2008, the LBO-fueled debt wave resulted in investment banks / broker dealers getting “hung” with large amounts of underwritten bonds that they couldn’t sell. They were forced to wait until market conditions improved before leaking these bonds out to the market, and many investors were able to buy these at very attractive prices.

Digital Assets: The same thing is about to occur in crypto. Many 2017 and 2018 ICOs are still “hung” on investors’ balance sheets (rather than underwriter’s balance sheets). Most are mismarked, and all are mispriced. At some point, these privately issued tokens are going to have to come out to the public as the notion of liquidity was (and still is) a big part of the story of these ICOs. When, and if, these tokens get launched on exchanges, the inevitable price drops may cause a bit of a ripple effect through the market. Further, some funds have shut down, and these investors are forced to sell, providing a good buying opportunity at distressed prices for those funds who can take this risk. Many of these projects are good, and have solid tokens with strong teams that should sort itself out over time.

Public / Private Markets

HY: The HY market has a healthy public and private market. The public market is easy to trade and is fairly liquid, while the private market including 144a deals and bank debt, is much more opaque.

Digital Assets: Similarly, the crypto markets have publicly listed tokens on visible exchanges, as well as privately listed SAFT deals and tokens that only trade through insider transactions. There are different investor types focused on these different markets, and they each take different skill sets.

Information AsymmetryHY: The HY market has a handful of firms that get information faster than others. Either the dealers call them first with banking transactions, or their salesman at the Broker/dealer calls them first when big trades are about to happen. Digital Assets: Similarly, a handful of large crypto institutions get first look on hot deals, and often have information with regard to big VC investments, exchange listings and block trades. Thus, where small firms may benefit by being nimble; large firms benefit from better access to information.

Capacity Constraints

HY: Blackrock, PIMCO, Fidelity and a handful of others often move markets in HY just because their trade size is larger than the market can support. This can cause ripple effects, but the funds and their investors have learned to navigate around these constraints, as have the dealers.

Digital Assets: Similarly, a handful of larger funds in crypto have a limited ability to buy certain assets because their size requirements dwarf the size of the underlying asset. Like HY, crypto funds and dealers will learn to navigate.

Valuation and Intrinsic Value

HY: Some high yield bonds have very high recovery values in the event of a default in addition to offering high yields. But a majority of unsecured high yield bonds are issued by companies that are perpetually free cash flow negative, and have no chance of ever paying off their debt due to their high debt burden and crippling interest payments. Investors almost universally agree that many of these bonds have no recovery value in the case of a default. The only reason these investments have value is due to “bond math” and probability analysis -- namely, how many coupon payments will the investor collect, and will the investor be repaid the principle upon maturity. These outcomes are 100% reliant on the company’s ability to refinance itself with new debt when old debt matures. So while we all know how to value a bond based on present value of cash flows, the present value formula is heavily skewed by the last cash flow -- the principle repayment. And the reality is, when investing in these instruments with zero recovery value, you’re making a prediction on the likelihood of others to refinance this debt when it matures. Thus, part of the “valuation” is an assessment of the behaviors of others -- namely, will enough investors refinance old debt with new debt.

Digital Assets: We often hear that crypto can’t be valued, or that there is no “intrinsic value” to the underlying digital assets. Like high yield bonds, there are different types of crypto assets. Some have real recovery values and real intrinsic value (i.e. those that offer cash paydowns), others can be valued based on their yield (i.e. digital assets that pay dividends or “staking rewards”), and other digital assets are more like subordinated bonds with no recovery value. But, these assets may still have value due to the behavior of others. Part of the valuation analysis includes the probability that demand from others will exceed the supply of tokens, and since demand is driven by community engagement and utility of the token, this can be measured using probability analysis. Thus, to say that digital assets have no “intrinsic value” would be no different than saying that a majority of the high yield bond market has no intrinsic value.

Conclusion

The digital assets space is new, different, and largely untested. But so are all new asset classes and products. From high yield bonds to CDS to CLOs to ETFs, they all started somewhere before becoming mainstream investable assets. We are in the early stages, but there are analogs from previous history that can help us mitigate risk.

To learn more or talk to us about investing in digital assets and cryptocurrency

call us now at (424) 289-8068.