What happened this week in the Digital Assets market

What happened this week in the Digital Assets market

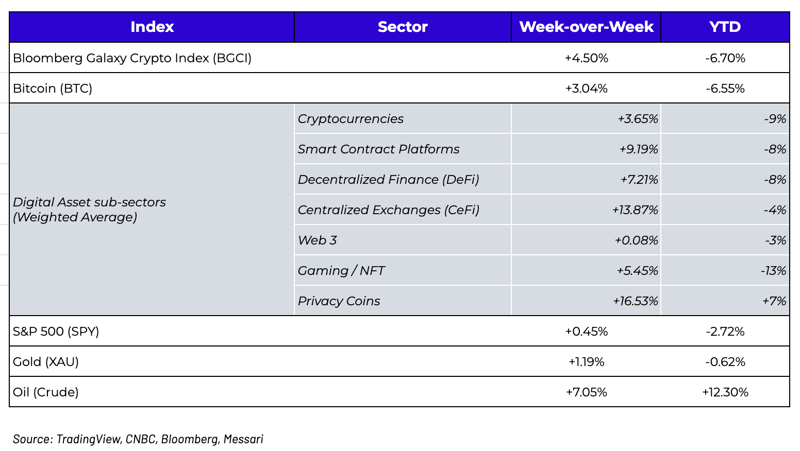

Week-over-Week Price Changes (as of Sunday, 1/16/21)

Source: TradingView, CNBC, Bloomberg, Messari

Inflation data shall pass – long live dispersion

Most digital asset subsectors bounced back last week, with sharp gains seen across the board, kickstarted by a “benign” CPI number that came in line with expectations (albeit still incredibly high at +7.0% y-o-y, the largest gain since 1982). It’s still a bit bizarre to acknowledge that a US-centric economic data point is such a driving force of sentiment and price action in global digital assets. It is also a tad ironic given that the bull case for many digital assets in Spring 2020 was expectations for higher inflation. Now that we actually have inflation, it is weighing on prices. Will the market really continue to be on pins and needles every time we get an inflation report or a Fed soundbite? Doubtful. Last week, we wrote that price reactions to current macro conditions were overblown and would not be a significant headwind to risk assets for several years, if at all. But let’s go even further, and revisit May 2020, back when the market was temporarily uber focused on every jobs report for similar insights into the Fed. At the time, we wrote:

“One of the hardest aspects of trading and investing in a new asset class is the lack of historical, and thus predictable, data. Even the smartest quant trading firms and algos don’t know which factors to focus on consistently. There have been times when digital assets have led other risk assets (last month), and times when other risk assets have led digital assets. Sometimes Bitcoin dominates the direction and magnitude of other digital assets, and other times (like last week) Bitcoin significantly decouples from other assets. Given their global presence, at times Asian equity and currency markets drive digital assets, and other times the US dominates the flows (currently). Historically, US economic data and Fed policy have had no impact on digital assets, yet many young digital asset investors just started focusing on weekly jobless claims numbers every Thursday as if this data point just started being released in 2020. And since this asset class is so small, oftentimes retail flows have a massive influence on price during momentum trades (like last week), while just one or two institutional investors can dwarf everything else just by entering the scene (Paul Tudor Jones earlier this month).

Of course, this is also why there is so much opportunity and alpha relative to other mature and saturated asset classes. Very few active managers outperform passive indexes in equity and debt markets, yet the opposite is often true in digital assets. This is partially because market-weighted and other rules-based passive indexes can’t accurately reflect such a fast-changing and evolving asset class, partially due to active managers taking advantage of high levels of volatility, and also partially due to how quickly narratives of relevance change. These shifting narratives are hard to keep up with.”

Said another way, “This too shall pass!” The market will most likely move on to something else in a few months. And that is why having micro-level investment theses, sustainable valuation techniques, and thematic investment focuses has been much more critical to digital asset investing success than having a broader, top-down macro thesis. This has been evident in the first two weeks of 2022, even as the market has focused on macro. A massive decoupling is already occurring as investors rotate out of large-cap Layer 1 protocols into emerging ecosystem tokens that haven’t yet matured. Jonathan Cheesman of FTX laid it out nicely in his weekly recap:

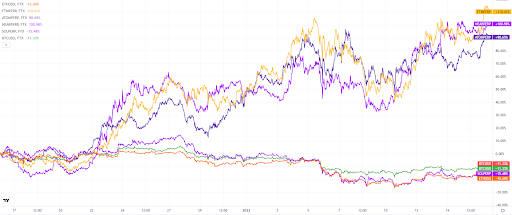

“BTC and ETH have been struggling for some time, but in the last month you can add last year's poster child SOL too. Over the last month, negative double digit returns for BTC, ETH and SOL; meanwhile, ~100% returns (yes in one month!) for NEAR, FTM and ATOM. Part of the reason is staking/farming yields on these upcoming layer 1s are so profitable that the total return creates a virtuous circle. Thinking big picture, since [digital assets] are meant to disrupt the rent seeker model in traditional finance, as the market matures, returns will require network participation rather than just investment capital (which there is an abundance of). We are starting to see this with how some new token projects are distributed and NFTs may play this role too - being part of a crypto network should be an active, not a passive role.”

Price dispersion of NEAR, FTM and ATOM compared to BTC, ETH and SOL - Last 30 days

Source: FTX/CoinTracking

This last point is the most important. While many casual market observers were able to print a pretty satoshi last year simply by watching their favorite assets go up, 2022 is likely to require a much more careful, nuanced, and active strategy. In fact, this was one of the major themes from our 2022 market predictions:

“Some of these sub-asset classes will do well while others perform poorly. We may continue to have steep, quick, highly correlated corrections, but as we’ve seen throughout 2021, certain assets and sectors will bounce back faster and stronger than others. If you’re looking to short “digital assets”, you better do a lot of research into the specific assets you are shorting. A lazy man’s approach to broad-based, 2018-like declines will not work in 2022.”

Fully Diluted Value is Misleading

While we got very little pushback on our “macro is overblown” argument last week, a smaller section of our writeup created quite a controversy. We introduced a new token, Ronin (RON), and discussed how the market was likely severely mispricing this when-issued asset. In our report, we indicated that fair value for RON was likely closer to $24 than the current whisper price of ~$5. The pushback was based on our estimation of market cap used in our comps analysis, which only took into account current circulating supply of RON (100 million tokens will be outstanding on day 90 when Phase 1 of the farming rewards ends, representing just 10% of total supply) and not the fully diluted supply of RON tokens.

The feedback we received immediately focused on our valuation technique and why we were dismissing the fully diluted value of RON (1 billion tokens) and instead focusing on circulating supply (100mm tokens). Clearly, this is a big delta and causes quite a discrepancy concerning any sort of valuation technique that would determine where RON should trade. “Fully diluted value (FDV)” is yet another flawed metric used to put a ceiling on digital asset valuations that sounds good in theory, but in practice is quite nuanced. Sure, it’s important to understand how much total supply could exist in theory, but it’s even more important to understand the probability of ever seeing that fully diluted number of tokens in the wild. In the equity markets, investors tend to focus on outstanding shares instead of authorized shares, which is a similar concept. Companies have a limit on how many shares they can issue (authorized), but market caps are calculated based on how many shares have actually been issued (outstanding). Only when these shares come to market via a secondary offering, or are telegraphed in a future issuance by management, do investors tend to focus on the dilutive impact. Moreover, it is often not difficult to increase the authorized share count via board approval, or to reduce the outstanding shares via buybacks. Why do most market participants dismiss authorized shares? Because without a roadmap or a plan for how and when these shares will be sold/distributed, it is simply too nuanced to bake into calculations. In the corporate debt markets, investors tend to look into bond covenants to see how much total debt a company can issue before tripping a covenant, thus putting a theoretical cap on issuance. And while this number is important, again, most investors focus on the total indebtedness of the company today, with a footnote into how much leverage the company may be able to incur if they max out their total debt issuance. Once again, this future indebtedness only comes into play if there is a rationale for why the company will need to issue more debt (declining cash flows, higher expenses, acquisitions, etc.) For government bond markets, there are no covenants, and therefore the “fully diluted supply” is technically infinite (unless you place any importance on the theatrical debt ceiling farce).

The same concepts are now true for digital assets. While it is crucial to understand and be aware of the fully diluted potential supply of an asset, it is (in our opinion) far more important to understand current supply and demand forces, with a simple footnote into what could ultimately be issued in the future. While Bitcoin is unique with its predictable and programmatic future issuance schedule, the vast majority of token issuers still resemble companies more so than programmatic currencies. As such, future issuance is not a foregone conclusion. We’ve seen many instances where these issuance schedules are changed, either by a small centralized management team or via governance votes for decentralized projects.

For example, in the ongoing Curve Wars, CRV includes a way to effectively reduce FDVs by locking newly released tokens for up to 4 years. Merit Circle (MC) just passed a proposal on January 2nd to reduce its circulating and total supply. Binance constantly tinkers with the formula it uses to burn Binance Coin (BNB). Arca was involved in blocking a dilutive and unnecessary token issuance from Sushiswap (SUSHI) last year. Aurory (AURY) just changed its seed vesting schedule, pushing back the cliff by six months. Yearn Finance (YFI) went the other direction, voting to increase its token supply issuance. The list of supply changes goes on and on. There is a reason we separate circulating supply from fully diluted supply. Just because a token exists does not mean that it will ever leave the project’s Treasury and be issued to investors. And that is a big distinction. We often hear about “token unlocks” and “VCs dumping on retail”, but this is an entirely different argument. When a token issuer sells tokens via private sales to investors (VCs), they often come with a lockup, whereby these tokens cannot be sold until 1-4 years in the future. When these “unlocks” occur, the venture capital investors are incentivized to sell, which can cause a massive price decline (see ICP or FIL). But those tokens were already issued and outstanding; they just weren’t trading—which is completely different than unsold inventory of tokens. A token issuer has little control over what an outside investor does with her tokens once an unlock period ends, but has total control over whether or not tokens are ever issued in the first place.

So while FDV is a metric, it is not a particularly important metric until you have visibility into how and when these projects will be diluted. Once again, those who do their research in digital assets have a stark advantage over those who fail to read the fine print.

What We’re Reading This Week

And That’s Our Two Satoshis!

Thanks for reading everyone!

Questions or comments, just let us know.

The Arca Portfolio Management Team

Jeff Dorman, CFA - Chief Investment Officer

Katie Talati - Head of Research

Hassan Bassiri, CFA - PM / Analyst

Sasha Fleyshman - PM

Alex Woodard - Research Analyst

Andrew Stein - Research Analyst

Nick Hotz, CFA - Research Analyst

Wes Hansen - Director of Trading & Operations

Mike Geraci - Trader

Kyle Doane - Trading Operations

David Nage - Principal, Venture investing

Michael Dershewitz - COO of Arca Funds

To learn more or talk to us about investing in digital assets and cryptocurrency